Who needs a mortgage? Cash sales continue to dominate market while mortgage applications run near levels last seen in 2000. Housing starts remain weak and expectations for price increases run wild.

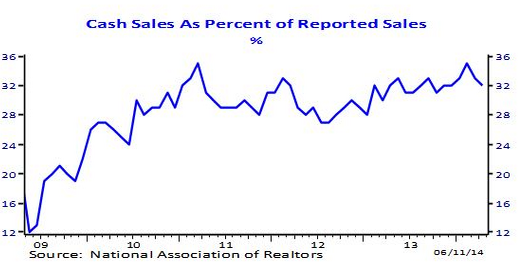

Apparently very few people need mortgages to purchase homes in the market today. One out of every three homes sold (at least those on the MLS) are going to those “all cash†buyers. Investors continue to dominate the percentage of all sales but the total number of sales is actually pathetically weak given the rise in prices. You would expect that somewhere in the rush to purchase regular buyers were the engine of this price increase. They are not. Even builders are not tempted to go out and build. Why build? For the younger broke generations living at home because of the weak economy? In California we have 2.3 million adults living at home. These people live at home because even a rental is out of reach let alone a $700,000 box with walls that are so thin, you can poke your finger through the crappy drywall and waive high to your other massively indebted neighbor. Looking at mortgage application data, it seems that people are simply not applying for loans. This is why in this housing “recovery†I’m not hearing the constant glee from mortgage brokers and real estate agents. Sales volume is low and mortgages are for the plebs in the streets trying to squeeze into these overpriced homes. Who needs a mortgage? Apparently traditional buyers but they are hard to find in this market. Even in high priced California, sales fell in May to 37,734 from 37,988 in April. This is a time when sales heat up. To put this in perspective, we had 67,958 homes sold back in 2004, a full decade ago.

Cashy cash cash

While investors slowly begin to pullback their suitcases of juicy Fed induced money, cash sales still make up a large portion of all sales. Going back to 2009, nearly 1 out of 3 purchases has gone to non-traditional buyers circumventing the mortgage process. It is actually higher because in the panic days, many big investors were buying in bulk off the MLS books via auctions and direct deals with banks. These were the best deals and of course, the public (the folks bailing out the banks) got no shot at these fantastic deals. Did you have access to borrowing rates near zero percent from the Fed? Of course not! You should be happy with the current 4 percent mortgage rates so long as you pay $700,000 for some Cracker Jack box with one functional toilet.

Here is the latest cash sales data:

Cash buyers continue to be the biggest player at hand buying up 32 percent of all homes last month. Prices are overheated since incomes are not going up. Investors, many of them looking for cash flow actually need local families to generate enough income to pay rents. Some are flipping but good luck flipping when prices go stagnant as we are now seeing the plateau phase hit.

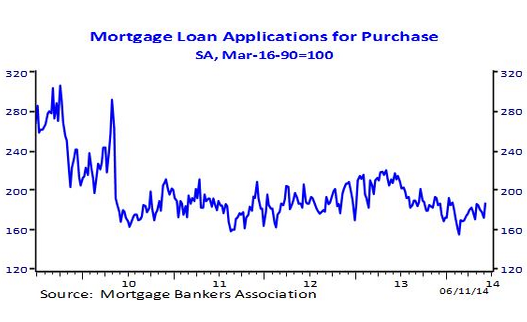

You would think with low interest rates that the public would be at it in terms of mortgage applications but they are not:

Mortgage applications remain at levels last seen back in 2000. In other words, people are not applying for mortgages needed to buy homes. Sales remain weak because the public is shut out of this game. And it is not for want of buying a home. Oh no. Rest assured the public if given the chance for toxic mortgages would be in the game the first chance they got. I constantly get e-mails about people saying things like “we overbid by [insert ridiculous tens of thousands of dollars] on this property in San Francisco and still lost out. What can we do?†This is part of the current game right now. Cash is still king yet slowly, people are starting to regain their senses.

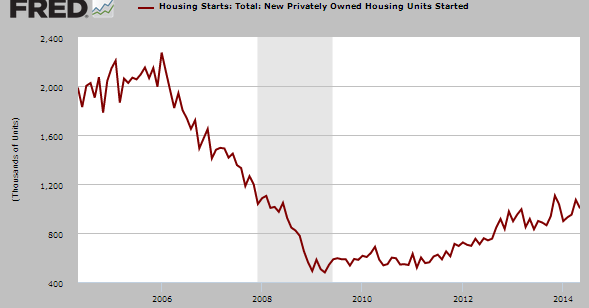

Housing starts continue to remain weak:

Why are builders not out building homes in this hot market? Newer homes typically go to your more traditional buying crowd and carry a premium, a premium that many income constrained households just cannot pay. That is very clear. What we have is a lack of affordable housing based on current financial conditions of US households. The market is largely manipulated and we all know this. The nonsense of “supply and demand†is for a kindergarten school books when you have the Fed buying up nearly 100 percent of all mortgage-backed securities, investor/dark pools of money crowding out regular buyers, mark-to-market fully stunted, and banks essentially dragging their feet like zombies on the foreclosure process only moving when it makes sense in their benefit (after leveraging every penny out of the bailouts). So yes, supply and demand matters if this were a fully normal economic system but alas it is not. House lusting sellers and buyers only care about one thing; what a house costs today. In fact, the epic housing bust we just faced is now a distant memory to them.

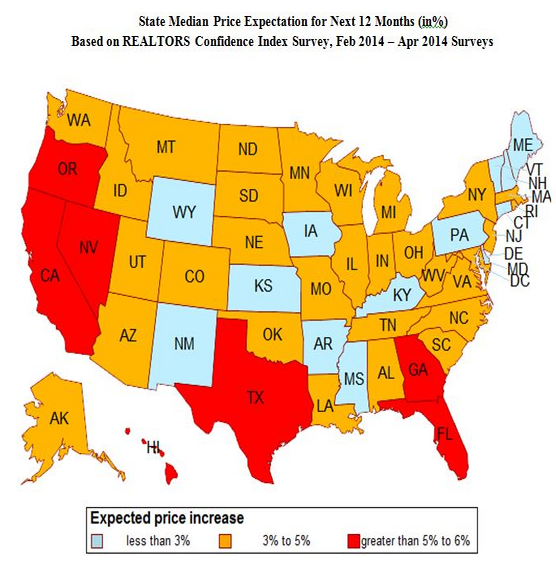

Optimism is running wild. Take a look at price expectations for the next year:

Source:Â NAR

The kings of housing bubble 1.0 are back in it! California, Nevada, and Florida are expected to see price increases greater than 5 to 6 percent. Every state is expected to see price increases even though income is slated to remain stagnant and interest rates are likely to increase (although what does it matter if the mortgage buying pool of buyers is marginal in this market).

So who needs a mortgage? Traditional buyers. Yet they are the folks now trying to compete with investors and all cash buyers and using ARMs (doubling in California over the last year) just to stretch their household incomes to get into those crummy drywall crap shacks so they too can pay for a piece of junk for 30 years, only to have to eat cat food into retirement and pretend their box is “worth†$1 million even though they are unable to sell since they cannot envision living anywhere else. Yes, this is the current psychology of the market. Sure sounds like a new “normal†to me.

I’m curious for those actively selling and buying right now. What is your current thought process on this market?

