California Investing and Housing 2009 Forecast: The Rise of the Bottom Caller. Bottom Investment Callers out Again, Foreclosures Dominate Market, Home Prices near 2002 Levels.

There is now new 2009 evidence and data points showing that the housing situation is quickly deteriorating in California even more than one would have expected. It is one thing to say that the market is flooded with foreclosures as if the Red Sea was parting but it is another to blur the facts and revise history to cover up the finance, Wall Street, and real estate industry dirt. I’m starting to hear a rather ubiquitous meme going around regarding the causes of this economic mess. The argument goes something like this; the government wanted to push homeownership so lenders (because of the government) went out and made loans to subprime borrowers in the inner city and that is the main culprit that set off financial Armageddon, which now looks like we are teetering on a the verge of a financial Great Depression. This argument has an additional component which is fixated to the point of calling in Sigmund Freud on the Lehman Brothers collapse and blaming the government for letting them go under. The underlying implication is that if we had only saved this investment bank, we’d all be rolling around in the yellow fields of daisies.

I find the cognitive dissonance of these people amazing. I say “these people” because there is some uniform thought pattern here and I have heard this set of arguments enough where I realize that this is a packaged mentality. These are usually the same people that cry from the hilltops that the government should stay out of business yet when it comes to letting famed crony capitalism go marching forward, they are all for it with a bottle of champagne ready for a celebration. By the way, wouldn’t bailing out Lehman Brothers actually come from the same government they want to stay out of their business? These people are selective about what they choose to believe and will usually throw out middle school intellect arguments and red herrings such as “freedom” or “liberty” since they know most people don’t have the spine to question these catchphrases once these words are invoked.

There is a song called Born Again American which has a message that I think will resonate with many of you. I think many of the battles we will face will require sacrifice from all of us at a certain level. It is just a matter of how much will those in the castles sacrifice?

In fact, letting Lehman Brothers implode was probably one of the few things the government did right last year. Why? I bring you to exhibit A of crony capitalism with Bank of America. On Thursday we find out the “shocking” news that Bank of America required $20 billion additional funds from the government to cover the “unexpected” $15.31 billion loss at Merrill Lynch during the fourth quarter. It is only unexpected to the delusional dingbats smoking the crony capitalistic peyote. So if you haven’t figured it out, we are now on the hook for this crap. That is why letting Lehman Brothers go under was a quick way of letting the market figure out the price of what was on their books. As it turned out, it wasn’t worth much and you might as well try to sell their assets at the local flea market. Now with Bank of America, CEO Ken Lewis is going to get another rude wakeup call when toxic mortgage factory Countrywide starts sucking on Bank of America capital yet we know deep down in our gut that BofA now serves as a conduit for free taxpayer money because they are now “too big to fail.” Yet as we all know, now even those pristine Alt-A and option ARM loans are going to pop like zits in 2009.

I put this out there because of what I have been hearing from more bottom callers and ideologues. First, most of these bottom callers are people that were wrong in the past so their credibility is shot to begin with. Next, they are misguided by their own belief system and really operate under a crony system of business, not any true form of capitalism. Before I dive into the California housing details, let us look at some new guess work made from these “experts”:

“(LA Times) California home builders are among those pushing for a federal tax credit to spur home purchases. Statewide, the California Building Industry Assn. estimates that fewer than 64,000 new homes were built in 2008, the lowest total since 1954.

The December sales total for new homes in Southern California was 79% below the peak sales month of December 2005, when 8,723 new homes were sold.

Although there remains an oversupply of homes, Leamer said new-home construction would soon be necessary to prevent “another mania” in housing.

“We overbuilt from 2004 to 2006, but now we’re underbuilding,” he said. “In four or five years, when the economy is strong again and people come back to the housing market, there may not be enough units.”

