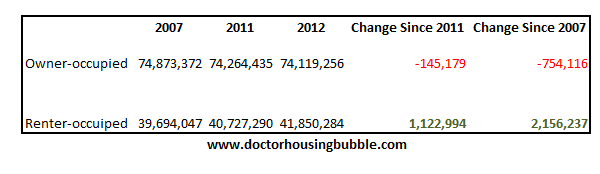

Landlord nation: Since 2007 the US has added over 2,000,000 renter households while losing 750,000 owner households. Rents rising in spite of falling incomes.

After scouring the newly released Census data many things stood out but one of them continues to reflect a growing disconnect in housing. The US is adding many more renter households. This of course is occurring in spite of record rising home prices. For regular buyers, the mortgage market is still checking carefully for income and other requirements yet “cash buyers†continue to be the dominant force in 2013. In expensive areas like California, more people are using jumbo loans. Ironically, the market has now adjusted once again to the Fed’s obtuse language on tapering. While this language might come off difficult to decipher, the stats are very clear. Over the last six years we have added millions of households as renters. What are the longer term implications of this?

Renters versus owners

I went ahead and pulled data from a few key years and the latest 2012 annual Census data:

The biggest change of course has come from the growth of renter households. 2.1 million more families rent today than they did in 2007. Even more telling, from 2011 to 2012 we added 1.1 million renting households. I think this is largely a reflection of the massive amount of investor buying and Wall Street suddenly having a liking for rental property. Is this a positive trend?

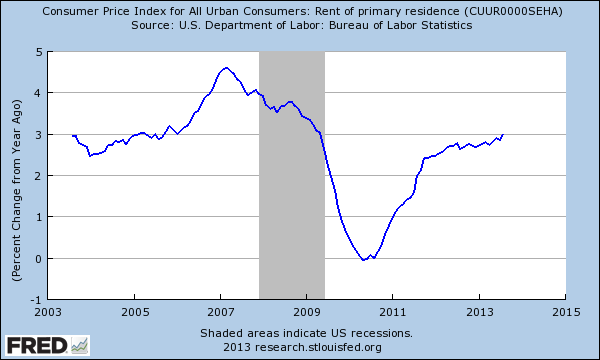

For one, it is clear that rents overall are rising:

US rents are rising at about 3 percent annually, about twice the rate of the overall CPI. The problem with this is that the Census figures also show that household incomes are falling. So more money is now being shelled out to rents. Or if you are buying, more is going to your PITI because home prices are now rising at an incredibly fast pace thanks to investors flooding the market. One thing is certain and that is more money is being plowed into real estate and that isn’t necessarily a good thing. Discretionary money is being earmarked for housing.

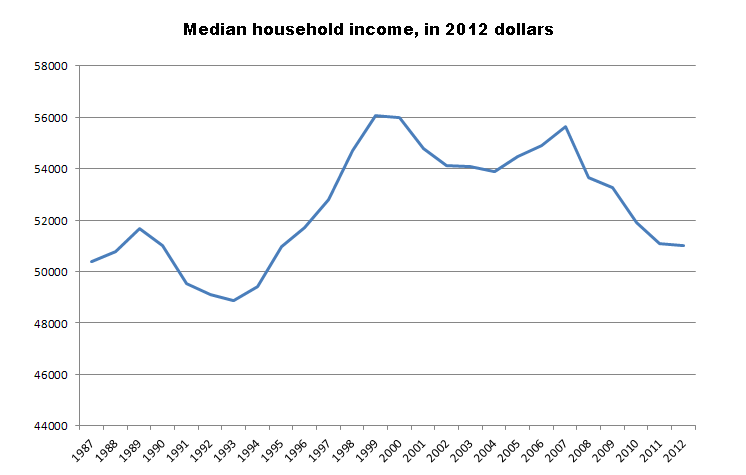

This is occurring under the context of falling incomes:

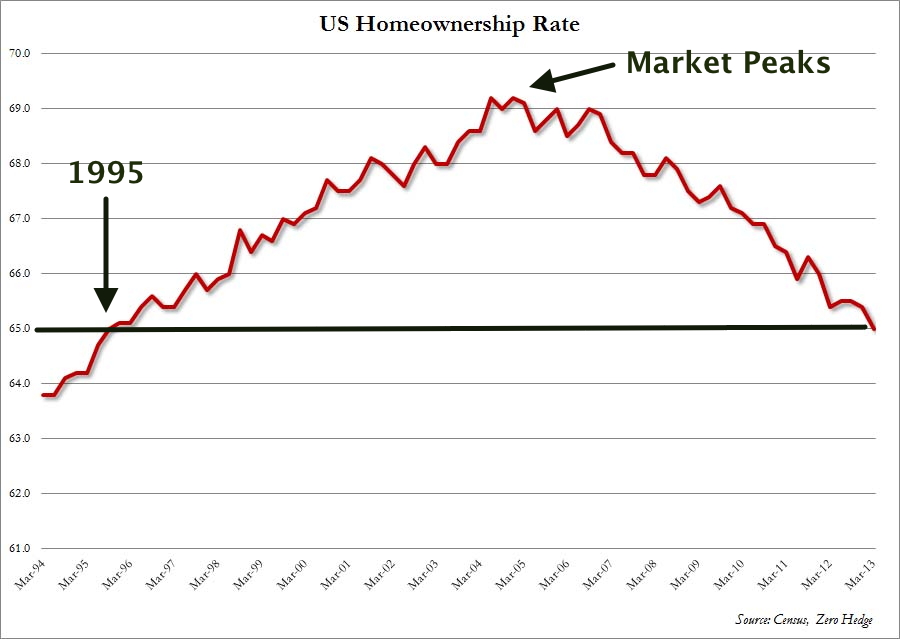

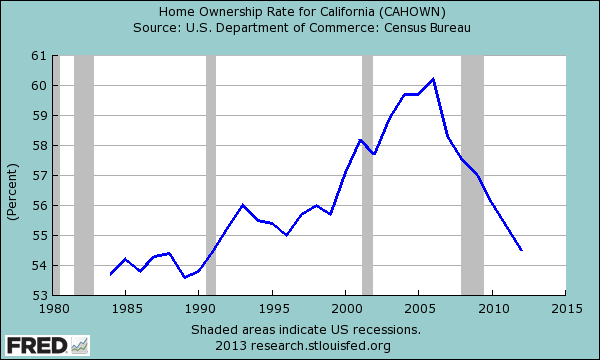

Adjusting for inflation, US households are making what they once did in 1989. In fact, the US homeownership rate is heading back in this direction as well:

Historically, US households have stored most of their wealth in housing. So the overall drop in homeownership and the big increase in renting means more Americans are being left out of the most typical way of building wealth. Of course, before the banking system turned housing into one giant casino, most households had very simple guidepost of entry. You bought when you were ready. You bought in an area you planned on staying in. You didn’t have to worry about buying at the top or bottom of rollercoaster swings in real estate that occur courtesy of the whims of the Fed. Today, you have some markets were over half of purchases are investors and in some areas home prices are rising by 30 percent annually even though incomes are falling!

This path is unsustainable and we even saw what happens when hints of removing the taper hit the market. The market understands that the Fed is the major player here. For most Americans all the banking bailouts have resulted in massive residential grabs by banks who are outbidding regular families.

People have a keen sense as to what is happening. This has been and is a bailout of the wealthy:

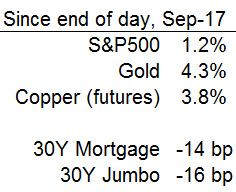

“(SoberLook) Mortgage rates declined – a full 14 basis points. So that’s the impact on the “real economy” of delaying “taper”? To make matters worse the decline in jumbo mortgage rates was higher than in conforming mortgages. Between the pop in investment portfolios and the drop in jumbo rates, those who are well off to begin with are more likely to benefit from this policy decision. Was that the intent?â€

Jumbo rates only impact a tiny portion of the market. In the Bay Area, jumbo loans make up 47.8 of all housing purchases and 27.2 percent of the market in California. Throw in cash buyers and over half the market is being driven by “cash buying†and those taking on jumbo mortgages. You think this is helping the ownership rate in high cost areas?

Not at all. And jumbo mortgages are a miniscule part of the market across the US. Welcome to renter nation.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Â

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Subscribe to feed

Subscribe to feed

65 Responses to “Landlord nation: Since 2007 the US has added over 2,000,000 renter households while losing 750,000 owner households. Rents rising in spite of falling incomes.”

Reasons against buying:

1. Job and income certainty is questionable.

2. Hard to accumulate down payment due to rising living costs

3. Tightened lending standard making credit less accessible

4. Memory of housing bust

5. Belief in low inflation or deflation

Of the five, #2, #3, and $4 were not present in 1995. Despite the low rates and low prices in 2008-2010, many families did not purchase a house.

Here’s an LA Times article from 9/23/13 that says pending home sales are down 5% in August from July, and down 9% in August from one year ago, due to rising interest rates —

http://www.latimes.com/business/money/la-fi-mo-california-pending-home-sales-20130923,0,5657900.story

Here’s a Reuters article about Oaktree Capital selling a portfolio of 500 houses they bought in foreclosure and rented out. The hedge funds are starting to cash out now, they know the recent rise in prices is over —

http://www.reuters.com/article/2013/09/23/us-foreclosed-oaktree-housing-idUSBRE98M0WV20130923

I have been tracking 3bd 2ba homes in a particular zip code in LA and even after all the hubub about prices flattening, higher inventory, etc. The inventory as of Sept 2013 (current search) is LESS than I have seen in the past 3 years. 12 homes rather than the 20-25 homes I usually see for sale. what gives?

I’m like you QE-A…. I watched the market in Arizona since 2002. Little of it made sense. Finally, in Feb of 2010 I purchased q new construction from a builder who wouldn’t stop throwing extras at me. Interest rates were right, location was great, with a reasonable lot. I finally did it and bought. But my head still spins with all the movement. I got lucky, and got it pretty close to right….. now, Well, I just don’t have enough health brain cells to keep track…. I’ll live here until i’m dead.

@QE abyss wrote: ” …inventory…is LESS than I have seen in the past 3 years…what gives?”

What gives? Sounds like you are tracking an area that is price attractive to flippers, REITs and investors. So the flippers and investors have swooped in and have vacuumed up the SFRs.

All real estate is local. And in some cases, real estate is extremely local.

The zip code that I live in, the inventory has been flat for a long time. Then again the median listing price on an SFR here is $1.4MM. So flippers and investors aren’t touching anything here especially when for the same money can get 4 to 7 SFR’s elsewhere.

The rentier class, Obama’s masters, are making out like bandits. Buying up all the assets and watching them bubble up. Now, see how the game is played, higher rents and lower wages, just like magic. And, the idiots still listen to him like he was some kind of messiah. Take a close look at the economic scheme behind the proletariat queen, your Senator Feinstein, and you will see that she is dipped in gold rentier a dozen times over. This is the economic system that was perfected during the middle ages and it is back with a vengeance.

