Global housing bubbles unite: How easy debt has created the first ever worldwide housing boom and bust. The busted, the leveled, and the booming.

Economic history is a fascinating subject. Yet in our modern day of instant news and second to second market analysis, it seems like the media is bent on skimming over on only what is going on at the moment. Even the deepest financial crisis since the Great Depression is now gone into the vortex of cultural amnesia. What is interesting however, is that many countries around the world being incredibly different culturally, went down into the rabbit hole of housing mania as well. If you ever think Southern California home prices are outrageous, you need only look at Northern California. If you live in the Bay Area, all you need to do is look at Canada. There has never been, from all the history I’ve reviewed, of a universal and unified housing bubble that touched nearly every continent at the same time at such a big magnitude. Let us take a trip around the world and see what other housing markets are doing.

Those in bust mode

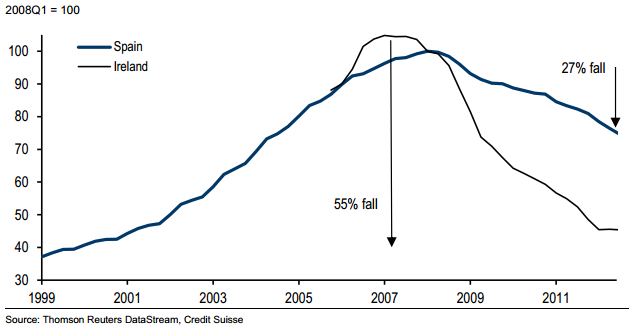

Two countries with giant housing bubbles that are still in the bust phase are Ireland and Spain:

Home values in Spain are now down by 27 percent from their peak while in Ireland, housing values are down a stunning 55 percent. It looks like prices in Ireland might be hitting a bottom but in Spain, given that over half of their young are out of work, it might be hard to see this picking up anytime soon at least from domestic demand. Easy money, fast building, and inflated prices.

These are a couple of markets that are still deep in the doldrums. It is hard to see these turning around anytime soon but if they do, the Irish housing market is likely to come back first simply because it has fallen so dramatically and popped a couple of years before that of Spain making prices much more affordable to those living in the country.

Those leveling out and turning around

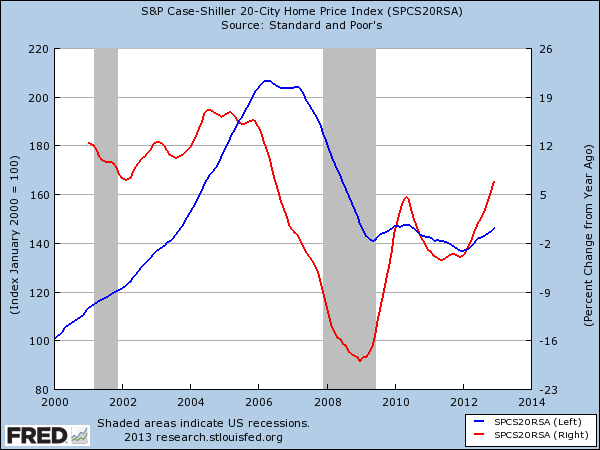

Believe it or not, the US overall has hit a trough:

US home values are now down about 29 percent from their peak and are up over 5 percent year-over-year. As we mentioned many times, in the vast majority of states purchasing a home in the US isn’t a bad move. Given the giant subsidies in mortgage interest deductions (not always utilized fully), cheap rates, and the ability to build equity it is a wise move if purchasing at a right price. This applied to a generation before us and applies to the market today. However, in some hot markets like in Southern California the typical buyer simply cannot compete with the all cash buying from investors. Someone in the industry mentioned to me that those that buy with FHA insured loans are taking the crumbs of what the investors don’t want which are typically not the best places. The deals are rarely going to the typical family looking to buy.

Yet this is not the case for the US overall. Housing markets in many places are very reasonable and ironically, many of those states are the states with little to no investor activity. California has had about 30 percent of all purchases being made by investors in the last few years (versus a rate around 10 percent or less being the case for more stable markets).