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

127 Responses to “Who needs a mortgage? Cash sales continue to dominate market while mortgage applications run near levels last seen in 2000. Housing starts remain weak and expectations for price increases run wild.”

That map indicates California home prices (if the Realtors, who are biased, are correct) will increase over 5-6% in the coming year. If so, there will be no Hard Tank.

I expect Jim Taylor will beg to differ.

Yet it’s been 3 months since the Ides of March.

And 2014 is about 46% complete.

I still see no Hard Tank yet. Some houses have seen prices cuts. But others are still being overbid.

Would you believe housing to go up 30%?

This house is so hot the list price is up -37%, that counts as a healthy housing market, right???

http://www.redfin.com/CA/San-Gabriel/6029-N-Willard-Ave-91775/home/7039508

“This house is so hot the list price is up -37%…”

F’ing brilliant!!!

Don’t Call It a Price Reduction

http://realtormag.realtor.org/daily-news/2014/06/12/dont-call-it-price-reduction

RE: Tired of the BS

Great link! Realtwhore newspeak at it’s finest.

Bread and circus while Rome burns

I’m in escrow for home in N San Diego County. A good property 3bed/2ba 1950 sf built 1980 and in good shape. On 1/1/2 acre with fruit trees, hilltop location. Was offered for $500 and I offered $500. I didn’t both offering lower because I kept running into other buyers in my price range while searching and just wanted to get the place, one of the better places that needed no refurbishment at all. Very slim pickings and for some reason, in this area the number of houses offered suddenly cut in half (from about 67 down to 35-40) while I had assumed at this time the inventory would be up. Anyway, looks like my deal will go through moving me out of Westside L.A. where I’m paying $4000 mo rental that’s taking up every extra dime I have. Deal is 30 fixed, 100K down 400 mortgage at probably 4.625. Payment will be about 2,000, taxes about 500, insur 100 so I’m glad to be out of the rental game on the Westside.

West L.A. has a higher level of demand than N. San Diego County, so comparing apples to apples, not only would one expect properties in the latter to cost less, rent would also cost less. That’s aside from both areas being two different lifestyles and all. Wondering what the point would be of comparing rent in West L.A. to a purchase in N. San Diego county.

Not only that, the comparison just shouldn’t exist at all… This guy is saying moving into $500k is better than paying $4k in rent….well if he was renting a place worth $500k in LA for $4k he was getting robbed…he was likely renting something worth around a million.

The house I rent is split with roommates and we pay $4,500 – and it’s 1800 sqft 3/2 remodeled nicely, in a nice quiet neighborhood a few miles from the coast. Would sell for just over a million.

One could ‘save money’ monthly by buying a $500k place instead of renting a $4k one…but you know what $500k gets you on the westside? Definitely not a SFR, haha…so he downgraded by changing location. You have to downgrade somehow…either move far away, move to a condo, or move to a terrible neighborhood…

Just out of curiosity, how did you accumulate that $100K down payment? I’m just wondering how people get all this money when household savings rates are down considerably and as you said you were spending nearly every dime on rent. Congratulations on your new home.

We have saved up over 150k in the last 10 years. We started living in a 1 bedroom rental in a very dicey part of town. Rent was cheap and we were frugal. As an example, I started out making 40k a year, the wife sold things on ebay in her spare time. I changed jobs, got promotions but we kept the same lifestyle. By the end of those 10 years I was up to 100k a year salary and saving probably 50% of what I earned. We saved… bought a couple new cars, cash. As I got promotions and pay increases over the years we kept the same level of expenses and put all the extra into savings. We missed some opportunities to buy due to some unexpected expenses, but now we are in a nice rental in a good neighborhood and still saving… just not as hardcore as before.

Now we are just waiting and watching the market… it’s crazy, and I’m in no hurry to throw down that huge down payment that took so long to save.

I had coworkers who made the same money as I did, but spent 4 times the money we did on rent. Their savings never increased, but ours did.

Once you start saving, it becomes an addiction of sorts… pushing yourself to see just how much you can put away and how little you can get by on for that payperiod. Seeing your savings grow is worth it.

“Just out of curiosity, how did you accumulate that $100K down payment?”

Slang’en, pimp’en, ho’en…

I’m an older person whose spouse has died. The 100K was hard earned over a number of years. While my spouse and I made a good living, we lost a lot in investments the downturn, spouse was very ill for a number of years and didn’t work, had some bad financial advisors we trusted, so not easy to get past these pitfalls to get the 100K. I don’t know how other people manage to do it. I suppose I could have gone in for a jumbo loan and gotten into a bigger place, but felt payments would be easy for me at this level rather than going all out for what some lender might think I could afford. And no, I will not miss L.A. Lived there most of my life, born in Manhattan Beach and I’m ready for a small, kind, humane town where I don’t have to spend $10 a day for parking.

You are leaving the Westside to live amongst uncultured backward country hicks. You will be back. I spoke to my friends at the Café on San Vicente Blvd in Brentwood, and they could never imagine leaving to go to live amongst such people.

C’mon Ashly, Brentwood has been a cultural wasteland ever since Dutton’s closed. You poor souls at the Café must suffer so.

Hey Ashly,

You and your comically elitist “Friends from the Cafe” can kiss my a$$. What a joke. See ya at the fundraiser!

Ashley

are you a transplant from outside of LA? Even us native westsiders (Venice, Santa Monica) would not want to hang out on San Vicente blvd…:)

apolitical scientist , Caffe Luxxe is one of my places, for meals, it is the Toscana Restaurant. I am high maintenance.

Venice boy, QE abyss, I live north of Sunset, you are not in my league.

FWIW, Nicole Brown Simpson used to hang out on San Vicente Blvd. She’s on my mind, because yesterday was the 20th anniversary of OJ’s Bronco chase, and KFI’s John and Ken Show were making a big deal out of it, replaying tapes from that day.

I often go to the Starbucks on San Vicente Blvd., the one near the Brentwood Country Mart.

Ashly РDid you know your favorite caf̩ is not the enter of gravity? I know, blows your tiny mind, huh.

If you are putting 20% down, you may want to consider using a credit union with a 15/15 programs. It is an ARM that adjusts once every 15 years. The rate is currently at 3.5%. The loan is a 30 year amortized loan.

My family and I are currently in the market for a home. Not for an investment, but more to lower our overall costs (owning is cheaper than renting in our area of San Diego). We own a home in OC as well, which has almost doubled in price since we bought it in 2011. Opting not to sell it as its cash flowing and we enjoy the passive income.

I am buying knowing that prices will stay flat or go down over the next 5 years since incomes won’t increase or keep pace with inflation. We are planning on being here for the next 15 years at this point and as such, the key is fixed housing for us as well as the ability to update/customize our home.

I’ve been reading these stories for the last couple of years now, and it seems like a conspiracy. You would think even the true investors would be backing off at this point, but they keep the prices high and out of reach. It feels like the Fed took a percent of that 85 billion each month, and gave it to some agents in each city/state with instructions to keep outbidding and buying. I was considering trying the auction.com thing, and watch so many POS’s in crappy neighborhoods go sky-high. Who in their right mind would pay so much for these?

I’m a single guy living in Phoenix, have a great job, and never owned a house. Even before the crash I didn’t want a mortgage. I’ve been saving for years, and after paying off my only debt; a car and a $6k student loan, I’ve manged to put away $40k.