Fulano,

Save your political diatribes for some other forum.

There is plenty to disagree about here, and the discussions are very interesting and informative.

Your posts are not interesting or informative.

Keep the nasty grams on some other forum where people like to have meaningless arguments.

@ Regular Joe

If I am not mistaken you do not run the blog. If you find my comments uninteresting, don’t read them, simple as that. However, I think you might learn a thing or two, considering you are a “Regular Joe”, about how the overall manipulation of the economic system affects not just the real estate market but a “Regular Joe” on the street. Rather than attempting to censor opinions, you might try rebuttal.

I am just saying that you could figure out how to make the same points without turning this into a useless political debate.

We have enough of that elsewhere.

This seemed like the one place where I could read opinions without feeling like I was sitting through some kind of political indoctrination.

Congratulations. You lowered the bar.

I agree with you Regular Joe.

I don’t find comments in threads using emotionally charged sound bites of some partisan gripe to be much useful or interesting.

This housing situation has been propagated on much longer than any particular U.S. President.

And I think that’s because discussing policy has gone out of fashion.

We should get back to discussing policy everywhere.

Thankfully, most of the comments on this blog do that.

@ Regular Joe, et al.

I guess you do not subscribe to the author of this blog’s writings, which are politically charged: “People have a keen sense as to what is happening. This has been and is a bailout of the wealthy:”

The reason for this is POLITICAL. It is all about the elite who control the financial system and if you think that has nothing to do with real estate, good luck. Please read the article below and see how your Senator’s husband benefits from this very system. How do expect to change things when these are the people who “represent” you. Yes, I guess ignorance is bliss. The points I make are based on facts, not emotions. By the way, this Fox news bullshit comment, I go on record that the Republicans are worse than the Democrats and Bush appointed the current Fed Chair. Maybe you guys should find a blog where all they is talk about real state price moves and where the best deals are, rather than analysis and critical thought as the Doctor provides.

However, I think Lynn Chase is correct, not only do you not have a clue but you are not interested in understanding how the financial system actually works and AFFECTS real estate.

http://www.washingtontimes.com/news/2013/jun/12/firm-chaired-by-sen-feinsteins-husband-cashes-in-o/?page=all

Joe, how about you keep YOUR mouth shut eh? I read your crap, let me read other people crap. I like reading posts that come from outside the “regular joe” mentality. Regualr Joe’s are what makes this country suck a$$ because they watch TV, eat fast food, and post things like you do.

Who appointed Regular Joe and watermelonpunch as moderators of this site? So posters can’t discuss politics or politicians when they have a major impact on the housing market? Regular Joe and watermelonunch want to silence anyone whom they disagree with?

I like fulano’s points and believe they are valid.

I don’t care what you think about his points.

I am tired of decent forums getting polluted with political rancor that adds nothing to the conversation. He could have made the same points without sounding like Fox and Friends.

The oligarchy in this country is not Obama’s master any more than anyone else in government, politics, banking, Wall Street, etc.

I don’t buy the whole ‘Obama is the boogey-man and is responsible for every bad thing that happens on the planet’. We all need a scapegoat to blame, and the radical right is happy to pin everything on Obama.

As a fiscal conservative, I am not all that happy with many of his policies, but I am well aware that the nefarious, self-serving and destructive ruling class in this country is not limited to or defined by a given political party.

There really is no point to Obama-bashing here, as Regular Joe points out. It detracts from any point that may have had some validity in the post.

It seems that Aimeel also needs a scapegoat to blame, so maybe that’s why Aimeel is blasting the “radical right?” No doubt Aimeel and the radical left is happy to pin everything on Bush and Reagan while ignoring the actions of the Obama regime?

the problem is the ” regular Joes” of the world don’t have a clue as to what is happening and how the criminal global banking system is robbing the world and creating feudal system.

Oh, my, my, looks like we pushed a button, Sylviasays?

Doesn’t take much to get these folks to go apoplectic! (LOL!)

That jibes with my experience, sold my last place in 2007 as I knew what was coming thanks to a couple of blogs I follow. Decided to buy again in spring 2011 but it was hopeless as the sort of house I was looking for (a 3/2 in a decent neighborhood) was also what legions of flippers and specuvestors were seeking too, got beat by cash several times….had a big down payment, preapproved loan, great credit etc. but that did me no good. Gave up mid 2012 and am continuing to rent in the meantime, may consider buying again once Bubble 2.0 pops but not now, prices are up about 35% in the last two years where I live in Sonoma Co.

I’d like to chime in from the Sacramento area and say myself and many of my friends and family have a similar outlook. Save, invest elsewhere where it makes sense…keep our cheap locked in rents for now.

This is insanity…I can’t wait for the evidence to become a little more irrefutable. 35% increases here too … sellers and realtors are claiming this IS where the price should be. Very arrogant of them and proud to say many of those houses are still sitting out there 30 days later. Good time to buy … yeah right! Many price drops starting to occur in our area, although the inventory is still looking low. Guess banks aren’t ready yet to give our communities back…but hey, who would fight them?

I agree with a lot of what you write and respect the fact that you are actually saving money, but curiously where does Gen Y think its safe ‘to invest elsewhere where it makes sense?’ If you believe that QE has inflated asset bubbles like real estate in Sacramento or elsewhere, how would other assets not be inflated similarly like stocks? Even Buffett said there were no bargains left in stocks two days ago. Gold and silver are tricky investments that seem to be hammered down by the govt to make the world think all is well with fiat currency so those investments have risk attached as well. Cash, where I am mostly, sucks bc of hidden inflation. I get the whole savings thing, I just don’t see the safe alternative investment.