The above chart of the 20 City Case Shiller Index is a reflection of the aggregate, not regional areas that may exhibit more bubbly behavior (i.e., over bidding, emotional pleas to sellers, all cash buying, and high flipping rates).

The booming

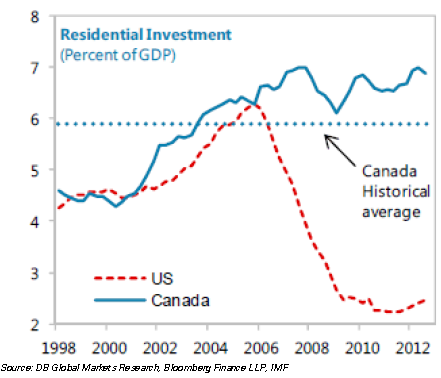

Canada is one of those housing markets that simply keeps going up, although it is starting to show massive signs of frothiness. Any time I bring this up, I get a good amount of comments on how “it is different†up there (or how we are different down there). In the US, even prime areas took a hit and the overall US market is still down about 30 percent from the peak. Zero correction has hit Canada and a big part of their economy now relies on housing:

At the peak of our insane housing market, residential investment as part of GDP made up about 6 percent for our market. In Canada, it is now inching closer to 7 percent. The historical average in Canada has also been higher. But what about homes already built pushing prices up? We’re not the only people seeing this:

“(Canada) A severe economic shock, such as the kind that hit Japan in the early 1990s and California and Nevada in 2006, would have to knock Canadian housing prices down by 44% to cause securities linked to Canadian mortgages to lose the highest ratings assigned by Moody’s Investors Service.

Such a house price decline, were it to happen, would be driven primarily by the phenomenal upswing in Canadian home prices over the past decade, Moody’s said.

Canada joins Spain, as well as the United Kingdom and Australia, in the ratings agency’s assessment of countries where growth in housing prices over the past 10 years has driven their values away from sustainable market fundamentals and into “overheated†territory.â€

Like the Endless Summer sagas, you can technically go around the world and chase housing bubbles into perpetuity!

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

62 Responses to “Global housing bubbles unite: How easy debt has created the first ever worldwide housing boom and bust. The busted, the leveled, and the booming.”

Where austerity is most felt, busts are on-going. Check out Greek real estate as well.

I’ve seen that Ireland has gone about 7.8% positive in exports lately. So they may have bottomed. But go to Spain and look at all the condo’s they built from 2002 to 2007! Way over-built. I’ve also seen very cheap prices in Portugal.

I still can’t believe we are going to have a second bubble in the same asset class within a decade. That Bloomberg cover that read: “Flips. No look bids. 300 percent returns. What could possibly go wrong?” nailed it. Our short attention span ADD nation is primed to get taken again and again.

However it seems that with volume cratering the specuvestor is the main victim/volunteer for this crash. When flip profits and rental yields dry up, probably within the year, we’ll be back to 06-07 with a crash picking up steam. Get ready for the mother of all bailouts. Will the majority even care to notice?

“It’s different this time”

The last run up was fueled by easy credit and lax underwriting. When the game of musical chairs stopped, people were simply walking away from their homes. It was a no brainer. ~40% of home sales in 2011 were distress sales, ~25% in 2012, will be smaller in 2013.

This run up is filled with cash buyer 30% and qualified buyers. A 10% dip won’t cause distress sales if the buyer has 20% down. A 15% dip won’t cause an investor to sell if rental yields hold. Even if rental yields fall along with housing prices, it won’t necessarily mean it makes sense financially for an investor to sell. ie ROI of 3% instead of 7% over 5 years may better than realizing a 50k loss today.

My point isn’t that a housing downturn CAN’T happen, but if housing does happen to turn south, the falling prices will be even stickier and slower than last time due to the makeup of the homeowners.