Even if I wanted to do the whole 20% down thing and go broke buying a $200k house, I don’t see anything under $250k in the areas I want. The idea of being locked in to a life time of debt is not appealing to me.

Well, thanks for letting me vent. Here’s to driving a old sun-faded car, living with a roommate, packing frugal lunches, and hoping the fed/gov doesn’t come after our bank accounts for not spending enough money.

The conspiracy is on the supply side. The establishment has been actively restricting inventory in an attempt to quell losses and stoke organic demand. They have so far succeeded in stabilizing balance sheets with a cost of stalling activity. Too much gas drowns the flame. The bulk of what little activity there has been is speculation-based and specuvestors are simply acting like flies being drawn to shit doing the only thing they know. No one wants to take the lumps for poor decisions of the past — especially those most at fault.

Ryan, the interest rate for deposit in the bank is less than 0.1%, and the food and gas price is up 5% every year. They have been after our bank accounts for the past 5 years. Larry Summers talked about the negative interest for a while. So our economy is the opposite to the common sense belief.

Cash sale without loan creation is net negative for the economy, and it is deflationary for the bank, since it shrinks the bank’s asset base. It decreases the bank’s liability also. Banks don’t feel like to give you a loan either, sot the lending standard is high. Its hot market out there, but people feel like shit.

LA Gas prices for the last 4 years (prices per gallon of regular in June for consistency):

2011: $4.016

2012: $4.285

2013: $3.995

2014: $4.175

While 2014’s June price is indeed 4.5% higher than 2013’s there’s hardly a strong year by year inflation trend in this over the last few years. I won’t deny that there’s been some inflation in food and energy, but the whole “government is lying to us about inflation” meme is a bit overdone.

There is not a single thing about the government lying in my post. Inflation or deflation is not evenly distributed. Your wages are not increased, and it is at best stable. The prices of tech gadgets are going down, no inflation there. However, there is a large segment of our society over 70 years old, and they only buy food, and medicine and some daily necessities. They have limited income, and a lot of their income is from bank savings. The bank interest rate is basically gone, and these people’s income from their savings is gone. So good luck with getting all the grandmas to the soaring stock market.

It is common sense that people play with fire get burned. Prudent people financially should not get punished. So in the crisis, cash is dear, and cash should get reward (return). you should be able to buy things cheap. That was not happening in the past crisis. It was just opposite that happened.

“Inflation” is a tricky concept. I have argued that Fed “printing” has not made its way into the M4 (not reported anymore) money supply. I think many of the price increases have more to do with market manipulation than money supply. Food prices have been sky rocketing but this really is all about the weather. Water has been rationed versus priced according to “supply” and “demand” and it has had a huge impact on crops which then feed livestock. The whole chain has been affected by the weather and we are seeing the consequence. Fuel has been pretty flat averaged out over the past decade or so. Remember, we had $4 gas during the Bush administration. Housing is the real issue in my mind. Rent and cost of buying have gone through the roof because of market manipulation and inventory control. There are other items as others have stated where some go up other go down and it is probably a wash. The real question is where is the rental equivalent (the way the fed measures housing costs) in the reported CPI? I think they have to be fudging this part of the index to continue to report less than 2% inflation… Not that anything is real anymore…

My thoughts are two fold I need to move to be nearer a job and I can buy for 20% less than renting and have more space, yard etc. I’d rather pay the ~2k mortgage for a place I will own long term if prices stagnate or if things are higher in the mid term explore my options.

I guess I’ll continue to rent for the foreseeable future.

It is quiet out there…too quiet. Where is everyone? Am I actually the first to post a comment? This is spooky.

Dr. HB,

I am not currently actively buying or selling. I am, however, somewhat affected by the housing market in the sense that I do not trust it any more than anyone else on this blog. I’m saving up $$ with which I can build my dream home on land I own in Oregon free and clear. If I wanted to build now, I could tap into equity in my current home to add to the $110K I have saved so far. But because I don’t want to be caught in the trap of so many who utilized their homes as ATMs just before the last housing collapse, only to be “under water” afterwards, I think I am definitely affected (albeit indirectly) by the current state of housing and our manipulated economy. So I will continue to save my $$ and by the time I take early retirement in about 10 years, I might have enough to pay cash for building a modest home.

No more mortgages for me…too confusing!

When or why won’t the Feds charge higher interest rates for investors? Keep the lower rates for those that buy with intent to live there. Wouldn’t that help things?

My family and I have been planning to move from Illinois to Southern California for about a year now. We preparing to sell our beautiful 3-BR 3.5-BATH 2 story home built in 2002 with a 2 car garage and big yard valued at $186,000 and move to SoCal to get away from the nasty winters and into the sun and traffic. Given the state of the housing market in SoCal …..please advise :p

Sorry, evermind the “please advise” … that sounds rhetorical. But I will say I find this blog as entertaining as it is informative. Keep it coming!

for $200,000 you might be able to find a 2 brm 1 bth house in compton. or just rent in a nicer part of LA. i just sold my 1 brm 1 bth condo in downtown long beach for $170,000.

good luck

Here’s some advice. The grass isn’t always greener in SoCal but that won’t stop many from convincing themselves and others that it is. There’s a cost to everything. No free rides and no utopia.

You can say that again, And I sure as he’ll ain’t gonna comit to a mortgage for a 1 bath $600K Crap Shack built in 1961 and flipped with hardwood floors, granite counter tops and ugly HGTV backsplash. I’ll be renting unfortunately.

@John E Bucks, LOL!!!!!!!

You have a disturbing sense of humor. It’s a question of income level. If you earn less than $60K per year, you won’t last for long in SoCal. $60K per year is the minimum household income you need to stay out of the ghetto/barrio/slums/Riverside/Ontario.

“$60K per year is the minimum household income you need to stay out of the ghetto/barrio/slums/Riverside/Ontario.”

I think you have a typo here. I think you mean $160k…

The question is, what are your requirements for housing? If you don’t really need a lot of white collar employment opportunities, there are a LOT of nice places in SoCal that are not nearly at LA prices. LA is horrible anyway – please don’t move there. Look into Claremont, Temecula (I’m biased), San Marcos. There are many others.

http://www.redfin.com/CA/MT-BALDY/13-BARRETT-CYN-91759/home/17275606

This and drive down about 18 miles to work in Pomona.

Or something similar. Keep searching, IMO. If your family really wants to live in SoCal, there is a way. “When there is a will, there is a way.”

I say don’t be discouraged. I’m from southern California and went to live on the east coast and the snow and shoveling was too much for me and I moved back. I’m going to stay here and live in a modest safe area.

Mansion near the beach is not mandatory!

In other words, if you lower your standards and stretch really far, you too can live the California dream. Please. There are good reasons why this place is priced the way it is and the owner is willing to carry the financing.

There are no shortcuts. You either pay in money or in sacrifice. It’s a high cost of living either way.

Tired of the BS,

How is that stretching far? Moneywise, it’s about the same as he is selling his house for. Distance wise, it’s about 18 miles to major cities. The little town of Mt. Baldy has some population and little stores. Yes it’s more like a vacation house in the mountains, but it’s better than being in debt for an expensive house in bigger towns, cities.

There are no shortcuts. There are tradeoffs. With this house, you are giving up convenience to stores/movies/city attractions. Good part is it’s big, cheap and comes with lots of land.