Gen Y, I empathize with the younger generation regarding securing affordable residential property in California, I believe your are correct, its a hopeless situation for most of you for the time being. I think it would be in your best interest to wait a little longer perhaps another 2-3 years, by then the banks, hedge funds, and foreign investors will sours on the residential rental business due to increased maintenance and stable renters. High value jobs are hard to come by here in California and reliable renters are in short supply. Just a suggestion, if your career permits, you might want to look at the Gulf Coast MS, AL or FL, they are not all uneducated folks, decent quality of life and very nice homes for under $150-175K. Have lived in CA all my life, but if push comes to shove and if I had a young family I would be compelled to relocate to an area where the property values are stable and not subjected to investor flip flopping. Living in California is great but one should not live to support a house, there is other things in life to do! Not here to promote these states but suggesting alternatives of stable housing in the US.

@FTB – thanks and interesting question regarding where is a safe investment for gen y. first, i think you are correct, in my opinion, about stocks being over valued. However, at least in the past 24 months … I preferred stocks because they are easier to diversify, liquidate and have lower acquisition and liquidation overhead. If stocks dip, you’ll take a loss but can still offload before losing more. If the housing market tanks (which i also think is unlikely that it will tank like 2008 again) you are trapped until it returns. Along with the cost of the mortgage, that is a lot to take on to feel underwater. Right now, i feel cash is a good option, but fear the same thing you mentioned … devaluation of our dollar by the FED and hence the guaranteed inflation to follow making the dollar i hold worth less every day. They are very good at forcing you to spend your savings now before they make it worthless.

Here in Sacramento, housing investors have all but disappeared indicating that there is no good yield anymore in housing … so hard to feel like it is a good time to buy if the pros think there is nothing left in it…I believe we’d be lucky to average 2-3% appreciation moving forward in the upcoming years … not really great for the risk, taxes, maintenance, etc involved. One thing i must disclose though is that i currently rent a 1600 sq ft home for $1300/month in a pretty good area and am on month to month terms. Fantastically cheap for around here and buys me a little more opportunity than someone just moving into a rental today.

For me personally, adaptability is the greatest investment at this volatile point in time… keeping the opportunities on MY SIDE. I don’t think at this point i’ll be missing out on much… that was last year … not the next 5. I think the following have me convinced we are still actually in a little bit of a recession:

1. Average wage has been proven by BLS numbers to have decreased over the past 5 years. Teamed up with the obvious inflation, that is a much weaker consumer.

2. The FED has had 5 years to make a mainstreet impact to where we would hear about the wage increases and much more hiring of quality jobs. They haven’t, but inflation on durables and assets took grip (greed and speculation for investors easy money).

3. They couldn’t even influence the rates 1% from 3.5 to 4.5% without it totally flattening the housing market. Doesn’t sound very strong to me.

4. This latest news last week on the fed NOT tapering in Sept had a 1 day rally and then subsequent dip erasing gains. The FED has exposed the weakness of their plan, which is that even after 5 years, all they did is create foaming at the mouth investors that will yank their investment at the slightest indicator that stimulus will subside and asset bubbles that would pop if they stopped..not really ideal long term.

The list of indicators really does go on and on. I’d at least like to wait through the debt ceiling and obama care to make any large decisions.. I think we are at a point in history where i feel more comfortable holding onto my opportunity tightly rather than gambling it away. Wall street has partied now for almost 20+ months … Just saying there are practical limits and this whole recovery was engineered and doesn’t feel genuine. It surely wasn’t because people are better off. And for now, it has worked for assets only but pressure is rapidly building again. 2014 will be interesting .. we are all getting massive pay raises, or perhaps some simple math and business dynamics will become more obvious to everyone… we’ve been fighting deflation for a decade now… wage gaps are growing…systemic issues are persisting. If and when things change, i’d like to be able to change with them..

What are your thoughts on some of the above? Curious to what you see out there and what your experiences are.

I also live in the Sac area. Outer Eastern suburbs, newer homes. I have a good, secure job, $75k a year income, no debt and a good down payment yet I can’t even afford to buy a condo in my area in 2013.

It makes absolutely no sense. I am above median income and I can’t qualify for a loan to buy anything.

Sacramento has notoriously low wages. The average wage for a person in the Sacramento region is $27100 per year. Median HOUSEHOLD income is $56500 per year. Average property price is $285,000.

If I can’t qualify (borrow enough) to buy an average property here, on $75k a year and no other debt, how can anyone else? I earn 37% MORE than the average household in Sacramento.

In my zip code the average per capita income is $36,300. Average house/condo price is $356,000. WTH? 10 x your income? I earn nearly double the median income for my zip code and I can barely buy a 2 bed condo… and a so-so one at that.

What does this tell us? None of these numbers make any sense. Nothing adds up. Economic fundamentals are not there.