Prices will be no more sticky during the next crash as they were during the first. These hedge funds will dump the properties as soon as Obama pushes through lowering the FHA qualifying standards. Some people still don’t get it, this is about bailing out the banks and NOTHING else! If acceptable returns were to be made on gulf SFH rentals it would have been done ages ago. The hgedfge funds are merely functioning as the middle man so these toxic “assets” can be passed from the banks to the FHA. When the crash comes 2 groups will be holding the properties, specuvestors and FHA (THE NEW SUBPRIME) borrowers. The velocity of this crash might be swifter than 2008 and WE WILL end up with prices below the 2010 trough, though maybe only by 10-15%. If you accept the simple fact that the whole charade is for the scope purpose of saving the banks from their losses while having a select few benefit from the trasnsactions, the endgame is crysdtal clear.

Good points made here – but here’s one you missed.

As prices continue to go straight up, at what point will investors decide a 100-200% immediate return via selling out is preferable to a 6-8% annual return via renting?

If a few of the big boys try to race each other for the door, this could turn around very quickly.

Also, how many buyers today are putting 10 or 20% down? 3.5% down FHA loans are king right now. A 10 or 20% dip will result in a lot of these folks walking.

True, if “prices keep racing up” investors may choose to sell and take the profit instead of collecting rents. That sets the price they bought at as a bottom. If numerous investors try to take advantage of short-term capital gains that will absolutely slow-down the increase in prices, but that doesn’t mean we’ll see a crash.

The recent breakdown in housing is something like: 34% cash, 23% FHA. Leaving 43% conventional.

Even if an FHA buyer were to experience a decline in the price of their home and was underwater, but purchased at or below rental parity, would they walk away?

Back in 2005 -2007 when homes were nowhere near rental parity it made complete sense to walk away when underwater because you would pay less monthly by renting. What’s the point of walking away if you’ll be paying a higher monthly payment?

A market that’s at least 50% “investors”? Does anyone think they’ll hold their investment at 50% to 100% gain? Just because it has a yield of 7% does not make it immune to being sold when there’s a hefty gain on the table. Actually, investors are far more likely to head for the exits when things have risen so sharply.

RE:SWC

This is my exact point LOL! The Wall Street Sharks are not in a slow and steady profit mode and never have been. They are in and out, maximize the profit (usually by frakking someone over 🙂 and on to the next opportunity. This is why the coming lowering of FHA standards is the key. they won’t completely bring back liar loans, but you will see FHS loans based off of multiple income streams of low FICO borrowers putting nothing down. When things teurn south these will be your new squatters. Here’s how this is gonna play in order:

1. RE booms through early 2014, Fall 2014 at the latest. Probably the former.

2. A stalemate is reached as rents drop due to the increase in inventory and the last of the greater fools qualify for their FHA loans

3. The smart money completes its exit from the market. It began exiting late 2013 and now has left the market with only greater fool FHA borrowers and specuvestors.

4. The market starts declining with prices dropping immediately to Pre-Bubble 2.0 lows as the FHA (subprime) market is dry and the agency itself is in the midst of a bailout.

5. The slow motion train wreck resumes as forclosures are dragged out behind the new regulations and interest rates rise as even the Great Helicopter Ben could not defeat the bond market.

6. Hello 2010 prices minus 10% or so along with much more government debt as the bailout of the banks is complete. Not a single bad mortgage remains on their books as they have been unloaded to the FHA in their entirety.

7. SUCK IT TAXPAYER!

MB, all good points. A big crash isn’t going to occur because of the makeup of homebuyers from the last few years. The all cash and big downs have nothing to worry about. Even the 3.5% FHAers who bought a few years ago likely have ~20% equity at this point (3.5% down, ~5% principal paid, ~10% appreciation).

Most importantly, the PTB will NOT allow a big drop in home prices as witnessed from the last 5 years…anything and everything will be done to prop housing up. A recovering housing market is the key to a “perceived” economic turnaround. When people constantly get bombarded with “expected 10% rise in home prices this year” they start feeling better about spending money on things and this is exactly what the Fed, government, bankers want. It’s really not that difficult.

So anybody waiting for “the big correction” to finally happen, don’t hold your breath!