Great recap of the housing bubble 2.0. The average buyer never had a chance against investor pools using virtually free money.

Folks holding on to the white picket American dream had their futures bought and sold several times over in the last decade.

The moronic herd mentality that causes people to overbid in a market that is double historic valuation increases is boggling. Round and round it goes…

Just made all cash offer in Eastlake San Diego because of good values and great schools. Offer accepted. Closing in 12 days. Keeping current residence as rental because condos still have NOT recovered in price from the crash. Bought another condo in Bay View with mortgage financing solely for rental income. Good rentals with modest upgrades are in huge demand, even more so are those that allow for a small pet. These landlords can often captures high quality and responsible tenants if priced fairly, with a modest premium built in for allowing mans best friend.

Wondering what your thoughts on reverse mortgages plays into baby-boomers.

I think your articles are great and look foward to them…thanks

My thoughts, FWIW, is: I know a woman, early 70s, who has opted for reverse because she needs the money – lives in Santa Monica, bought her place for 125K now worth well over a million, but south of Montana Ave. She was middle class, then divorced, now retired. She can’t keep her home unless she’s reverse mortgage. Hanging on by her fingernails until she dies is why this “reverse mortgage” business was invented, in my opinion.

I have a friend also, an elderly woman, retired and living off social security living in her 2bed 1 ba home in Mar Vista. She bought it in the 1970s. Although the house is worth approx $700K which she could sell and then buy a 1 bedroom condo somewhere in WLA for half that amount (and then have $350K to live off) she would rather scrape by and even opt for taking the bus rather than spending gas money. I asked her why she doesnt sell her house and relocate for 1/2 or 1/4 what the house is worth and she says: “I love my house and I love being near the beach”… perhaps a reverse mortgage is in her future also.

Regarding your request for current buyers and sellers comments our home in Northern California is currently in escrow. The market is still very not in our area. Just signed escrow docs in our home and I was told the buyer will sign theirs as soon as the bank issues loan docs. We had many eager buyers and multiple offers. It has not closed yet but I expect it will as the buyers seem motivated and are financially sound. They put 300K down and financed the rest. I see where the So Cal markets are cooling off but it doesn’t seem to be happening here, yet. Silicon Valley is rife with big employers. I believe unemployment is way down in our area. Even during the last horrific downturn many people here weathered the storm quite well. Really, its only the very well healed who are able to buy here as prices are sky high. Traditional middle income home buyers are really non existent. We have lots of foreign big money buyers and Silicon Valley high tech purchasers and that’s the market.

yes, the Bay Area is largely driven by the equity markets, and not just the big name IPOs like Twitter, etc. Even the established tech companies like Oracle give out a lot of stock options and restricted stock, and when share prices are up, those options and stock are worth a lot more money, money that flows into housing. I have experienced it myself – my options went from +400k in 2007, to literally worthless in 2009, back to +400k today. There are probably thousands like me in the Bay Area (and more senior execs have much bigger swings – “losing” and “gaining” millions based on the markets).

As long as the Fed keeps the stock market inflated, Bay Area housing will remain hot. If we see another 50% correction in stocks, Bay Area housing will suffer greatly, as it did during the last bubble (and don’t believe the hype, SV house values declined as much as they did in other parts of the country – a decline from $4M to $2.8M is still a 30% decline).

WHEN WILL THE NEXT STOCK/HOUSING CRASH OCCUR? THAT’S WHEN I WILL BUY. FOR NOW IT IS CASHOLA.

The housing market historically crashes *after* a recession is in full force. There is no rhyme or reason to when the stock market will crash.

Generally a debt created asset bubble crash leads to the depression/recession. The majority of crashes were a loss of credit confidence of the ability to carry the debt once the underlying asset can no longer generate funds to cover the cost of the debt. Historically, housing was not the asset bubble that crashed (except for 2007) but now we are in new territory where we have a stock bubble, a bond bubble, a housing bubble, an art bubble, an antique car bubble, a tulip bubble, etc. Eventually all bubbles crash but predicting how and when is purely an art and not a science…

Oh Builder, if we only knew, we’d tell you. Or keep it to ourselves. Good luck.

On the subject of building, in the metro adjacent to mine a new development of roughly 300 SF tract homes was announced a few weeks ago (metro holds about 400k).

The hitch is that the developer is building homes that are priced at 45-100% of the current median sales price (and 5-8x median family/household incomes.

So even the development that is happening is trying to pick off premium buyers, not to meet the sector of the market where demand actual exists. And it’s not that there’s a shortage of homes available for sale at the price point they’re building at.

For multi-unit buildings, I get that small mom/pop developers can’t compete, but it is a bit more surprising there don’t seem to be more small-scale redevelopments under way building smaller homes in the 3-4x income range or that no larger developer wants to make a run at developing in the price range where the pent up demand seems to be.

If there is no profit, there is no building taking place. If you consider that price of land went up, cost of construction materials went up significantly, cost of labor for skilled labor went up if you add some mark up for the builder, there you get the price.

There is a fact that construction is at decades low. That tells you that builders have razor thin margin. People who come up with the ratio of so many times the average income for an average house don’t understand business. If builders don’t make anything to keep that ratio, that means they stop building.

If they stop building, rents go through the roof due to shortage (in time). Based on higher rents, investors will buy for returns. That is exactly what we are seeing.

It is true, that young people can stay with parents, that parents move with children, in the end there are only so many people you may cram into a house. If people don’t like the clown houses, then they move out of state; we see that too.

I agree that investors are buying for returns. The problem comes in when better returns start to be found elsewhere. Who knows when that will happen, but when it does, they’ll be running for the exits. Just like the casino, when the payouts get thin compared to another casino, the herd will leave the building.

“There is a fact that construction is at decades low. That tells you that builders have razor thin margin.”

It also tells us that the demand isn’t there. When the demand isn’t there, you either adjust your business model to bring costs down or go out of business.

“People who come up with the ratio of so many times the average income for an average house don’t understand business. If builders don’t make anything to keep that ratio, that means they stop building.”

The two inform each other. The income level is an input into the general price level and vendors (outside of monopolies and cartels) either adjust prices to a supportive level or go out of business. Builders can’t just “stop building” forever without financial consequences. The only hope would be if demand above a certain price level picked up soon enough down the road.

“When the demand isn’t there, you either adjust your business model to bring costs down or go out of business.”

This is an old business. Out of so many hundreds or thousands of companies you would expects that at least one would be able to figure how to cut cost. For materials and land they are price takers. For labor it is true that you can easily cut cost in half by hiring “monkeys” but the quality of the construction will be “trash”. If you are a low price builder and that is your business model, then you’ll spend the difference in law suits.

A respectable builder who wants to deliver quality to his clients and have a good reputation hires skilled workers/craftsmen who are twice or three times the cost and happy to find them. They build a house which decades later looks like new. It is a big difference between minimum building codes and best building practices and that is reflected in cost/price. It is like the Doc said “people have champaign taste on beer budget”. Most people ask about the price per sq. ft. without thinking about the difference. You can write pages and pages about those differences and most people never thought about or maybe they can name a few.

” They build a house which decades later looks like new.”

It’s a good conversation, and I do appreciate the comments on both sides. What I meant mostly wasn’t cutting price by skimping on quality (since I see a fair amount of ‘higher end’ newer homes with fairly dubious craftsmanship).