We’re in the Sacramento area also and have noticed many housing price drops as activity from cash investors has all but diminished. We’re looking in the City of Roseville which is about 35 miles northeast from downtown Sacramento. Roseville has many newer middle to upper income housing developments and it’s generally a safe community with good schools. One house we’ve been following is a 4 bedroom 3 bath house that was built in 2002 in West Roseville. The house has dropped in price from $375,000 in July to $340,000 last week. It last sold for $365,000 in 2008. The Realtor has had a couple of open houses but no offers.

http://www.zillow.com/homedetails/1848-Granite-Way-Roseville-CA-95747/59369532_zpid/

@ Gen Y, another Cali gen Yer here. I live in the LA area, bought a 2BD/2BA condo townhouse in 2010 in a nice quiet area, good schools, decent proximity to downtown, a good neighborhood sushi joint a few blocks away. I can’t speak to what it’s like trying to secure financing these days, but housing prices in my area are definitely up significantly over the beginning of this year. An 850sqft condo went on the market at $320K in July, price was raised to $340K in August, and closed in September for $330K. Last year those condos were selling for $230K-$260K. Right now there are actually no apartments or condos listed for sale in my zip code, which is something I haven’t seen before. The cheapest property is $380K for a 950sqft, 2BD/1BD sfh fixer upper. If I hadn’t already bought, I would be completely priced out of my zip code right now.

Rents are also rising in my area. Two years ago, units in my HOA were renting for $1625-$1750/month. Now they are renting for $1900-$1990. Again, ridiculous.

The only advice I have for fellow GenYers is the age-old advice of save your money by minimizing expenses, build your skills and network to increase your income, keep your money in safe(r) investments. Also, make sure you don’t have unrealistic expectations about your lifestyle. I’ve seen too many co-workers my age complain about being unable to afford a decent house, when their idea of a “decent house” is a swanky 3BD/2BA pad with all the bells and whistles in a prime location for $300K. (Umm…not gonna happen.) These are also the people who complain about how it’s impossible to save for a downpayment these days, while they drop $2500 per month to live in their luxury loft apartments and drive around in their $400-a-month-lease car. (Gee, and they wonder why they can’t save for a house.)

The ownership society. I guess it’s getting smaller.

The next step for the banksters is to manufacture a situation where folks get used to taking out loans to pay their rent. Leverage up so your kids don’t get stuck in the ‘wrong’ school district.

This already happened in the last housing bubble in Los Angeles. In 2004 The East/West Bank branch at the intersection of Wilshire and Grand in downtown advertised for apartment loans with a big red banner stretched out front. I went in to ask because I wasn’t sure if it was for purchasing an apartment building or to renting an apartment. They said it was for renting as the loan to purchase a building wasn’t a new product. They had people lining up because they had to live somewhere and didn’t have the money to cover costs. In fact my rent was going through the roof too. For me, between 2004 and 2005, my rent went from $700 to $2,800 per month that year. It doubled every six months. I was about to vacate when the owner suddenly went bankrupt and died. The building was paid-in-full already and another owner took over from out of state. He let us stay if we would agree to pay our original rent amounts, which we did. I no longer live there now. Bought in Glendora in 2009. Don’t know if the building is even still there.

Hey Bloggers,

Are there any honest realtors or current buyers out there have any first hand experience or any update on the home buying frenzy in the Inland Empire as of late? Such as are the foreign money from China still out buying at full force, are there still lots of serious offers on a single home, and are buyers still flooding the open houses? Also, are banks still releasing the shadow inventory on their short sales?

The builders shares are up is reported.Lets take a look…Mighty developers are seems to be making a killing by building & converting places, super cheap new cramped cages for serfs.Section 8, HUD,USDA etc..subsidized housing is mushrooming all over the place.How are these cheap cramped cages gonna look like in 10 years time,who is going be its occupier,what would they do, how would they feed themselves,what would be their mind set? Do you still need a crystal ball to see the future.?Those attractive voluntary prison camps are marketed as quality living at affordable price, pictured akin to care free living vacation homes with swimming pools and palm trees from afar..You just don’t see the monkeys…not yet, unless you decide to join the crowd and sign on to their waiting list.

To get in one of those cages your lease must be approved…the application is 10 pages long, where the approving brothers and sisters running the camp are having a chance to peak in your empty wallet,in your checking account, in your grandmother jewelry box, and your uncle Barney family ranch barn.Once lucky, approved for the cage of your own, ever so often your income will be assessed and reevaluated, so to make sure you’re good serf you said you are, and you don’t make any more money under the table, or your rent goes way up.

Next week stop, trailer parks reviews and the benefit of living frugal in one of my custom build modular homes.

A decline in home ownership rates is not a bad thing. As part of the housing bubble, people who couldn’t qualify for a used car loan were given mortgages. If they broke a shoelace, they lost their house. This was not healthy, and we do not need to go there again. In Germany, the healthiest country in the EU, home ownership is only about 40%. Let’s put this all in perspective.

The Germans are thrifty, work hard, and are not involved with the Euro. Angela Merkel is proud that her campaign “was the dullest ever.” The Germans produce top-quality goods, and take off a month a year. They are conservative with their assets. When they take over Europe, they probably shouldn’t start with Poland.

Well, that’s nice and cherry for them in DE. But how about this perspective, the typical section 8 renter paying 15 to 20% of the rent you pay, or you own a house in middle class hood and the investor next door rents section 8, because money is guaranteed… you property goes down in value.

how about the state and federal assistance purchase down payment, for which mostly broke people who will eventually default qualify for… you my friend don’t make the cut.

What happens when you make too little money to compete with rich or Foreign investors, and too much for state assistance programs?

In a true free market everyone finds their place by making sacrifices… in manipulation you are sitting duck!

Once again superb analysis. This won’t bode well for the economy or for anyone in the country. Eventually the people getting screwed won’t take it anymore. With enough guns to arm every man woman and child eventually this leads to bloodshed and it should. The rich need to realize that what allows them to become rich is that most citizens can buy their products. Henry Ford realized, but somehow the country completely lost its way in the 80s and now too many people have the evil government taking my hard earned money attitude. Your money wouldn’t be worth the paper it’s printed on without the government. Quit acting like you did it all yourself. Even the super rich would be unable to become rich without the rest of society. You think they build their homes and yachts by themselves? Do they build their own cars? Quit crying just because you are asked to give a little more back then the guy who can barely afford to eat and feed his family.