You obviously don’t understand that FHA loans have been a huge component of the mortgages out there. By leaving that important fact out means you are either stupid or a RE shill.

Annnnd cue Blackstone beginning the shift to dumb money – http://www.zerohedge.com/news/2013-03-14/landlord-blackstone-rushes-capitalize-housing-bubble-launching-first-ever-reo-rent-s

MB, you make some very valid points about why the next downturn won’t be as swift or as bad as the first. NihilistZerO is wrong.

The big banks had so much terrible backlash against they from the 99% marches and sit ins a few years ago… that i don’t think things will be so peaceful demonstration wise if the banks tried to rape the american public again anytime soon.

The makeup of home buyers over the past few years have been WAY different than the bubble era. The majority are all cash buyers and those with 10, 20, or 30% down payments. Sure, FHA loans have become the new subprime.. but they are a smaller percentage of home buyers than the old subprime market by far.

Not to mention, if prime borrowers in the past came to the table with no money down and liar loans.. so practically all buyers in 2004-2007 were subprime in that respect.

A 10% drop below 2009 or 2010 home prices won’t devastate anyone. Even FHA buyers that can afford their monthly payment might cringe, but will easily swallow that bitter pill.

Rental Parity will keep those with homes from moving out. I predict gridlock and low inventory for MANY MANY years to come. People who want to move, but can’t… buyers who want to buy, but can’t find a home, and renters who are stuck with yearly increases like clockwork.

No big crash in home prices??? I guess 2007 to 2010 didn’t happen? Short term memories make for bad investments. The Fed and govt are reactive tools. They never front-load a solution.

I am starting to hear more loose loan ads all over the place. This is a strong bounce. The investor clubs are going crazy and worrying, all at the same time. Why, because they’re seeing everything they saw in 2005, but happening right now. And hedge funds are driving this baby, hard. You think those guys won’t dump?!?!

NihilistZerO: Curious, what make you think Obama will loosen FHA requirements. The trend has been to increase the minimum FICO score required and increase MIP, making FHA loans less attractive. That’s the current direction it’s been heading for the last decade and while a loosening is possible, everything I’ve read about it is contrary to what you wrote.

JMac: Read my post above 5 hours previous to yours. As I stated, FHA loans are 25% of the market.

“The big banks had so much terrible backlash against they from the 99% marches and sit ins a few years ago… that i don’t think things will be so peaceful demonstration wise if the banks tried to rape the american public again anytime soon.”

Surely you jest here – unless I’m missing something, not one banking or government official has gone off to jail for their malfeasance regarding their roles in the financial meltdown of the last decade. Quite frankly, I believe they could give a rat’s ass about whatever the public thinks, they’re still handing out massive bonuses for performance targets that have been primarily achieved via the use of taxpayer monies. How about people like Mozillo? What happened to him, you may ask yourself? Nothing, and he got to keep hundreds of millions of dollars of his ill – gotten gains. The reason? The bankers are joined at the hip with their governmental overseers, and it doesn’t look like that dynamic is going to change anytime soon.

Lord, doesn’t the 10% appreciation you propose go the the flipper, not the recent buyer? It’s been well-documented that the FHA buyer hasn’t gotten the deals over the past 18 months; instead, they are over-paying in order to beat the all-cash investors or buying quick flips. If you rationalize what has happened to the FHA buyer over the past 36 months, I’d bet they are hanging on by a thread.

“Back in 2005 -2007 when homes were nowhere near rental parity it made complete sense to walk away when underwater because you would pay less monthly by renting. What’s the point of walking away if you’ll be paying a higher monthly payment?”

All the folks I recall who either did walk away or were contemplating it weren’t thinking about rental parity as a part of their decision making. They all had various reasons for wanting to live somewhere else but couldn’t sell without taking a loss. In fact, some people I know simply were pissed that their “investment” took a dive and wanted a better house which was then priced less than their original house.

Per usual, the rental parity concept continues to be overstated in its relevance to all micro circumstances and understated in its subjectability.