This guy has been wrong so many times, I’m surprised people still quote him. First, Mr. Leamer is wrong about under-building. The problem we have in California is a low supply of affordable housing. Incredibly the housing collapse is pushing prices lower which believe it or not, has increased sales in areas like the Inland Empire and has also made homes more affordable to many. What a stunner right? If he worries another mania is going to happen it’ll be because of weak lending standards and not because of the supply of housing. That notion is simply unfounded. The reason California saw prices skyrocket is because people drank the housing Kool-Aid and relied on economist like Leamer who couldn’t see a recession if they were even standing in it. Oh, if you think that is hyperbole take a look at this memorable quote:

“(International Herald Tribune)Â Despite plunging housing values, rising oil prices and credit problems that continue to plague Wall Street, the U.S. job market is unlikely to suffer the kind of steep losses that would tip the economy into recession, according to the quarterly Anderson Forecast by the University of California, Los Angeles.

“We still think an official recession is not in the immediate future,” concluded Edward Leamer, director and co-author of the forecast set for official release Thursday.”

You know the date of the article? December 5, 2007. Bwahahahaha! We were standing knee deep at the start of the recession and he didn’t even know what he was swimming in! Earlier this week Ben Stein was on the KNX Business Hour, a local radio show and he was one of the above people who thought Lehman Brothers changed the entire landscape of the universe and altered his earlier predictions. He is another one that missed the entire housing bubble bursting and recession. You have to be economically blind or suck at your job if you couldn’t see this coming. By the way, the market was already getting hammered before Lehman imploded. The S & P 500 on September 15, 2008 was already off by 23% from its peak and this was the day the infamous investment bank went under. But why let facts get in the way?

The reason I bring this up is because this cadre of pseudo financial wizards are now proposing notions and predictions that make no sense. We should be listening to those who have gotten it right from the beginning. I was happy to see that Nouriel Roubini, the New York professor was getting some airtime on Bloomberg and even made it on CBS MarketPlace. He didn’t simply predict what was going to happen, he nailed it with almost prescient precision. For those of you who have doubts, you should download his testimony to the House of Representative made on February 26, 2008. Here is a quote from the testimony:

“At this point the debate in the U.S. is no longer about soft landing versus hard landing (recession); it is rather on how hard the hard landing will be. An analysis of the macro data published in recent weeks suggests that the economy has already entered into a recession in December 2007. So the question now is whether this recession is going to be relatively short and shallow (lasting two quarters in Q1 and Q2 of 2008 as several analysts suggest) or much longer, deeper and more protracted (four to six quarters).”

He pegged the recession months before many did. Read the entire thing, it adds to his credibility. I want to bring this up because there is a lot of misinformation flying out there and for some reason those that were utterly wrong still have access to the airwaves and TV. Let us now dig into the California housing situation.

California Market Advice:Â Don’t Buy in 2009

I was wondering why in recent days I have gotten many e-mails from readers asking if now is a good time to buy. Seeing the bottom callers emerge from their educational timeout for being so wrong, they think that they’ll get it right this time but this is also the reason why many out there are still sitting on the fence. In regards to buying a home in California for 2009, you should not buy a home. I’ll give you five major reasons why buying right now makes absolutely no sense:

Reason #1 – Prices are Still Dropping  Â

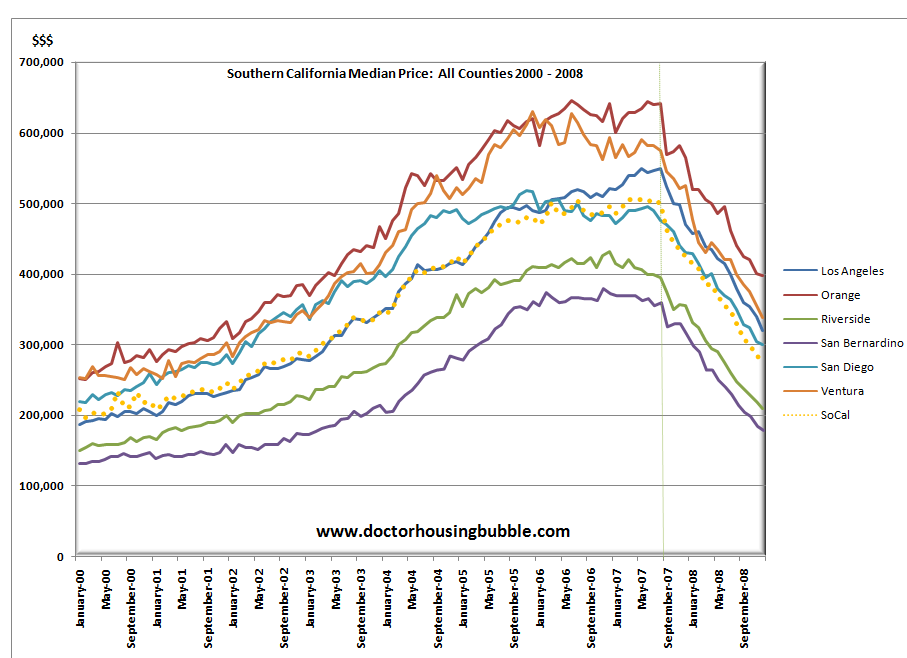

Why would anyone be buying when the trend on housing prices is clearly pushing prices lower? Let us take a look at Southern California since over half the state’s population lives here:

*Click for sharper image

A couple of big trends are emerging. First, Orange County broke the $400,000 median home price mark in December. One county is solidly under $200,000 which is San Bernardino with Riverside inching closer to this level. Like I mentioned before, these areas have a major case of the option ARM psychology going on and this is only going to get worse in 2009.

The fascinating thing is the most expensive county which is Orange, has a median home price of $397,000. I have heard a few (not many) misinformed folks in the lending industry still living in their reinforced anti-reality bunker thinking that not lifting loan caps is the reason we are having all these problems. If they would only look at the median price for all areas, why would we need a lifting of the cap from the Federal government? In fact, the nationwide economy is reeling so they have bigger fish to fry and I assure you since I travel the country often that few people in other states are going to have sympathy from someone trying to buy a home that is priced over $417,000 in California given the current depression like climate.

The Southern California aggregate median price is now $278,000. This is a 44% drop from the peak reached on July of 2007. That is why when I made the prediction that housing will not bottom until 2011, I was looking at multiple data points and also, consumer psychology. If you listened to the delusional pundit crew, it is your duty to write into networks that harbor them and ask for more balanced (and accurate) prognosticators. Otherwise, networks will still feed you the same crap over and over.

You know the last time prices were this cheap? Try August of 2002 when the median SoCal price was $278,000. By the time this is said and done California will have a lost decade similar to Japan in real estate. Think about it. If we bottom out in 2011 and prices are still going lower in the short-term (which they will), we will have a decade of lost real estate appreciation.

Northern California is now in the same boat. In fact, they are worse off since that region is now off by 50.4% riding a median of $320,500 off from the $665,000 peak in July of 2007. The 50% mark has been breached. I just recall a few folks on the Craigslist housing forum back in 2005 that couldn’t even envision Bay Area prices dropping 10 percent.