=Eventually the people getting screwed won’t take it anymore. With enough guns to arm every man woman and child eventually this leads to bloodshed and it should.=

The rich own the media, don’t forget. Anyone taking up arms against the government, even with the best intentions will immediately be painted, by the masters of mankind, as an enemy, a terrorist*, armed-and-dangerous, psychologically unstable and a traitor on the news shows. You know the rest. Revolution 2.0 is not an option. In a ‘free’ country, folks are controlled by propaganda, anyway.

And are there not social studies in existence that show no correlation between a citizen’s happiness and his country’s per capital income? A little food, a little beer, a little sex and other social interaction, and a little cardboard over one’s head to keep the rain off from time to time is all one really needs for happiness. I imagine the rich can plunder all they like, as long as it happens incrementally, and there won’t be much of a fuss (especially since our ‘poor’ people have access to enough nutritional calories to turn them into 350 pound ‘people of Walmart’ folks, have a/c, microwaves, diswashers, etc., have cable/internet/iPhones, have free medical care if they get into dire straights, etc.).

*Incidentally, was it not just the other day that there was some political pressure to try to classify anyone opposing the Keystone XL Pipeline via picketing and the like, on site, as a terrorist?

*per capita

Very good post.

Having watched properties in San Diego get close to their 2005-06 price levels again, I have decided to sell a rental (duplex) and roll the cash into another state where prices are still about 35% below their 2005-06 levels. Will likely buy 5 units for the price of the 2 I am selling here. I don’t feel like I am some horrible person for buying rental properties DanG, nor are we rich. Rather I am just trying to have a source of income down the road when SS goes bust. I have been thinking of rolling my 401k into rentals too, before the guberment grabs those from us ala Poland and Cypress. While prices are high today, do you really think they will be less in 15 years? I don’t. Do what you can to get your foot in the door and try and pay it off as soon as possible has always been my advice. No, I am not a RE Agt, just a average hard working guy that wishes he had been smart enough to buy in 2010-11.

Jim wrote “I have been thinking of rolling my 401k into rentals too, before the guberment grabs those from us ala Poland and Cypress. While prices are high today, do you really think they will be less in 15 years? I don’t. Do what you can to get your foot in the door and try and pay it off as soon as possible has always been my advice.”

If you believe the “guberment” could/would “grab” a 401k, what makes you believe the “guberment” couldn’t “grab” RE in similar fashion if it wants to; some type of eminent domain, raise taxes/fees that it would be a financial hardship/no longer make sense to keep it? How is RE unique from other assets if the “guberment” really wants “grab” it?

“Do what you can to get your foot in the door”. Oh, dear.

Reporting from San Diego; prices up > 25% y-o-y (varies, depending on location). Made attempts to buy last year, but opted NOT to get caught up in a biddging war. Moving into a new rental in a nice location. Reducing current rent from 1800 (2/2) to 1500 (3/2). Purchase mortgage would have been closer to 3500 for what I was looking at; homes in the area of this rental go for about that. Will easily put away 2000/month for ~12-24 months (translates to 24-48k; not including interest). I don’t see this type of return on the home I would have purchased. I’m very happy with my decision. Oh, and the house I failed to buy back in 2000 resulted in a savings that allowed me to pay cash for a second home in Big Bear Lake… I’m playing this market for what it is… a game!

This is the top. Guys just wait. Who will investors sell to?

Think about it. THe big crash investors stepped in and bought from the people who could not afford. Well when we crash a second time this safety net of investors already used their cash. They will now need to dump and who can buy? First time homebuyers. Where are they, out of work kids with college loans. So we are talking 500k homes will need to be sold down to 200k for them to be able to buy.

Just wait and watch the epic crash to come.

That reminds me, hows that Canadian housing bubble coming along? Last we heard, there were corrections with no stark crashes.

In my opinion I am concerned with the taper being stalled the FED chief is probably being allowed to leave looking like something was accomplished to fix our debacle. After the curtain is lowered it’s anyone’s guess what happens next. Pray for our grand children’s economic future.

http://www.zerohedge.com/news/2013-09-22/what-shadow-banking-can-tell-us-about-feds-exit-path-dead-end

Maybe a new government program of affordable housing paid by guess who….wait till you meet your new neighbors..

When the ownership rate falls to 50%, the people will revoke Prop 13 and property taxes will go up. California has the Red Star in the flag. Soon it will be a reality.

Before residential real estate gets knocked off Prop 13, they’ll go after commercial real estate. With disastrous results for this economy, I might add. That might be able to pass a ballot vote now.

In my opinion the only way that may happen is when all investors have left California.

Rachael, it was “the people” voted in Prop 13. Were they commies, then?

And, you can’t “revoke” a proposition, unless it’s found to be unconstitutional.

But, you’re right, there is a red star in the state flag. Good work.

Here’s an interesting LA Times article about a homeowner in one of the “desirable areas”, where it’s rumored the economic downtown hasn’t hurt people, they’re all doing just fine…

http://www.latimes.com/business/la-fi-dreams-on-hold-20130922-dto,0,4020745.htmlstory

One of my relatives has been a homeowner in a “desirable area” for years; from the multiple stories I’ve heard, this family’s situation is hardly unique.

