The Lords of Money Speak: Even the Prime Will Fall. Lessons From the Great Depression Part XV. The King JPMorgan Speaks.

When the House of Morgan speaks, people listen. There are very few banks that carry an aurora of royalty like that of JPMorgan. Unlike our brethren in Europe or Asia, long historical banks or families simply do not exist in our nation’s short history. The life of American financier, bankers, and art collector John Pierpont Morgan with the ability to merge Edison General Electric and Thompson-Houston Electric into the mega conglomerate General Electric, is one of great historical reference and study.

Morgan entered banking in 1857 in his father’s London location and then moved to New York City with the knowledge he learned. During the Civil War Morgan was approached to purchase old rifles being sold from the army at $3.50 each. One of Morgan’s partners retooled the rifles and sold them back to the army for $22 each. This was touted by some as a scandal but the army knew the weapons were retooled; what this highlighted was the ability of the government to spend more than it should and also, brought to light inefficiencies in large bureaucracies.

This is part XV in our Great Depression series. Below you’ll find the latest five articles:

10. The Sham of our Current Unemployment Numbers

11. Understanding the Impact of Asset Deflation and Consumer Inflation.

12. Is the DOW now Tracking with the California Housing Market?

14. Bank Failures.

Morgan had an uncanny ability of taking over businesses and reorganizing them. He had a reputation that would be similar to something of a Warren Buffet in our day and age. Yes, they played in the economy in different roles but their ability to be successful is born from the same ability to make businesses work.

During the Panic of 1893, the Federal Treasury was nearly out of gold. Yes, they actually used gold back then unlike our current system where money is made up out of thin air. During this panic the President at the time Grover Cleveland asked Morgan to help supply the U.S. Treasury with $65 million in gold with half coming from Europe to restore the treasury surplus. This move saved the Treasury. During the 1896 campaign Republican William McKinley ran under the gold standard platform.

It is incredible to think how much power Wall Street had back then. One year before his death in 1912, Morgan testified before the Pujo Committee, a subcommittee of the House Banking and Currency committee regarding finance and banking. As it turned out, a small group of financial leaders were abusing their public trust and consolidating power to the hands of an extreme few. Morgan died in March of 1913.

Many books have been written about J.P. Morgan. His life is more complex than a single article can sum up but suffice it to say that it is an intriguing one that has left a historical impression on the life of American finance. The fact, that the House of Morgan was the one who stepped in to save Bear Stearns with the aid of the Federal Reserve should tell you how the American finance system is structured. It wasn’t Bank of America that stepped up. Maybe to soothe their ego they took over Countrywide trying to gain some love from daddy at the Federal Reserve?

Now why is this relevant to what is going on today? Well it is relevant because there are very few institutions that have the ability to tell you how it is with little fear of repercussions. Many firms including the now taken over IndyMac Bank were assuring the public that they were fine up until the day they were taken over by the FDIC. Even Bear Stearns was telling the public all was well before that faithful weekend when they were sold off for a token $2 a share. Yet JPMorgan Chase & Company with their current CEO Mr. Dimon recently came out with a few simple words that essentially sum up the current situations. Mr. Dimon told analysts on a call that mortgage problems were now spreading to prime mortgages:

(Housingwire) “Prime looks terrible,” he told analysts on the call. “And we’re sorry, and there’s nothing else we can say.”

The company currently holds $34.4 billion of jumbo mortgages, along with $2.5 billion of Alt-A mortgages. Net charge-offs among prime loans in the second quarter rose to $104 million, more than double the $50 million recorded just one quarter earlier. JP Morgan jumped in headlong into jumbos and Alt-A mortgages during 2007 – obviously an ill-timed bet, given where the market has headed.

“We were wrong, we obviously wish we hadn’t done it,” Dimon told analysts. “We’re very early in the loss curve.”

This is as honest as any top CEO has come out in the recent housing debacle. To take ownership of a blunder in your company plan. The fact that we are now being told that “prime looks terrible” is simply another way of saying we are now all in this mess. No one in this country will be able to hide from the hideous repercussions of this housing and credit bubble bursting.

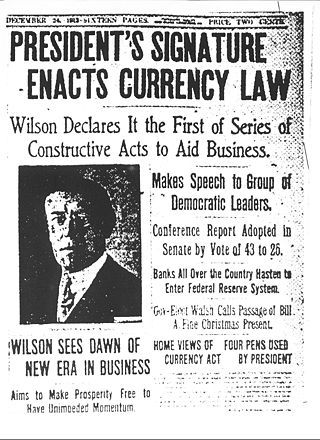

Yet it is important not to setup a system where we are doomed to repeat similar mistakes in the future. The knee-jerk response to trying to save Fannie Mae and Freddie Mac, trying to symbolically go after a select few naked short sellers, and making a public spectacle of the public’s money is coming to an end. The Federal Reserve came into existence signed in by President Wilson in 1913, after the death of J.P. Morgan:

The Federal Reserve Act spells out their purpose:

“To provide for the establishment of Federal reserve banks, to furnish an elastic currency, to afford means of rediscounting commercial paper, to establish a more effective supervision of banking in the United States, and for other purposes.”