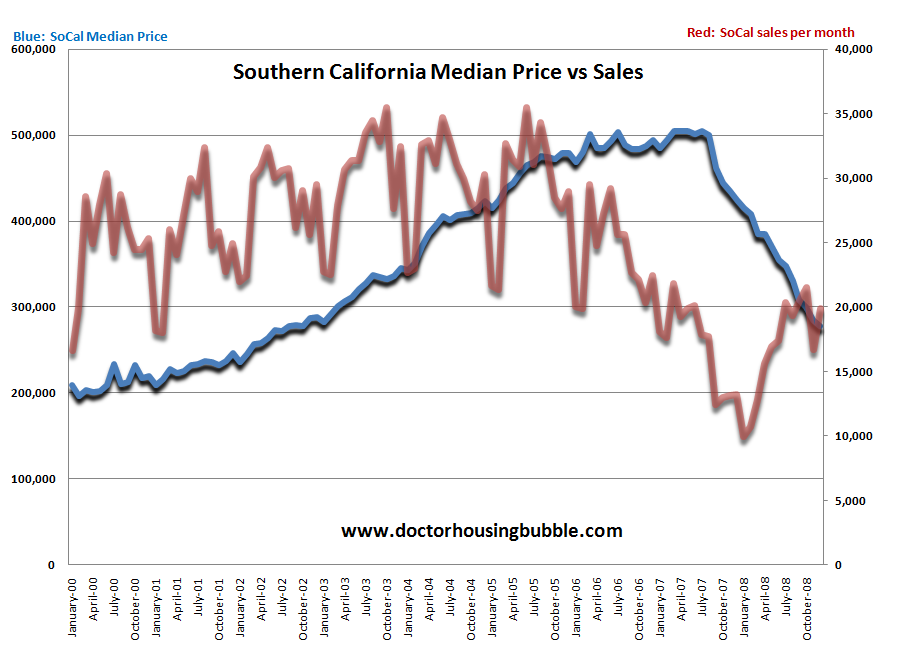

Reason #2 – Sales are Still Low

Sales are all over the map and I’ve seen a few headlines jumping up and down because sales are flourishing. In the Bay Area 50% of homes sold last month were foreclosures and in Southern California it was 55.7%. Foreclosures are the market. Let us see how this looks on a chart:

You’ll notice that yes, we are off the lows of late 2007 or early 2008 but this is simply because of the massive amount of foreclosure sales. This is also a reason why the median price is getting hammered. Sales are still not up to their average levels for the decade. Yet keep in mind that appraisals look at recent sales so comps are getting slammed. It is naïve to look at the median price by itself when the bubble was booming and it is equally deceiving to look at the median price now that the bubble is bursting. Yet we now need to look at the following; local area incomes, home condition, area amenities, area rent prices, and economic prospects. Looking at these traditional measures home prices are still overpriced! Don’t be fooled. 2009 is going to slam California real estate.

Reason #3 – The Economy Stupid

What many bottom callers forget is that our economy largely revolved around the housing and finance sector. Those jobs are gone. The state budget is in an absolute mess and now we are days away from thousands of state workers who will be furloughed and will effectively have a 10 percent wage cut. That is less consumption by the way.

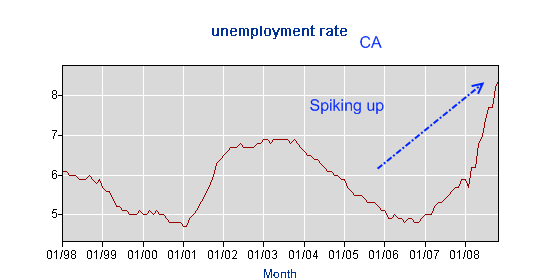

California also has the third highest unemployment rate in the country:

As it stands, the current state unemployment rate is 8.4% which will spike when state data is released next week. How do we know? Just look at the unemployment claims data. If it stays steady or declines, we know why and fortunately many mainstream media outlets are now covering the sham on how the unemployment numbers are calculated. That is, things are so bad even fudging the numbers can’t cover this up.

So if this is our climate, those in the real estate industry forget that people don’t want to buy big ticket items when the economy is in the gutter! Why do you think auto sales have fallen?  Circuit City anyone? The only way people bought this over priced crap for so long was because of easy credit and saving absolutely nothing. This will make this downturn the worst since World War II but hopefully not as deep as the Great Depression.

Reason #4 – Expert Creditability Shot

As I have mentioned above, people simply do not believe the same tired old mantras:

(a)Â Real estate never goes down.

(b)Â If I dollar cost average, I’ll be okay.

(c)Â If you call yourself a “realtor, broker, economist, banker, etc” then you must know about money.

(d)Â If I work hard and play by the rules, I can live comfortably in the middle class.

All these rules are now shattered. Why? The crony capitalist with their de-regulating tools in Washington sold you out over many decades and it is all exploding like a debt filled piñata. Now we are left with one big mess to clean up. We are left with some circus where all these worthless institutions want to shift the losses onto the public without owning up to their mistakes. Look at the $700 billion useless TARP. That first $350 billion only bailed out the bankers and Wall Street. Not you. Foreclosures are still soaring. Unemployment is raging high. The experts are delusional and justify their blurry economic philosophy and think they are capitalist but in reality, they are nothing more than a criminal justifying his deeds to let him sleep at night.

That is why when I hear them blaming subprime borrowers (aka, poor inner city families) or the government for this mess, they forget that the size of the pie falls more in their area of crony capitalist greed. They are nothing more than self-serving plutocrats. We need to distinguish between ambition (good) and uncontrollable greed especially if it falls on the laps of taxpayers who didn’t even share in the upside but are eating up all the downside.