I read that little article. This is a perfect example of long time owners who would have zero percent chance of buying their house today if they had to. A teacher who makes 68K per year can’t buy in Redondo anymore, plain and simple. This example is definitely not representative of what is going on in the desirable areas. For every long time owner who decides to sell, there are very qualified buyers who will take their place. Gentrification is happening on a grand scale.

I doubt this family is an anomaly. In many “desirable areas”, especially near the beach, homeowners who bought pre-2000 far outnumber recent buyers. I doubt a majority could qualify to buy their own house at today’s prices.

Job loss, adult kids moving home after college/job loss/divorce (some w/grandkids), business closure, bad investments, etc. affected many Americans; it wasn’t restricted to the poor/middle class. In “desirable” hoods across the USA the valiant struggle continues; flashy leased cars, expensive haircuts, designer clothes/handbags bought with available credit perpetuating the illusion that all is well to neighbors, family and friends. As long as minimum monthly payments are met, lives continue like carefully crafted stage sets…looking great for the audience; get up close, roll back the canvas and often there’s little but dusty scaffolding holding it all together.

I may be in the minority, but I feel the people in the article should go to a financial planner. In considering her mortgage payment of $1300, the owner probably owes under 300k. The lowest priced home with close to 1000 square feet in Redondo is about $560k. My feeling is she should sell her home and pay CASH for a condo in Lomita or Lawndale, or some other neighboring city that is a slight step down. What was the point of this article? I don’t feel sorry for her.

Drinks, I had to read that again and really don’t feel sorry for them at all. The LA Times really put out a good sob story there.

First of all, they bought in S. Redondo (a block from PCH) in 1994 for 260K. The place is likely worth 750K today, assuming they didn’t cash out any equity…they are likely sitting on 600K plus of equity. Am I supposed to feel sorry for these people? Sell the house, buy a cheaper place cash, problems solved.

Husband only saved 130K for retirement and blew through it quickly. Who’s fault is that? I suppose mine.

Daughter is unemployed and mad that she can’t get a decent job after slaving away getting that sociology degree (and she wants to get a masters for icing on the cake). How about a degree that is actually applicable in today’s society: nursing degree, engineering degree, accounting, etc. That actually might take some real work.

Daughter didn’t do herself any favors marrying a guy from Hong Kong who is waiting to get his work visa. And certainly didn’t do herself any favors by having kids in such a precarious economic situation.

And quit playing the lottery if you literally don’t have a penny to spare. Like I said before, these people are lucky they bought when they did. People waiting to snap up their house at today’s prices are waiting in the wings.

No sympathy here either. The article says the husband blew through his entire $130K retirement fund in 3 years. How the heck does that happen when he was making $52,000 per year (gross, I’m assuming), unless he kept right now spending money as if nothing happened? If my husband or I get laid off, that means we immediately go down to bare-bones spending to preserve our cash reserves as long as possible. No trips, no eating out, no iPhone, no nothing.

Also, if mortgage is $1300 per month and the wife is making $68K per year, and the husband’s SS income is $1500, then where is all the money going? She must be netting at least $3200-$3500 per month after taxes, and his SS income more than covers the mortgage. Even after paying part of the daughter’s student loans, they would still have over $3K per month between the two of them. Why do they even have credit card debt? I don’t understand this at all.

If she wanted to save money, she should put any extra cash toward paying off that credit card, which is no doubt costing at least 15% interest. That would be the equivalent of earning a 15% return on her money, which blows away any other investment option out there.

Drinks,

I played internet detective for 5 minutes and found out where the Barkers lived and did a Zillow zestimate on their property. South Redondo premium area on a large lot.

Zillow says estimated value 904K!!!!!!!!!!!!!!!!!

Somehow the LA Times forgot to mention that. These people should sleep real well at night, there is nothing to worry about. I feel sorry for folks who are one missed rent payment away from living in their car.

The QE program is designed to prop up the prices of financial assets. It is putting vast quantities of newly created money into that sort of thing. But that is not money that circulates, so it has little impact on the velocity of money, hence no huge jump in inflation.

If the economy were to start firing on all cylinders, we might see inflation with the prospect for another round of inflationary housing price increases like back in the late ’70s.

This QE policy is not specifically Obama’s in its origin, but since it keeps growing on his watch he should own it now, for better or worse. Tax cuts were called “trickle down economics” by the opponents. But they do increase the money that circulates, instead of just pumping up assets. So QE can be considered trickle up economics? Or trickle down monetary policy as opposed to trickle down fiscal policy?

I work for a living, and as we have lived fairly frugally as did my parents and my Wife’s parents (all deceased), we have quite a bit of money put away for our retirement. So I see both sides of the economy, from decreased buying power of my earned income to up and down fluctuations of our assets. Right now with QE, the classic assets of the investor class (stocks, bonds, real estate) are doing better than the disaster hedges (cash & precious metals).

Roddy pointed out that by European standards, we have high home ownership. Yes, and Europe has deeply imbedded welfare Socialism. We can expect the same to happen here if we continue to ape Europe.

I just got home from the very nice house our Daughter and her Husband now own. They are early thirties, with good government jobs. (Our Daughter is on leave to care for her infant. She has until a year from now to go back to her old job.) They will have about 35-40% equity in the place at the current price. I’m not sure if they would have as nice a place as their new home if we hadn’t helped them some, but I do know they would’ve had as nice a place as my Wife and I have for which we got no family assistance to purchase.

If you are in your 50s or 60s, I urge you to consider helping out your married children get a place when some sanity comes back to the housing market. If they already have a starter property, you might consider helping them to move up as my Wife and I did. it’s easier to jump to a bigger horse on the merry-go-round than to get on while it’s going.