Well they succeeded on an “elastic” currency since it is has been bouncing off the walls these last few years. Should we even discuss the supervision component? The fact the IndyMac Bank is now under the FDIC and other banks are hanging by their nails speaks for itself. The fact that the investment banks on Wall Street are holding a hand grenade of credit default swaps and have essentially insured mutually assured destruction goes to show that supervision once again was not there.

And this goes beyond Ben Bernanke. This stems back to Alan Greenspan who under his watch, allowed the balloon to inflate to the current point of global financial destruction. Anyone thinking that we are out of the woods because a brief bear market rally last week is simply deluding themselves. Take a look at the raw numbers in terms of bad mortgages, foreclosures, bank balance sheets, and you’ll quickly realize that we are standing at the edge of Niagara.

If you want to gain some perspective, it may be helpful to look at a letter of a banking president during the height of the Great Depression:

“This is a shameful and humiliating exhibition. It is uniquely bad. Across the border in Canada, there was not a single bank failure during our period of depression, and one must go back to 1923 to find even a small one. Nowhere else in the world at any time, were it a time of war, or of famine, or of disaster, has any other people recorded so many bank failures in a similar period as did we. We were not experiencing a war, a famine or any other natural disaster. All the economic tribulations we have undergone in the past three years have been man-made troubles, and Nature has continued to shower us with an easy abundance – more, indeed, than we have known how to distribute with economic wisdom.

Human stupidity and cupidity were the taproots of this great financial disaster. Those are evils which will always best us. There have, however, been revealed faults and weaknesses in our banking and investment practices that account in part for the extreme nature of this experience. Isn’t it about time that we began thoughtfully to examine some of the fundamentals of our banking and investment theories and methods?”

The question is, are we going to continue fueling policies that clearly led us into this mess or are we going to finally sit down and examine the actual premise of our entire system? Here in California, it appears that both parties are more interested in getting re-elected than actually coming up with long-term sustainable solutions. I think that is key here. What is sustainable for our nation in the long run? Clearly debt isn’t. Government officials would rather borrow and expect that money will grow on trees. Yet this is checkmate folks. Some don’t like the comparisons to the Great Depression but when I drive down to work and see huge lines of customers trying to get their money out here in California in a desperate panic from an institutions that made absolutely absurd loans, what other comparisons do we have? I think many people for the first time in their lives are seeing housing prices go down nationally (first time since the Great Depression), bank runs, a crumbling dollar, and unemployment that realistically is hovering around 10 percent if we count those underemployed and those who have simply given up looking for work.

What Mr. Dimon is saying is things are as bad as they look. It will take time to fix. Yet why compound these mistakes by giving carte blanche to the institutions that got us here in the first place? The Federal Reserve could have stopped this mess before it got out of hand with Alan Greenspan. He could have raised rates and used his rightful jurisdiction provided by the Federal Reserve Act of supervising banks but instead chose to lower rates and become a cheerleader for adjustable rate mortgages. And now, we want to give the Federal Reserve more power?

Mr. Dimon may have summed it up when he said, “And we’re sorry, and there’s nothing else we can say.”

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Subscribe to feed

Subscribe to feed

19 Responses to “The Lords of Money Speak: Even the Prime Will Fall. Lessons From the Great Depression Part XV. The King JPMorgan Speaks.”

You are indeed the Doctor of the Housing Bubble!

What bothers me is our legislators have lost complete faith in our ability to recover from this thing on our own. It is either that, or that the American Public itself doesn’t believe we can pick ourselves up by our bootstraps and build back what we have lost. I have always been a fighter and I know that I am not alone.

Hiding true inflation with that rental equivalency and basket replacement crap was the start of this. If we could see true inflation, interest rates should have gone up and cooled off this housing bubble. Housing prices, especially in California have a LONG way to fall still. $200 a square foot sounds about right.

could it be, that Usa is now getting paid back form the Asian crisis, where some currency’s were down 60-80%.

So far there have been losses og 400Billion +

BUT who made that money, it didn’t just D”isappear”.

Everytime oil or stocks DROP, is because ” investors” take profit….??

wake up, then some one, some where LOST that Money.

Well ask the mining C E O s, they were selling gold short and thus suppressing the commodity, that there “investors” thought they were – long in.

Even south africa is running out of deep gold – 3-4km’s deep, any now also electricity too…..to pump out the water and cool down the hOT mines 50-80 celsius – and struggle to make a profit at 900$ + .