Look at it this way. The Wilshire 5000, the broadest measure of U.S. stocks is now off by approximately 50 percent. At its low it hit below 7,500 which represented a $10 trillion market cap loss. We are now at 8,484 which is near those lows reached on November 20, 2008.

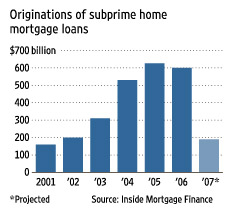

Now let us look at the subprime loans made throughout the decade:

Keep in mind that the market virtually disappeared in 2008. So adding up every subprime loan made since 2001 will yield us approximately $2.5 trillion total originated. So even if banks lost 100 percent of the loan amount which they can’t since the house is still worth something, we realize that the equity markets were a bigger sham by far. Let us assume that the loans were only worth 30 cents on the dollar. That means, that total losses are around $1.75 trillion and that is assuming the worst case scenario for subprime loans. So let us run the numbers:

U.S. Equity evaporation:Â Â Â Â -$10 trillion

Real Estate value decline (peak of $24 trillion residential):Â Â Â Â Â -$5.6 trillion

*Using current Case-Shiller decline of 23.4%

Not including global equities, global real estate, commercial U.S. real estate, commodities, etc.

Keep in mind that subprime loans got recycled by greater fools. Meaning, someone that bought in 2002 and then sold in 2004 shows up in both counts even though the 2002 loan gets paid off in escrow. So in fact, the actual subprime market at implosion time may only be at approximately $1 trillion. Who really knows the exact number but we are close. So above, just in the U.S. alone we can already account for $15.6 trillion in wealth that is gone and you’re telling me that $1 trillion in subprime loans caused this? You really have to be smoking some good stuff to believe that.

Reason #5 – Option ARMs

And finally if that still doesn’t convince you, California is loaded to gills with option ARMs which I will steal a phrase from Warren Buffet, are weapons of financial mass destruction. There is more of this crap out there than subprime loans and this will take a bigger hit on the psyche of many. It may be the final nail.

The importance of this comes more from consumer behavior theory. First, subprime borrowers are highly unlikely to be invested in large amounts with 401ks or IRAs or went crony shopping with Bernard Madoff. No, these people lost their home and that is pretty much it.

Yet many option ARM borrowers and those in the Alt-A category do have good credit and investments in other vehicles that just witnessed a shellacking in 2008. Now, many have to decide whether they will stay in their massively underwater home while they watch their investments crater. Many people doubled down by massively having their portfolios in real estate and finance yet also owned a highly leveraged home. Both are now deep in the red. So do you really think these people, who now have a damaged brand view of housing are going to be ready to leap back in the flame? The only way that is possible is if we bring back more option ARMs or more absurd financing like when Japan started offering multi-generation loans which hasn’t done a thing since housing has been in the dumps since 1990, nearly 20 years ago.

A good fighter for the housing truth and colleague, Mr. Mortgage showed a recent WaMu modification loan that transformed a $1 million loan into an $878 monthly payment! Bwahaha! However, this is only for 2 years then on your 3rd year, the payment goes to $2,633, in the 4th year hits $4,389, and finally in the fifth year you’ll need to cover the loan. In 5 years California real estate will still not be near peak prices! I can assure you that. Unless incomes double in that time, you can rest assured prices will remain low. Kick that shiny glimmering can down the road.

The more time that goes on, the more I am convinced that we are going to have our lost decade like Japan. We’ve already had a lost decade in stagnant wages. California is now back to 2002 price levels. Don’t let the ill informed pundits try to suck you into their Alice in Wonderland world. The only thing consistent about them is they have been wrong for years and continue to be wrong in 2009. At least some things don’t change.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

31 Responses to “California Investing and Housing 2009 Forecast: The Rise of the Bottom Caller. Bottom Investment Callers out Again, Foreclosures Dominate Market, Home Prices near 2002 Levels.”