For example, in Portland one thing you see quite a bit of is larger lots with run-down buildings being bought up for $150-180k, torn down, subdivided, and rebuilt into two new ‘skinny homes’ that will combined sell for $550-600k. And they sell despite the relatively low curb appeal and some craftsmanship that’s not always very crafty.

And I don’t have a single simple solution either, but one thing I was expecting was more town homes, or smaller SFH. There’s no question the 2000+ SqFt model commands a premium, but it may not be where mass demand is.

Certainly developers need to cover costs and make a margin, but BS is correct that you A) also need to be able to sell what you do build, and B) you do need to build something or you don’t have a business at all.

Though anecdotally I see quite a few larger developers that have been conglomerated into larger property development/mgmt corporations. In which case perhaps the corporation overall can maximize profit by not doing development. Not sure.

When you see lots of construction taking place, that is a good indicator that house prices are well above the cost of construction. Till then, you pretty much buy at cost.

I also agree that the government affects the house prices through many channels:

1. Easy money affects the price of land

2. ZIRP makes the value of dollar lower – therefore higher prices for materials due to more exports and less imports.

3. Easy money affects the demand side, too. Lower interest, means higher prices (somehow). However, it doesn’t influence too much because dismal employment numbers; that is the reason for lower number of sales.

I guess despite the so called demand for the type of housing you speak of, developers don’t see enough profit potential to build that type of housing. You see a similar issue for section 8 where demand for such units has been skyrocketing, but a lot of landlords don’t want to get involved with the hassles related to the program since the tax wrightoff may not cover their own costs. It has now become easier to get market or above market rates for their units & unless there’s a serious ecconomic downturn, don’t expect too much in the way of rent consessions.

I have been renting for several years now, sitting on an inheritance that would permit me to purchase a decent home in the Los Angeles area. I’ve been waiting for the real estate market to return to more reasonable levels. I’m about to throw in the towel and buy something. Why? When I see tens of thousands of dirt-poor kids and families walking across our Southern borders, getting arrested, fed, housed, and often turned loose at bus stations across the Southwest – it occurred to me that the only way the government will pay for all this generosity is to print more money and devalue the dollar yet again. I don’t want to be sitting on a pile of this constantly devaluing paper any more!

My advice, walk you own path, do what’s best for you and don’t waste time on regrets if you aren’t making a mint off your home. Live your life. Nobody can give you the advice you need for that but yourself. Sometimes you lose money, but if you’ve had a good experience, consider that payment and call it even. Sometimes, worrying too much about money and the “who wins, who loses” game can cost you more in stress and upset than the farcking money is worth. My opinion only stated here…

Refreshing to hear someone else say it!

I am looking to buy in North County Coastal San Diego. Generally speaking prices in this area are about back up to peak ’06 depending on the neighborhood. However with low interest rates, my mortgage payment will be about 20% less than in ’06 for the same house. When adding inflation into the calculation, prices in terms of payments are down closer to 30% from peak ’06. Prices are not that bad in real terms, it is an inventory issue with a real lack of quality inventory to choose from. We might see some erosion in pricing later in the year and next but hard to imagine anything dramatic, especially due to lack of inventory.

I purchased a property near peak in ’05 that was down 35% but now is only down 10%. Two friends also purchased at peak and both are about even now on value and they have been paying down their mortgages for 10 years and have solid equity with locked in fixed sub 4% mortgage re-fi’s in ’12. I look at our situations and think wow, we are in damn good shape even though our timing could not have been worse – we bought at the majestic insane peak but look how it has played out. Sure lots of fools got in over their heads and got crushed – but the moral of the story is get into something you can afford and let time do it’s thing. Otherwise you are on the sidelines trying to time the market with your crystal ball while playas are in the game paying off their property.

Otherwise you are on the sidelines trying to time the market with your crystal ball while playas are in the game paying off their property.

Does that make that a “Playa Vista”?

Falconator – just so you realize. It took everything the Fed and Govt had as well as a completely rigged market with rewritten rules to get those who bought at the worst time back to those levels. Fundamental reality is that the buyers and lenders should have been completely wiped out and the world would be in full scale depression (real deflation year-to-year similar to the 1930s and even they eventually went with a foreclosure moratorium).

Don’t think for a second that fundamentals don’t matter, there has been a bailout of biblical proportions alongside changes to rules and outright lies to make this “kind-of” work out. And in the end, it is everything they can do to hold prices up right now in the hope that the real economy gradually gets its feet underneath it again some 6 years later.

I’m not being a bear so much as a realist and in general your point is absolutely right and well taken, just don’t lose sight of all that has gone into make the numbers work out here and we aren’t close to having worked through the restrained backlog of inventory or near anything resembling a legitimate housing market yet.

Agree re the impact of govt intervention Slim. I have little doubt that the govt and other PTB will ever abandon support for housing however, so the game goes on. The fundamentals actually could not be much better these days with the elevated level of cash deals and the diversity of buyers and the elimination of radical NINJA type loans.

I think sitting around and waiting for a crash is a questionable call. If your personal fundamentals are solid, it is better to be in the game than on the sidelines.

The market is still burning hot in my area. Much to my shock and surprise. The same floorplan as the house I rent came on the market on Friday. Priced 40% ABOVE 2012 prices. That afternoon driving home from work I saw 3 different people and agents lining up to tour. $379,000 for 1500 sq. ft. No upgrades except laminate “wood”floors. Tiny backyard, on the main drag into my neighborhood, not tucked away on a loop like my rental.

So the cost of buying this little house vs the $1650 a month I pay in rent. How does that make sense? And I have no repair expenses…. Insanity. I will continue to rent and bank away a ton of money. I am in no hurry to buy at that cost.

Who thinks it makes sense to buy and pay out, what? $2300 a month in carrying costs, + maintenance??

You do know the math isn’t that simple when making the comparison between renting and buying, right? If I was in that situation and I thought that house prices would be stable and I thought I’d be there at least 3 years, I’d buy. But on the cul de sac 🙂

3 year’s worth of rent is just about $60 grand.

The way I see it is if I was to buy that property at $379k, put 10% down (there’s $38 grand out of my cash savings gone right there – I would be borrowing say $341k, at the end of three years I would still owe $322k.

So even if the housing market does not tank, but stays stable I am minus a ton of money.

379k

38k Less deposit

7k Less closiing costs

24k Less selling costs in 3 yrs

= 310K

and I still owe $322k on it. Makes me UPSIDE DOWN.

Plus that 3 yrs I have been paying circa $2500 a month to carry the property PITI & PMI, and been lugged with maintenance and repair costs.

When I could have been paying $1650 in rent and saving the difference.

Makes no sense to me. I’ll buy when I can at near rental parity.

Calgirl

Your calculations are a bit off.

If the house is sold after 3 years for 379,000 and you owe 321000 then you get 58000 back.

58,000 – 6% selling costs (22,700)= 35300

35300 – 7000 closing costs= $28300 left

The interest alone is costing you $39000 over three years. The property taxes essentially are covered by the mortgage interest deduction.

But renting during the same period is costing you $59400

36 months * 1650rent = $59400 gone

So for owning $39000 + $9700(lost downpayment) = $48700

Renting costs are $59400

Taking maintenance into account you are probably even after 3 years.