DFresh is spot on with the statement “It’s been well-documented that the FHA buyer hasn’t gotten the deals over the past 18 months; instead, they are over-paying in order to beat the all-cash investors or buying quick flips. If you rationalize what has happened to the FHA buyer over the past 36 months, I’d bet they are hanging on by a thread.”

Is there any historical data anywhere on median household income versus rent? Or median household income versus home values?

I’d be curious to see if Angelinos are spending more % of their income on rent/mortgage over time.

Wolfram Alpha was unhelpful.

The yearly Harvard State of Housing Report has a good one.

http://www.jchs.harvard.edu/sites/jchs.harvard.edu/files/son2012_appendix_tables.xlsx (Chart on page W-2 has price to income ratios while W-3 has payment to income ratios)

Here are the cliff notes for LA/LB/Santa Ana Metro Area:

Price to Income Ratio

2011: 5.18

2006: 10.36

2001: 5.06

1996: 4.07

1991: 5.76

Peak: 10.36 (2006)

Trough: 4.06 (1997)

Price to Mortgage Payment Ratio

2011: .28

2006: .70

2001: .36

1996: .32

1991: .51

Peak: .7 (2006)

Trough: .28 (2011)

Who needs to go Spain to see overbuilt condo’s…?

Just look at Myrtle Beach SC … you have 800+ condo/homes/rentals for sale as we speak — the scarey part is, these are the same 800 that were on the market back in 2008 and 2009 and 2010 and and …. the only difference is, they went from $250,000 to $125,000 and they’re still not moving…

–

Why can’t someone build 800 condos in Irvine for 125K? I would actually be happy with 250k.

Why don’t they build? Because Florida has very little regulations in terms of building restrictions. Same too of Texas. Now, California has some of the tightest building restrictions in the country. And places like Santa Barbara have the most draconian restrictions in the entire U.S. Orange County and Los Angeles are only a couple of steps behind Santa Barbara. That is why there is no “…build it and they will come…” in Orange County, Los Angeles, Santa Barbara and the Bay Area.

As A potential home buyer I would love for the market to tank. But I don’t have another 10 years as I lost my previous 10. If I want to raise a family with kids I have to pay the higher price. Or move to some other part of the country more I’m not going to enjoy my life. This is it. Time is up, it’s pay now or flush my life away.

This overpriced housing is unfortunate for everyone. Why I can’t afford a newer clean home on a six figure income is beyond me. Housing is ridiculous, add in taxes, mello rip off, association fees, and I can’t afford a home.

And I don’t have family money nor can I share my home with all types of in-laws.

With everyone thinking housing is an investment it drives the market up, so its no longer a place to live and raise a family.

I would not care if I didn’t make one dime on my Home as an investment. I just want a safe place to live and raise a family that I can own when I retire so I am not homeless.

Wow, the American dream, seems more like a dream every day.

Pardon me for pointing out what may be obvious, but the belief that you must own a home is part of the problem. The only difference between you and the sheep is that you’ve not yet been willing to act on prices that seem unreasonable.

No one has to own a home. Not even if one has a family must he own a home. That whole kids need a house thing is a bunch of marketing propaganda.

Your life can have the same meaning with or without a deed to some land. I feel your pain and there’s a lot of bullshit going on, but you can be smarter than the herd if you choose to be. Let them overpay for hype and be slaves to the banks while you forge a better path that includes renting for some period of time. Ask yourself how often impatience pays off.

Finally someone who isn’t drinking the Kool-Aid here!

Well put Joe. A friend gave me some great advice a few years ago: “A house is a building. A home is the feeling. You can rent and have a home with great memories.”

We’re renting for 2 more years, saving more for a down payment, staying out of debt and building our credit. And yes, we have 2 kids.

Thanks, that’s true. I do rent, I have cash, I’m just more disgusted with prices then I am with the ability to own a deed to land. The owning part is more for the 40 year picture then the next 5. I was thinking that homes shouldn’t be such a burden to own, it’s not healthy. Also, renting in LA sucks, lots of trash properties.

I’m with you, Sean. Everywhere I’ve looked in L.A. for years is just overpriced junk or overpriced mediocre regardless of renting or buying.