Another excellent post Dr. Thank you for bringing attention to Prof. Roubini’s predictions. I highly recommend his blog, great reading and insight on global economics. Become a member to:

http://www.rgemonitor.com

Here is one of the best articles I have read regarding to where the housing prices are going:

http://www.rgemonitor.com/globalmacro-monitor/253320/putting_a_floor_under_american_homes_how_low_do_we_go

Keep up the good work!

Great post Doc! My parents are just looking around at houses in the metro L.A. area, their realtor is pushing them hard to buy. They are older asian immigrant couple so I’ve been trying to explain to them all the reasons for not buying now and this blog has helped me a great deal. The biggest thing that hit them was when I explained the Alt-A and Option ARM loans and how these loans would make subprime look like a drop in the bucket. Also they own a business and can see w/ their own eyes how customers have cut back on spending. They won’t be buying until end of this yr at the earliest no matter what their realtard tells them. Keep up the good work!!

There are still countless amounts of delusional sellers out there who put their homes on the market using bubble prices even though comps are selling at half that. The coming Option-Arm resets will be the knock out blow which will send the so called resilient zip codes crashing down. Un-employment will make sure housing doesn’t recover until at least 2016, that is unless .gov steps in and postpones the inevitable.

I agree with everything the Dr. says except for all of this being caused by “crony-capitalism.” This was caused by a combination of a lot of Americans not saving any money, buying more house/car than they could really afford, and the Federal Reserve printing money like it’s going out of style, which causes the purchasing power of the dollar to decline over the years. All of these factors have caught up with us at once. Keep in mind also the unemployment numbers are fudged: not 7.2% currently, but 17.4% (if you add up all of the REAL gov’t numbers.) Things are going to get a lot worse, I am afraid.

amazing how the sun continues to rise every day and life is going on as usual. I don’t see anything different in my surroundings. people still driving, attached to gadgets. Home building has slowed – but new homes going up was not an ‘in-you-face-every-day’ observation.

I read the finance blogs, including this very excellent one – and all have me believeing a pretty doomday scenario.

Yet 99.9% appear oblivious, versus 0.1% overreacting.

Time will tell…..

Things are going to get real interesting, real fast. For example, a 5br + 4.5 Ba, 5600 sqft House in Pacific Palisades, just took over a $1,000,000 price cut to sell.

The house was bought in:

7/2007 for $3,300,000

Just Sold:

12/2008 for $2,200,000 (1/3 off)

http://www.westsideremeltdown.blogspot.com

http://www.santamonicameltdownthe90402.blogspot.com

Guess I’m one of those yahoos looking for a house — moved to California in 2004 and couldn’t afford a home and now we can. Only problem is, we don’t want to pay more for a home than we have to. What is your opinion on Temecula/Murrieta area? Looks like prices have dropped 50% — think they will slide even further?

Great article by the way !!

Alot of good date here supporting the housing trend. What people need to consider is consumer confidence. Everyone of us know someone whom have lost their job in the last 6 months. Even people with money to buy wont buy any time soon because they can’t even besure they will have a job in 2-5 years or may be relocated.

I have been seeing more and more homes being on the market as of last week. People with interest only loans are starting to feel the heat. This Alt A and Option Arm wave is gonna hit hard and it going to take at least 2 years for it to iron itself out. The inland area price is going drop a lot more drastic than the coastal area which is a given. Remember no job = no real estate market. With state budget and even Microsoft annoucing 5000 job cuts in the next year is another knife into the cosumer confidence. The doctor is right about the unemployment rate. I believe it is a lot higher than we are aware of. Keep in mind during the housing bubble alot of constructions jobs around the real estate boom are lost. Many of those people are unmployed unaccounted for, we are talking a whole industry of cash payroll.

The homes in my area were going up approximately 100k a year, starting in 2001-2006. Watching it all was kind of like being hypnotized, or on acid, nothing made any sense. Yet everyone seemed unphased by it.

IT turns out they were the ones who were hypnotized, not me.

What percentage of the population purchased homes after the year 2000?

A simple guess might be 10%. then the question is how much of an effect does 10% of the population have on the 90% who are unaffected by price declines.

Reason #3

California unemployment rate jumps to 9.3 percent

By SAMANTHA YOUNG, Associated Press Writer

Friday, January 23, 2009

California’s unemployment rate jumped to 9.3 percent in December, capping a tumultuous year of massive job losses and a housing slump that has struck most of the country.