Of course the big unknown is rent payments, they only seem to go up.

“But renting during the same period is costing you $59400

36 months * 1650rent = $59400 gone

So for owning $39000 + $9700(lost downpayment) = $48700

Renting costs are $59400”

In both cases (rent+save vs buy+don’t save) you may end up with a gain. The difference is that renting affords more flexibility to adapt to changing financial conditions and purchasing affords more flexibility to renovate. In the current climate, financial flexibility is prudent for all but the wealthy.

There is an exception to this but most people don’t cash out high, wait and then buy back in at a discounted level. What they do is immediately buy back into the same level they just sold into so the gain is not realized. They may borrow against perceived gain, but most don’t invest those borrowings to arb a profit, they usually use it to renovate or consume.

“the mortgage interest deduction”

It’s time to stop with the interest deduction as a given nonsense. First of all, it depends on one’s tax situation as to if and how much of an advantage it may offer so it’s inappropriate to make general conclusions. Secondly, don’t expect it to stick around. Just ask the IMF’s Christine Lagarde, one of the few bureaucrats in the financial world to publicly state the game plan.

http://www.foxbusiness.com/business-leaders/2014/06/16/imf-lagarde-iraq-oil-shock-may-threaten-us-economy/

http://www.imf.org/external/pubs/ft/scr/2012/cr12214.pdf — Page 62 “Abolishing mortgage interest relief would also improve the progressivity of the income tax code.”

Folks, it’s in the works. Some might try to downplay the IMF’s role in domestic policy – that’s bogus as the IMF is conferring in the same private dining room as the Fed and the BIS.

“Of course the big unknown is rent payments, they only seem to go up.”

Just like home prices, right?

Thanks BB and BS for adding the details. It’s always surprising to me when folks that can do the math don’t do the full equation….

Sitting on the sideline and wait? Ask people who did that in OC 20 years ago, guess what? Those people are still WAITING!!!

Once again, we have to face the facts, California will always be expensive, compared to other states. You have to PAY to STAY, to live in Cali…PERIOD.

The day you see a house for sale in Irvine, CA for $125,000, is the day you’ll see 125,000 people bidding on that house.

Listen, there is a reason, why other cities have homes for sale for $50-$80,000….HURRICANES…..TORNADOES…….BITTER WINTERS…..FLOODS, Who wants to deal with that every year?

They don’t call California, The GOLDEN STATE for nothing…..#ijs

I’d rather ask the 7+ mio who are still underwater by 100’s of thousands.

Please, you’re embarrassing the bulls.

#always

#period

#promisedland

#crystalball

#hashtag

Goldie…It has been a dream for many not only for CA. but for anywhere that climate not weather is the norm, to move to these places once the prices get to where they can afford them???

I have many relatives who live in Chicago, heard the same story for over 40 years now, someday when prices come down we are moving to a sunny place.

One of these relatives died recently, the spouse tells me, think I will sell everything ,cash out, and move to nicer climate and digs, want to bet it never happens?

Robert…..Great Point.

Fact 1: It’s different on the coast now than it was for our grandparents. Prices there were always higher than inland or the flyover states, but the difference is larger now, even in a normal market, and that’s a relatively new phenomena. In the past 20-30 years, things have changed on the coast. Population density and employment, mainly. Prices will always be much higher there.

Fact 2: Prices fluctuate. There are good times to buy and bad times to buy – even on the coast.

Fact 3: The coast is currently WAY overpriced, even for the coast.

As a realtor you can’t admit or even believe Facts 2 and 3, but that doesn’t make them any less factual.

20 years ago no one sat on the sidelines and waited to buy in the OC, because it wasn’t a stupid time to buy – as it was in 2005 and as it is now.

John D your post was full of facts, logic and devoid of emotion and confirmation bias.

In other words it has no place in a discussion of housing 😉

“In other words it has no place in a discussion of housing”

Exactly!!! So take your facts, figures, pie graphs and non biased comments and get the F outta here!!! You will be welcomed back with open arms if you talk about “feelings”, “experiences”, “perceptions”, “fantasies”, “unicorns”, “rainbows”, and “how you got rich off of CA RE”…

I’m a California native who hasn’t made the wisest of decisions when it comes to real estate. I got hosed during the last housing crisis and don’t want to make the same mistake twice. My question is if I plan on staying here for the long haul does it make sense to buy now or rent hoping the market will come down. I want a decent place to live with a back yard for my kids. I have the 20% down but my budget around 500K won’t buy much. For me it is not all about the investment. I just want a place I can call home where my kids can grow up. I’ve worked in the movie business for close to 20 years so moving out-of-state until retirement is not an option. Any advice on what to do?

I’m not a hard-liner on renting vs. buying – we rented for years, actually just bought a place, but we were *extremely* picky, and walked away from multiple situations where we felt we were not getting the value we wanted. You can always “save” money on housing, regardless of whether you’re renting or buying – move further out into the burbs, downsize, etc. but you have to think about what it is that you want at the end of the day, and work through the numbers. What’s it worth to you to have a backyard? Is your job stable and can you swing the monthly payment over the long haul?

The one thing on which I do feel strongly… if your kids are in school, I’d suggest limiting your search to good districts. I have colleagues who bought in the “hip”/affordable areas before they had kids, and are now faced with sending their kids to really crappy schools vs. paying $20K+ per year per kid for private. Talk about throwing money away! If the monthly payment is an issue, I think renting in a good neighborhood is far better than buying in a questionable one.

Honestly I feel bad for people in your situation. It seems you’re a responsible buyer looking for a place for all the right reasons, but you’re right in that price point that interests the “investors” and you would be paying through the nose to rent a house too.

Managing the school situation is very difficult. There are some advantages to staying mobile so you can take advantage of the best public school available for your kids based on their ages.

Dan… As a person who has owned a lot of residential and commercial investments in my life, 4 words come to mind “you got a problem.” This scenario you just laid is the same for millions of people who live in very “tall cotton” places.

Look for anybody to access your problem they need to know your location in CA., how far you are willing to drive to obtain a decent house for 500k. If children are involved because of schools, your hours of work, do you have to be at work at 8 am for example.

Lot to play out for you, if you could move to lets say Las Vegas or Phoenix more doors are open for you.

Plenty of rental houses can be called a home and offer back yards that kids can use.

I feel for you Dan. Have had the losses you describe myself. Frankly, we don’t live in the time anymore when “home” means buying a house. A great lesson for your kids BTW – a reminder that a building is not their “home”, the family is their home. Doesn’t matter if you live in a tent. your family is home, the wooden structure is merely tradition. I’m sure I’m older than you, and I have the same feelings about a house, but really the family is the thing. You’re kids would rather have you taking care of yourself and your wife in old age retirement than having memories of a building. They’ll have memories of where they grew up, but most important memories of what home was like

Great comment.

I look at many, many properties, without question these homes on the market are not in very good shape, RE agents desperate for sales are still talking out of both sides of mouth as usual. They tell sellers I will take the overprice listing ( the market is hot???) and tell buyers to wait till the over price house gets disgusted and swoop in and offer very low, this theory is not playing out.

Investors are now finding very few good properties for sale, homes in bad zip codes are not what they want.

Traditional buyers are not in the investors league, they think they are but can’t qualify or compete for the very few that remain good homes in good locations.