The longer this goes on, the less attractive the region becomes for talented people and businesses looking to locate/remain here. Climate isn’t everything, just ask coastal Greece, Italy, and Spain how good business is.

Joe, it would be practical to rent as opposed to owning but depending on where you live rents are/have gone up. I live in the SF Bay Area and rents have gone way up in the past 12 months but wages have not. Sure, people are going back to work but most incomes (90%)are remaining the same. The greedy large apt complex owners are raping good people who are still struggling to get back on their feet. Unemployment seems to be retreating but depending on what you read many people think the unemployment is misleading cause many people who were on unemployment are not filing anymore and many people going back to work are taking part-time jobs. I would like to be hopeful for a rebound but it’s not hard to read between the lines. I’m fortunate that I own my condo but there are still many unfortunates.

A-Men.

If you don’t care about making money on your home, why not rent for half the price of paying a mortgage? Put the rest into your retirement, and take a nice vacation every now and then with the kids. You don’t have to choose between flushing your life away and flushing your money away.

Exactly my thinking. Sillycon Valley has insane prices but I’m getting too old to wait it out. Got two kids that are in the schools here and rent was going up 10% a year. At least I know what I’ll be paying for the next 30 years. It is somewhat of an inflationary bet. Been renting for the last 6 years and just wanted some stability.

There is no reliable fixed monthly outlay in the case of a owned, mortgage, or rent. Property taxes are a variable for which you have no control. Rents don’t always move upwards.

Stability is not defined by a land deed but rather by the state of your health, employment, and other circumstances.

Joe, due to Prop 13, property tax hikes are capped at 2% here in CA. I’d be willing to bet my life savings that rents have increased at a rate much greater than 2% in the last 35 years since Prop 13 has been in effect.

LB, I’d be willing to bet my life savings that Sacramento and local taxing authorities throughout California are hard at work in the process of unwinding the tax cap party of the past few decades.

Rents are mostly guided by supply and demand whereas taxes are completely guided by political processes. Rents can move in any direction so it’s not a given that they always move up.

I doubt today’s buyer is thinking about retirement nor are they thinking they’ll pay their house off. Inflated prices equal higher property taxes that retirees will struggle to pay.

We’re being manipulated Sean. The Federal Reserve wants you to feel the way you do so you will go out and buy a house. It’s no secret. It’s called Perspective Economics and Bernanke talks about it often.

+1

it’s incomprehensible. it doesn’t make sense. we’re in the exact same boat in the same area. we’ve decided to stay here another 3 years then depart to fairer shores. although we’ll be moving to an above mentioned bubble country. but at least we won’t have to sit in our car for half our day to get anywhere here in OC. bizarre ‘planning’ around here. I like Irvine and is the best around here but man the driving is just too much. and kids hate it. my kid told me the other day when he grows up he will never drive a car and walk everywhere. he also told me he never wants to move out of home. good chance of all of that happening at this rate!

I don’t understand the feeling of needing a home to raise a family….. I’m 33 and my wife and don’t care if we ever own. We are not going to pay for what we feel in our area of the world, Sacramento, is an overpriced asset. So we will rent, save and invest until we feel the house we want in the area we want is priced more accurately. Who knows what that is but I know a heavily manipulated market will not accurately value assests. I don’t need to own a house to live and I can do plenty other things with my money to protect against inflation and grow it.

Maybe you’ll understand once you’ve set up your six year-olds bedroom in another house for the fourth time. Renting is unstable. Actually, by the fourth time you are well and truly over doing it you just leave most things in boxes and shove them in the garage. Buying is more about feeling like you aren’t an a-hole loser who can’t let their kid paint his walls. When your kid can’t even paint his walls you start questioning your usefulness, right? Like, I can’t even control the color of my goddamn walls. Plus, moving a couple is on a different level to moving a family with kids. If I could buy and never have to move again I’d be pretty content.

“If I could buy and never have to move again I’d be pretty content.”