RATES will go up to 10-15% sooon.

The thing that puzzles me is how our leaders could have failed us so miserably. The housing blogs accurately predicted what would happen. In fact, I knew very well that something was terribly wrong early on, when housing was going up 20% per year in SOCA.

As a layman I knew that things were not right, so how did the experts fail to notice and act? Look at the mess we’re in. It didn’t have to happen. All of the misery, the foreclosures, the debasement of our currency…none of it had to happen.

The FED surely knew what was going on.

Is it that Wall St. and the real estate industries give so much to politicians that they are allowed to do as they please?

The entire mess sickens me.

As to recovering from the mess…they need to keep their hands OFF.

They allowed the money men to make obscene profits on the way up, and now they want to socialize the losses. What bullshit! People should be rioting in the streets. Why should taxpayers have to pay even one penny for a mess caused by the big money men?

The runup in housing ruined a great relationship for me that should have led to marriage and kids, but the housing prices in CA. shot up so much that I got priced out. I will never forgive our “leaders” for this fiasco, and will never trust the government for anything as long as I live.

Great article once again, Doc. And kudos to Dimon for his lack of (as we say in England) turd-polishing. More and more people are starting to realise that this is going to go off the edge of a cliff some time soon and despite the protestations of the CNBC Kool Aid crew and Fed manipulation, don’t have a clue what to do. Whoever wins the election is screwed and will to some extent be made a scapegoat for the worsening economic pain. But the buck stops with every one of us – stop buying crap we don’t need from China and start buying American. Do everything we can to import less oil and export more. Give businesses that export better tax breaks and reduce our balance of payments. And stop the Fed from their dubious methods that will extend the agony with their aspirin in a gaping wound philosophy. America can be great again. Remember 1979 and how bad things were then? Ask not what your country can do for you etc etc. Each and every one of us can make a difference.

What have been people’s experiences with ING Direct? My teenage son researched it and recently switched his savings account over to it from his credit union savings account. I know it’s FDIC insured (ha!–until those reserves are gone; thanks for the info on that, Scott) and it’s paying 3% interest. Maybe a better bet than a money market fund?

As always: this blog=required reading. Can’t wait for some savvy lit agent to get Dr. HB a book deal so I can get my copy signed at a Vroman’s reading.

Well, eloquently stated and put. I think however, it would be a SEVERE mistake to think that the current housing morass is the cause of the overall economic catastrophe ongoing. It is only a PINPRICK in a truly MASSIVE distortion in credit through-out the entire economic system.

Much as it is difficult to visualize an event when part of it, we don’t see how out of whack our current consumption patterns are. I mean, 70 percent of our economy is CONSUMPTION, now thats just re-gawd-damn-dickulous. Economic stimulus checks to stimulate the economy? Thats how distorted our economic thinking is, we believe that consumption precedes production by putting the emphasis on that with “stimulous checks”. ANYBODY can consume, the trick, is PRODUCTION!!!!!!!!!!!!!!!! Our economy needs to produce more and consume less, much less.

No the “rot” in our system goes far beyond real estate or asset prices, it’s due to an un-tethered currency to anything tangible. Our very values both as individuals and a society have been skewed so that we cant see value anymore, because we’re so detached from it. The effects of that are, rampant relativism and various fuzzy thinking projects eg. global warming crisis, save the polar bear, etc.

Lads and Lasses, consider yourself dubiously fortunate to see the actual sinking of a formerly great and prosperous economy. Hopefully this epoc will be correctly documented as a cautionary tale for future generations.

PS: Hows that for doom and gloom?

In regards to ingdirect, I just moved my down payment money into capital one’s high interest savings account at 3.5%. Ofcourse I won’t let it get over 100k before I open a 2nd with my wife’s name. I figure I might as well make a couple bucks while I wait for our raft to fall off the edge of the waterfall.

$200 a square ft? Try $100. When interest rate hits 15%, and real unemployment hits 15% as well, houses will again be affordable, except no one can buy them….

Areas of IE and Bay area is already close to, if not below $100 a sq ft.

Wow, another great assessment — thanks doc. I’m in a plastic surgery group here in Utah and after reading your take on the 30-40% declines in SoCal cosmetic work I warned my partners. We’ve hunkered down now, praying and hoping. I have watched nice home prices start to decline here on the edge to below $100/ft but I won’t buy until $50/ft or lower ($25?). Who knows how low it can go? Not in any rush. My wifey and I rent and save for now and live VERY conservatively (not like on Nip N’Tuck). I also have family in SoCal and wonder if you guys are gonna consistently see

if you ever get the chance while in New York, visit the small morgan museum. He was an avid collector of books. Free entry with live string quartet on Friday evenings after 7pm. they also offer the morgan martini, to steady the financial nerves.