Traditional buyers are buying homes in need of work, this can get expensive, but this is all they can get for the money and jobs they have. RE agents show them the junk they can deal on, these agents don’t have enough real buyers to make a living otherwise they would drop these folks for the money buyers.

This is what I’m finding every weekend, the standoff of good houses, in good zip codes, sellers that won’t budge on the price, and the buyers who want to steal at 2008 prices, now accepting bad homes, in bad zip codes, just to get something.

What’s up with this stealing business you keep bringing up? Perhaps there’s some axe to grind or misuse of hyperbole. It’s not stealing if it’s sold.

BS… when a seller puts in upgrades to bring value to their home and the buyer also benefits by receiving a upgraded property, then everybody should be happy, except now buyers want to play the 2008 nonsense steal your home then turn around sell it at 2013 price, they are killing the market, they want it all, especially these Canadians buyers..

So I say screw the buyers, if you can wait it out why give them anything, they should have bought in 2008, now they missed the boat and want to take a row boat to catch up to the luxury liner, let them sink or pay the adjusted price, 2008 isn’t going to happen.

To that I say the seller is placing a bet on an outcome if they are renovating for gains. If they find a buyer willing to pay their price, then so be it. If they don’t, then so be it. That’s the marketplace. It’s not stealing if the seller accepts the buyer’s price. My contention is with framing it as stealing. I call it making a bad bet. That’s the reality of gambling.

Another thought – sellers should be sending thank you letters to the banking cartel for their role in restricting inventory. If it weren’t for such meddling, these sellers would have far more to worry about.

Little robert sez: “So I say screw the buyers, if you can wait it out why give them anything”

And so the standoff begins again.

For those with short memories, there was no glut of cheap wonderful homes in 2008-2011. Owners, by and large, when confronted by falling prices, simply hit the Pause button and decided to wait for a more opportune time to sell. So inventory dried up, and what little was available was either really beat up or often wired straight to insiders. Then 2013 rolled around and prices rose enough so that greedy homeowners (and the realtors who love them) came back out of the woodwork. Sadly, though, last year’s mania appears to have been short lived and the potential sellers are stuck again with buyers who actually care about pricing.

So now, as robert says, they will pull their horns in and wait another few years. Heck, sooner or later dollar devaluation will provide them with enough of a nominal price increase that they’ll get the selling prices they want – who cares if it’s in devalued 2020 dollars?

Me, after playing one side of the standoff for the last decade, I’m getting sick of the whole business. Rather than buy a big place here at inflated prices I’ll retire and likely take my millions out of state, buy land and build my own place on it.

“Owners, by and large, when confronted by falling prices, simply hit the Pause button and decided to wait for a more opportune time to sell.”

If by “Owners” you mean the banks who got bailed out by mark to market suspension and stopped processing foreclosures you’re right. There’s just one little problem. We still don’t have anything near a “market” in Real Estate. The whole thing’s being held together by scotch tape. The FED is fighting market forces on all fronts and is losing.

No rational housing bear seriously believes Santa Monica is going to get a 40% haircut in a crash. But we are headed for a period of higher interest rates, The FED has telegraphed as much. It’s inevitable. Without some form of rate normalization inflation will destroy the dollar system. So how are we not going to see a significant price reduction, especially in the IE and other Non-Prime areas when incomes are lower, interest rates are higher and rents are lower due to increased inventory and sales prices are lower due to collapsed investor demand brought on by lower rents.

14 years after the greatest “Greenspan Put” and we still haven’t dealt with the consequences of pulling that demand forward. The bill is still due and whether we pay it off in one big adjustment or, more than likely, another echo bubble or two it must be paid.

An excellent post AS. Succinct and factual as to current sellers and a great idea on moving.

Was it not for close family ties here in So Cal, I would have invested in setting up a self sustaining ranch out in the sticks years ago and moved my family out there.

“The whole thing’s being held together by scotch tape.”

I’m envisioning the “Magic Tape” frosted variety of many pieces laid over the top of one another, not the transparent stickier type. Gotta obscure those seams and cracks.

Then again, Scotch is a premium brand, this is more like President’s Choice brand or a dollar store knock-off.

It is neither scotch tape nor magic tape. It is being held together with pixie dust. Remember the “Full faith and credit†clause?

Full = Complete

Faith = Belief without evidence

Credit = Ability to have access to goods and services before payment based on the trust that payment will be made in the future

Translation: The citizens’ complete belief without evidence and the ability of the Federal government to have access to goods and services before payment based on the trust that payment will be made in the future.

This is what they tell us! Do we really need to know anymore?

Mwhahaha ‘stealing’.

Is someone finding buyers in the market aren’t offering to meet their inflated bubble asking prices?

Add value? We’ve seen house price crashes wipe out decades of inflationary gains in the past. 2008? I’d like you to try on 1988.

Welcome to the start of the crash 2.0.

The Doctor’s articles are sometimes a little misleading. 32% of sales is not that much if sales have tanked, which they have. The smart investor money is no longer in the market. There are no “returns” these days unless you buy at auction for cash, YOU are the contractor, and you price it to sell fast. Cash buyers at current market prices are NOT investors, they are idiots. In my neck of the woods (Temecula), inventory is higher than it’s been in over 5 years, homes priced at what was the market rate several months ago are getting exactly ZERO offers, and listing price decreases are more than double what they were at the beginning of the year. Those price decreases are next month’s comps. We are at the brink of a long, slow downturn – not a tank, in my opinion. The last bubble burst because the rug was pulled out from under it (no more easy money), which isn’t happening now.

The inland empire foretells the future of the coast to some extent, but don’t wait for a 40% drop there because it will never happen.

John D.. Very good thought out post.

“The last bubble burst because the rug was pulled out from under it (no more easy money), which isn’t happening now.”

Should read “isn’t happening yet”. FED forecasts 2.25% FED rate by 2016 and Leslie Appleton Young sees 6% mortgages by then. We are a year and a half away from the end of easy mortgage money according to the people standing next to the levers.

Flipping is dead for the most part as you said. Once the SFH rental ponzi breaks down under the weight of market forces, the rug hath been pulled.

#never

As someone who just moved to Temecula, I’m happy I’m not the only one out here who feels like this. My wife and I went to school in the Bay Area and had lived in San Francisco since 2008 when we graduated. The wife grew up in Temecula and most of her family lives in S. California so when I got recruited for a job out this way, we figured it was a good opportunity to move close to family and raise family in an affordable area.

We had enough for a 20% down in early 2013 when we could buy a new home for 350k but we decided to wait and see which area worked best for us. We’ve been renting since and looks like we plan to rent a little longer while we wait this out. We looked over in Morgan Hill in early 2013. Brand new McMansions were going for 350ish and a year later are pushing up against the 500s. There is a new development off Butterfield Stage and Rancho California with starting prices in the 600s. The Roripaugh Ranch development which was started in 2006 and stopped, began building again in 2012 with first homes selling in 2013. Starting prices in the low 400s but average sales price over there is close to 500. Looks like building over there is slowing down now.

I like this area but I refuse to buy a house for 450k when it was sold for 200k as a foreclosure 5 years prior. While we probably won’t see a big crash here, I think were in for a slow decline over the next couple years. I just don’t see the fundamentals backing up these prices.