Just wait until the family running the large unlicensed day care or the power couple who work nonstop with teenage son/daughter with raging drug/emotional problems moves in next door; you could have a very different perspective about never wanting to move again/perceived contentment of home ownership. Good times!

@Drinks yeah you’re right actually. We’ve moved from rentals in the past because of bad neighbours. Years ago before kids we lived in a tiny street in LA and the neighbor next door rented out the house directly across from us and had a fully fledged business running from the two houses. Pick-up trucks moving merch, sales guys parking on the very narrow parking street all day and night, and then the neighbor also had a side predilection for just released from prison meth-head trick boys. We still keep in touch with other neighbors and they tell us it all still goes on but the trick boys are a little more brazen with the *stuff* they do on the street. This guy completely ruined a great place to live. No amount of complaining to him or the city changed anything.

Another reason to not buy now. After a few bad neighbors (including current) I decided if we buy to thoroughly stake the place out at all times of the day. I am serious when I say I could go as far as hiring someone to get me info on the neighbors of a place I buy. While you can’t check for everything you sure can check a lot. Nothing worse than a bad neighbour.

Everything is unstable. Just ask anyone who has foreclosed on a house. No guarantees.

Paint your walls whatever color you want and put it back after you move out. Big deal.

And seriously, your kid has to paint the walls?

“They call it the American Dream, because you have to be asleep to believe it” George Carlin

“The American Dream…” that’s all it is – a dream.

I’m sorry, I don’t see where “overpaying for real estate in Los Angeles” is referenced in these definitions of the American Dream (per wiki):

In the definition of the American Dream by James Truslow Adams in 1931, “life should be better and richer and fuller for everyone, with opportunity for each according to ability or achievement” regardless of social class or circumstances of birth.[1]

The idea of the American Dream is rooted in the United States Declaration of Independence which proclaims that “all men are created equal” and that they are “endowed by their Creator with certain inalienable Rights” including “Life, Liberty and the pursuit of Happiness.”

That’s what happens when we equate homeownership with “happiness”.

But that’s a spiritual thing. 🙂

I can really identify with some of the posts here. Especially the angst filled kind.

You see, i was in the same psychological boat. I call it the “NO BOAT”

What’s inside it is a ton of negativity, indecision, fear and regret.

Its easier to talk yourself out of something, then into something, right?

Now then, this is mostly aimed toward Sean’s comments. Hey buddy, ease up.

Depending on where you live, and the type of work you do, there are options.

First and foremost being due diligence.

Okay, its a really tough buyers market. We agree.

But from your post it seems that you are presuming that you will have assoc fees and also Mello-Roos, ect. That may end up not being the case. What i am trying to convey is, if you take your time, view ALL your possible options, and take at least a year diligently getting to know your local market and objectives,(and i do mean knowing nearly all possible aspects) you will find the right situation without feeling as if you were ripped off. I knew absolutly nothing about real estate, the types of transactions, or what to expect 2 years before buying. When you satisfy THAT, then its time to get serious.

Even so, i worked with a long time buddy who happens to be an agent, i feel and felt like it was my job too find the right home, at the right price, and too be FULLY informed.

If you commit too that, things will turn out fine. Also, if you have a stable income, whats really holding you up? Besides, you may already be paying a price by not buying, in that you have to listen too the wifey Bitch all day about not being in a house, right?

You must be a realtor.

Careful, anytime you call anyone a RE shill and/or troll here, someone will immediately pounce and call you “bitter” for missing the alleged bottom of the market – like clockwork.

Nope. Im not a realtor. Just someone who kept telling himself he couldnt afford an awesome quality home in a safe neighborhood, (Even on a six figure income)at a decent price. But i found it. It just took 14 months, thats all!

I should have been more clear. You must become a realtor.

“Besides, you may already be paying a price by not buying, in that you have to listen too the wifey Bitch all day about not being in a house, right?”

Shades of “Suzanne researched this.” Never gets old.

“Also, if you have a stable income, whats really holding you up”

that stable income could dry up at any moment AND rent is 1/3 the price.