Great article doctor. I don’t think tha the government should be helping out at all. At some point the Fed willhave to say ‘we can’t give out any more money’. And why should people that were prudent pay for the mistakes of others.

“why should people that were prudent pay for the mistakes of others” Basically because the prudent people put their money in the bank and, instead of Jimmy Stewart being the banker, Angelo Mozilo was. Was it Morgan who made the quip “when you owe the bank one hundred dollars you’ve got a problem but when you owe the bank $100 million the bank has the problem”? Present day banking

has turned that bit of wisdom on its head. Nowadays even small time deadbeats

leave the banks nervous. I went into the belly of beast today. Wachovia. I had a SunTrust CD expire and needed to do something with the money. That is the prudent person’s dilemma these days. Its not like SunTrust or BofA or even the Swiss banks offer one any ‘peace of mind’. Wachovia is offering almost a full percentage point more than anyone else ( their desperate) so I rolled over the $25K with them. As I chatted with the branch manager I said ” Don’t you guys pull an IndyMac on me” and the branch manager said ” I put all of my 401K into Wachovia stock last week when it fell to $7″. I almost choked as I thought of those poor souls at ENRON who had done the same. I mumbled “I wish you luck”. I would have liked to have chatted somemore but there were other lambs out there waiting to open CD’s, like me, desperate to get something for their hard earned money.

There are so many angles on this issue, MC Escher could have drawn this whole bizarre debacle.

I think the majority of the American public could, and would be able to afford what they had worked for all their lives if they weren’t being taxed out of existence.

How much do we have to fork out to support massive numbers of immigrants who never put a dime into Social Security?

How much do we have to pay to house, feed, educate (in their own damn language) and medicate hordes of illegal immigrants?

How many billions have we given away to foreign governments and organizations? Loans forgiven and outright gifts? Who did all that money come from?

Yes, people like to say the government borrowed it from a central bank that created it out of thin air. It doesn’t matter, all of us were left on the hook for it, and in order to satisfy that debt we work like slaves with guns to our heads.

I don’t know about you, but I’m pretty pissed off about the $15 BILLION that Bush gave the countries of Africa to fight AIDS. Not because I don’t want people who are suffering to receive help, but because we got nothing in return but bad press and comments about how stingy we are.

Those same politicos now say that we are to blame for the straits we are in, and the only thing they’re doing is trying to cover the asses of their wealthy contributors while leaving the rest of us to twist in the wind.

Johnny 5, glad to see you’re only looking out for numero uno… Also, immigrants are good for social security. They pay into the system with fake/stolen documentation, but never take money out when they retire. See this: http://www.nytimes.com/2008/04/02/opinion/02wed3.html

Back to immigrant bashing Johnny 5? Why dont we blame global warming on them too. How about Hurricane Katrina? Enron? 80’s S&L crisis? Get over it man! Do what you can to elect someone that you think might put an end to it and stop spreading your hatred. Just in case your wondering, yes I am of Mexican descent. My parents taught my brothers and I to work hard and earn an honest living. Some of us listened others did not. Just like White, Black, Yellow, and Red parents do with their kids. Crap happens, what can you do?

Great article as always. Your blog is a must read for me everyday. You have great insight into the housing market.

I am waiting to buy and it is really darn difficult to wait, especially when it seems you might be one of the few qualified buyers out there. But I am waiting because I realize the market is very probably heading south further. The only problem with this stubborn market is it moves along so slowly and sellers are really calcitrant about lowering their prices.

It’s always nice to see what you have to say to give a more realistic breath of fresh air than the propaganda espoused by the government and realtor associations. It reminds me how stinky this market really is and why there are many reasons it will continue to drop.

To those who think I’m “immigrant bashing”, get a grip. I’m the son of an immigrant. One who came here, and did it legally. English wasn’t the only language spoken in my house as I grew up.

Your knee jerk reactions and inferences that I’m targeting legal immigrants and Latinos show where the hate really is, and who is truly intolerant.

Why is it that when someone mentions illegal aliens, they’re seen as “immigrant bashing”? Immigrants come here and deal with the hassle of INS and go through the red tape. Illegal aliens just hop the fence. No better than tresspassers.

If illegal aliens wanted to truly contribute to society, then come across the border and deal with the red tape and bureaucracy that comes with being a United States citizen. But don’t come over here in a criminal manner (because illegal means that something is against the law, break a law, you’re a criminal) and then demand rights.

Yes, our nation spends an assload on illegal aliens, while our citizens suffer. Has anyone ever tried to apply for public aid? I did when my wife was pregnant with our first child. We both worked just under full time, so we weren’t able to get health insurance through work. So we applied for the state health plan. Had to jump through hoops galore. However, if you are an illegal or a “migrant/undocumented worker”, you move to the front of the line for “emergency approval”.

Leave a Reply to dreadlord