Joe

Back on the topic of landlord nation and rising rents: what I’m hearing in the field, both among some very large scale property managment firms and also in the mom & pop landlord community is that more and more tenants are running between 3 -5 months behind in rent but rather than start eviction proceedings, they are opting for work outs to avoid legal costs, court delays, repair expenses and the possibility that the next tenant will be even worse. Wages are declining, rents and consumer prices are rising. The big picture does not bode well for So. Cal. landlords. Frankly, I would be seriously nervous to be a landlord in LA county right now. I mean, what would happen if the tenants of any given building or apartment complex started organizing and demanding lower rents or just stopped paying? (Okay, maybe it would never happen — but it could). With all but 4 courts handling evictions now closed from state budget cuts and no better replacement candidates for tenants, what would the landlords do? I can’t help thinking the big picture doesn’t look so rosy for landlords or investors, and that counting on 3% annual rent increases is downright delusional.

Housing “Recovery” Endgame Escalates

http://www.zerohedge.com/news/2013-09-23/housing-recovery-endgame-escalates

Tank baby, TANK! Hopefully The Bernank or Mr. Yellen raise interest rates more – that way when my lease is up in June being a first time home buyer I may have options…or I’ll just rent again until it unwinds.

@Xia: you’re instincts are right. It could happen. What could a landlord do if their entire building(s) organized, especially here in L.A. county where decent paying jobs have been evaporating for years?

That’s all about everyone who SOLD the banks’

mortgage bubble bearing under the Liquidity Trap

combined with high net interest margin.

They can’t buy take advantage of the free reserves

and everyone’s expectation that once rates rise

from real neg. less principal will be required for comparable

return.

They expected to use their proceeds to earn more than their

rent. They’ve faced “hand it over” as a policy along with their

Mumsy’s and Dadsy’s, who’ve surrendered their retirement

nest eggs’ earning power. Everyone’s default decision upon

waking up has been real neg rates for safe money.

Being forced into a casino economy is really still alien for Americans.

The mortgagors duped into putting down 5 and 10%, while unqualified

in the first place, as the loans were simply sold, should of course have

non-recourse. Free enterprise should be a la safe amusement park,

and hedging should be for economic efficiency, not the primary means of

profit by calculation and encouragement.

Case Shiller Y To Y In Line Increase, M To M Miss

Zerohedge, 9/24/2013

Has The Market Been

Dominated By All Cash

Flippers Seeing An

Opportunity While Inventory’s

Held Back?

http://pages.citebite.com/v2q1m2c3v2yti

And

http://www.doctorhousingbubble.com/mortgage-rate-shuffle-housing-market-trends-applications-rates-finance-money/#more-6836

Suggest An Absence

Of Much Else.

Will The Flippers Skedaddle

With Rising Interest Rates?

Precisely How It Works

http://pages.citebite.com/d1i8e3n1t3rpv

With Case Shiller,

Particularly Hand-In-Hand

With “Price Dispersion–”

http://pages.citebite.com/o2c0d2e1j0mlb

Simply Selling Yugos And

BMW’s One Week, Just

BMW’s The Next.

Mtg Apps Plunge

http://www.cnbc.com/id/101025316

Homebuilder Confidence Pause

http://www.cnbc.com/id/101040159

Signs Of Supply Wave

http://mhanson.com/archives/1419

Hitting Pre-Set To Fed Itself Seeing Bubble.

http://www.youtube.com/watch?v=RYcG0uXppQM&t=14m10s

With Shadow Inventory

Like This,

http://www.keithjurow.com/excerpt-from-5th-issue/

Who Needs

Residential Shadow

Inventory?

As To The Flippers, That’s Largely

The Bankers Themselves Buying

Released Foreclosures Along With

Fed Mortgage Purchases, And That’s

Getting Turkey’d.

http://henryckliu.com/page117.html

Was Simple Condescension

Laid On Top Of It.

http://landscapearchitecturemagazine.org/2013/06/03/istanbuls-awful-plans/

Predictably

People Felt Insulted And Threatened, Though

The Vulnerable And Victims

Of Cronyism Generally

Feel That Commonly.

http://www.multiurl.com/ga/8_6_13_Evidence_Of_Illusion_4_Propping_Last_Bubble_Selling_Liqui

http://www.multiurl.com/la/Self_Defeating_And_Profitable_Adversity_Created_Too_Great_Too

http://www.multiurl.com/ga/Self_Defeating_Ill_Conceived_Bailout_Of_The_Bubble_Makers

http://www.multiurl.com/la/Self_Defeating_Ill_Conceived_Bailout_Of_The_Bubble_Makers

As I indicated in another column here, I’m pronouncing charade

the Jean-Luc Picard way.

also:

http://www.keithjurow.com/etf-alert-article/

Can someone please explain how the following house which was last sold for $496K is now listed as a short sale for 625K. I thought the whole point of a short sale is for the property to be sold for a price lesser than the last loan amount.

http://www.zillow.com/homedetails/684-Alameda-Dr-Livermore-CA-94551/24938113_zpid/

I love what this article is saying, its becoming a nation of renters! Rental prices going up, up, up! Even as people’s incomes fall. I own a 2 bedroom condo in Orange County, CA that I rent out and I love it. I luckily have great renters in our unit, and we have not increased the rent on them for the past 2 years, but I think next year 2016 we will increase it by $100/month. That is low, we could get $200 more easily, but they are good renters so we won’t do that 🙂 I love renter nation! If you are a landlord you are screaming heallz yeaahh baby!

Leave a Reply to QE abyss