Thank you for your replies. I have to be at work super early so I am able to avoid traffic for the most part each day. Location is a definite must on my list. We currently rent a townhouse in Oak Park which has one of the top rated school districts in the nation. The problem is that homes are unaffordable in this area for the average guy. I make around 100k a year but it’s just not enough. I’d have to move back to the Valley to afford a starter home. As a surfer for over 30 years moving out to Palmdale is also not an option. Just would love a home for around 400k in Agoura Hills. I guess my biggest fear is to buy a dump for 500K in an area that I really don’t want to live in and then the market tanks and I’m stuck with the house.

Well… you’re already fairly close to where SFRs actually do start getting more affordable. If you’re at 100K HHI with a spouse you probably won’t benefit too much from the deductions associated with buying. No idea what the house rental market is like out where you are; I do know that it is *terrible* on the westside – at least when people try to sell their “crap shacks” they fix them up a bit, when they rent them out they couldn’t care less, and they still charge insane rent. Maybe you do want to consider renting a house if it makes sense in that area, especially if it would relieve you of anxiety. (Although reading this blog can sometimes be unnecessarily anxiety-inducing. Take all comments with a grain of salt.)

Know your location very well since I had many properties in Ventura County. Oak Park is a great school district but as you know pretty much out of control on prices.

Have you consider Moorpark or Simi, always someone there in trouble with payments. Just a suggestion, good luck

Don’t know where Oak Park is. I was in film as well, moving away because retired now. Refer to my previous post – home is where the family is, not a structure. You live at a time when the “right thing to do for your family” is impossible. Deal, dude! Times change, buying more than you can afford can break up the family no kidding. Swing free, make the family the heart of your home, not a building

No offence but why the F would anyone come to a housing bubble site expecting advice on purchasing a home? The reality is that we are in the throes of a massive debt induced asset bubble and housing is one of the assets. No one on this site has any idea what is going to happen next. No one on this site has any idea when the next shoe will drop.

The current financial system is a zombie system which no longer provides the service of allocating capital. The current financial system is cannibalizing the market on which it depends. It is like the scenario when you run out of fire wood. You have two choices, go out and get more firewood or you start to burn the furniture and when you run out of furniture you burn the structure. The original purpose of the fire was to heat the house but now there is no house to heat.

Governments are buying their own debt. Corporations are buying their own stocks. Banks spend all their time buying and selling stocks based on insider information versus loaning money. Worker participation continues its long painful decline. The definition of GDP, inflation, unemployment, Dow, etc. changes more often than I change my socks. Every market is highly manipulated. Thank God the theory of supply and demand has been debunked because we would be really lost if where trying to predict price based on the debunked theory.

So is it a good time to buy? Sure, why not? Nobody knows what anything is worth anyways. So make it up just like our banking system. Mark your assets to your own fantasy and pretend your debt away. Better yet, when you are a little short on cash, just change the running balance in your check book. It’s all good!!!

Relax What? take a deep breath, step back, all the man ask for was advice, I doubt he

will act on it, he will give further thought of his situation.

Of course none of us know when the grim reaper is coming either, just like a

investment who knows really, I still go for test, screenings and ask the results,

maybe I still die soon after?

Once again the point of my comment evades little “r”…

let’s all bow down to the all mighty petro dollar. print and spend and lend to grow the debt based economy.

Nice post What? Many on here feel the same way, but most people reject these concerns. I have witnessed this repeatedly. Especially lately it seems the average Joe has built a reality distortion field that protects them from bad news. Maybe people are just fighting back pessimism, or perhaps they just don’t care because if anything bad happens the fed and gov’t will step in.

Anymore up is down. GDP dives greater than 1% and the economy is booming enough to continue taper. Americans save too much because they are aging hence low interest rates, yet we are too indebted. Housing has “recovered” to previous house valuations and now sits at price levels where people again can’t afford the mortgage even with low rates. Exciting times. What will be the trigger? Recession? War? Oil? Earthquake? Thing is with everyone so heavily leveraged it takes less and less. I can’t what to hear, “no one could of predicted this.”

Agreed that there seems to be a cognitive disconnect in the comments asking for buying advice. It’s like telling a desperate girl that he’s not that into her and then she immediately asks what she needs to do to win his affection. Some people will learn the hard way.

This is not the time to “relax” and chill-out man. This is the time to get up off of one’s apathetic ass and pay attention to the details.

If some prefer or benefit from complacency, fine for them. Meanwhile the rest of us will continue to call out the B.S. because that’s how things get changed.

This Sherman Oaks house not only has a red front door, but in case you missed it in the photos, the description specifically mentions it: “Manicured lawn and flagstone pathway lead to the rich red front door.”

http://www.redfin.com/CA/Sherman-Oaks/4435-Katherine-Ave-91423/home/4830837

Don’t buyers realize they can paint a door themselves — any color they like?

House was sold for $660K in April 2006 — and flipped 3 MONTHS later for $770k.

Now selling for $779k — Zillow estimate $853k.

Description also says this house will “tug on your heart strings.”

Description also says this house will “tug on your heart strings.â€

—

Must be the strings that will rip it out of your chest once the bills start arriving.

Ohmygod, a pale yellow 1950s vintage frame ranch with a fire-engine red front door.

I don’t even know what to say, and nevermind the price.

Would you rather have them print the truth “Tug on your purse strings” or as What? points out stick to the emotional slight of “heart”?

Love the code words generous, spacious, this home is 1900 sq ft, at 799k and the age of the home, location which also seems to be within a block of a major street, I would use the code words, not warranted or worthy of 799k?

Speaking of buyers, Sunday went to a open house, it was 3700 sq ft 4 bed 3.5 baths excellent condition 7 years old, in comes the buyers, first thing out of their stupid mouths, foyer to big, who needs 4 car garage, pool to fancy, lot of wasted space(?).

That is why they tell the owners not to be home, you just want throw folks like that out of the house, because they can’t afford it, they go on the hate trip.

Not really a hate trip IMO, but statements of fact. That house is too big for one 4-person family. If they buy it, better figure in the cost of a housekeeper at least once a week, probably twice a week, or the woman will feel like a slave. Hard and expensive to heat and cool, family members far away from each other (believe me this makes a difference when you have kids) so these places aren’t as wonderful as they look. About that huge foyer – and I’ve been there – how the heck you gonna change those lightbulbs and clear out the cobwebs?

I’m one of those who would love to buy….Recently sold my home in Virginia to move back to Pasadena for family reasons, but I’m NOT going to try to compete in this market. I’ve finally arrived at the point where I’ve just given up and decided to rent for the forseeable future. We have the cash saved from our recent sale and can afford a nice down payment, but we’ll just bank it for now. My wife and I are in our 50s…..now we have flexibility and aren’t tied to a specific house or neighborhood, not to mention tied to the massive debt. Yes, rents will undoubtedly continue to rise…so we’ll just keep moving on as necessary. If we find a nice deal on a fixer, we may reconsider, but other wise, screw it

Agree, could make a big downpayment thanks to selling my last place in 2007 but will not buy into a bubble. Wasted a year trying to buy in 2011/2012 but it was basically hopeless, made several offers but was ignored every time as a flipper or specuvestor offered 100% cash. Renting more or less happily in the meantime and living in a part of town I like, may give buying a shot again after Bubble 2/0 pops and if it looks like like regular buyers have a decent chance of having a solid offer considered.

St63, sounds smart to me

Leave a Reply to Tired of the BS