Wow, you sound just like my realtor. Although he did add a bit of spice to our conversation when he was trying to get me to put down an offer on a overpriced 1,600 sq./ft. home for 525K. He knows my budget is 500K. He said, that extra 25K over 30 years only equates to about $50 extra on your mortgage payment. Needless to say, I dropped him like a bad habit.

Canada and especially Vancouver are doomed.

Vancouver will be just like Toronto Bubble in the 1980s. A 50% decline in downtown core between 1989 and 1996.

90% of life spent working sleeping commuting; hardly see spouse, can’t afford kids, hardly see kids if they exist because always working/commuting to afford lifestyle but CALIFORNIA HOME OWNERSHIP a dream Weather stainless steel appliance granite countertop worth sacrifice go to beach stand in sun don’t lose job.

“True, if “prices keep racing up†investors may choose to sell and take the profit instead of collecting rents.”

And of course they will: Good profit now is always better than potential profit in 10 years. It’s the root of quartal capitalism.

Sure, some will take the quick profit… And inventory might increase a little and put downward pressure on prices… But as soon as the first investor can’t find a buyer.. he’ll take it off the market and continue collecting his rental returns.

We are bouncing along the bottom…. No one is getting rich or going poor in the real estate market for the next decade.

This is just one example but I’ve been keeping an eye on it. I have a realtor sending me listings for rentals and sales. It was bought last on Oct 26 2012. It was on the rental market for 126 before it was pulled seven days ago and put on the sales market. For $50,000 more. They were asking $2450 as a rental. Dropped a whole $50 to $2400. To buy it now with 20% down, 30 years is $2230. FHA is $2992. The new sale went pending in about 7 days.

http://www.redfin.com/CA/Orange/581-N-Pageant-Dr-92869/unit-E/home/5689486

“And of course they will: Good profit now is always better than potential profit in 10 years. It’s the root of quartal capitalism.”

Some may, some may not. It depends what they’re looking for. You can see examples of this in apartments or other RE investment vehicles that were bought in the 1990s. Investors could have realized 100-200% gains by selling but some chose not to and still own today.

Uh, did Ben Bernanke withdraw any of the ’emergency measures’ he put in place over the past 4-5 years? Has Washington taken any steps to bring our fiscal deficits under control? You let interest rates ‘normalize’ by withdrawing QE 4ever and the bottom is going to fall out from under this Potemkin economy we are living in. Nothing has been fixed, its gotten worse. Europe and Japan are in a race to see which economy has a debt implosion first and China and the US are not far behind. When it happens it won’t be a case of how far do housing prices plunge rather it will be a case that there will be no more housing market.

I am really happy that i rent a home but have to admit that i am a little bit disappointed

that i missed the boat in 2009. Was not be able to have enough cash back then. Now i am dreaming of having a house in the US but i am sure that this is not a good moment to step into the market because the increase in value goes up way to quick. The fact that this market t the moment is not an organic market but an over-manipulated one makes it for me easy to conclude to wait some years and save money by searching other opportunities.

Here in my country the bubble has not burst yet. But houses 180.000-250.000 class are on the market for a very long time. Meanwhile the government is trying to do everything against an inevitably crash within time. Taxing, keep taxing, finding-out new taxes, and so on…

Europe is sold already and the only ones who make profit are those who are above us.

Middle class is always been the cow with the best milk. Only difference between Europe and the US is that here the bubble begins to burst. In the US the bubble bursted in 2008 and is transforming in another bubble. Just like popcorn in a pan, everywhere bubble go up and burst. Maybe we could see one big global bubble burst in the future, one that involves US, EU, China, Canada and Australia.

I think we are in very interesting times, look back to what has happened in history. I think we are the year 1932 in comparison with nowadays. The world is going crazy nowadays, we need a big clean-up. Only 700miles from my city people are shot on the streets. No difference with the United states, but at least they don’t burn the corpses on the streets to hide the identity of the victims. In European media papers, we see only the bad things that happen overseas but they are trying to hide their own problems. Look to what happened in Marseille. Crazy world…

Leave a Reply to JQ