The jobless rate announced Friday by the state Employment Development Department represents a jump from the 8.4 percent figure in November 2008.

Dear Comrades,

~

I have some advice to you potential homebuyers that I gave to my brother in Phoenix. If you must buy a home soon for whatever reason, wait until the end of the traditional selling season (May-August). This is the housing equivalent to the Christmas holidays. The best sales are always after Christmas. For housing, the best deals will be had during the fall when sellers are in despair having missed the prime window driving prices lower. There is a seasonality to housing sales as the Doctor’s charts show so take advantage of it.

~

Of course, I still agree with the Doctor that the true bottom is years away. As the saying goes, don’t try and catch a falling dagger. In the meantime, save money and pay off any outstanding debt. With the world economy in free fall, you just never know how this thing will play out.

~

Be brave Comrades!

Hey, someone made an offer on my friends place in hermosa beach. It was only on the market for a couple weeks. I guess there still are people willing to shell out over 800,000 for an older 1500 square foot place?

Wow ! This is The Best Site, Thanks and Keep Up The Good Work.

One person you should quote and provide links to the Commentaries is Peter Schiff who is like Nourini and has been On The Money since 2007. I have done enough research myself to conclude that Subprime was a drop in the ocean compared to Option ARMs and Alt-A loans which are ready to explode and send us for sure into Depression. Today, Toll Bros released a press statement announcing 3.99% Interest after they dropped the prices on their new homes in Yorba Linda CA (Legends) by > $200,000 last week. So here’s my calculation: After all that price drop and interest reduction a 4000 + sq ft home costs about $1.2Mil (without Upgrades and Landscaping) compare that with a home just two yrs old selling for about $1Mil (with Upgrades and Landscaping), next, a 3.99% Int is only about $200/mo lower than a 4.5% Int available these days. That is about $2400/yr or $36000 assuming a 15yr LOS (Length Of Stay). One can find a latter home for a far lower price than a Toll Bros New Home, Who are they Fooling? – Surprisingly Many ! I have seen Saps even in today’s recessionary climate buying everyday but, I refuse to be another Poor SAP! Oh By The Way, my research of a 1 Mile Radius in the zip code 92886 shows over a $Million in delinquent Property Taxes as of 12/10/08. All these homes were purchased for over a $Million at least. So lets Buckle Up and wait till at least 2011 !!!

Yet another great post.

Have you seen the MOS (Based on the last 3 months sales) of $1,000,000+ homes and condos?

So many of these seem to have been purchased in the 250k range in the late 90’s.

I was perusing Redfin trying to figure it out. It took quite a while as I had to break down housing types and prices so that I was able to see the max 500 allowed. When looking at solds, I made sure that the “new listings only” was checked to make it easier to look at them individually.

One disturbing trend that I’m noticing is that many of the listings are actually duplicates. What I am seeing for example is that if a 20 unit building in a “fairly undesirable” area sells for $2,000,000, Redfin shows it as 20 different sales. One sale for each unit at the full $2,000,000 price. They are incredibly easy to find if you sort by $psf and go to the most expensive $psf sold listings. You’ll see the $4,000psf and up 500sf 1BR’s listed all with the same address.

Backing these “solds” out of the equation…I can assure you, if you look at homes and condos for “sale”, you will never see one of these buildings listed. (And I don’t check “multi family” for any of my searches BTW)…and backing out the “overlappers” such as a $2,000,000 home that will fall into the $1,750,000 – $2,000,000 range and the $2,000,000 – $2,250,000 range searches.

Conclusion.

Close to a 200 month of supply inventory.

Keep in mind… that doesn’t include all the new construction condos being built and not advertised on the MLS nor the plethora of homes that are still under construction all over the city.

Sure hope this comment goes through as most seem to be lost in the ether.

nope…didn’t post.

anyhow…close to 200 MOS over $1,000,000 in LA county currently.

Watch out for apartment buildings selling for millions and each and every unit listed individually at the full sale price.

The devil’s in the details.

SB/Riv has barely begun to slide even though it’s already this far:

http://housing-kaboom.blogspot.com/2009/01/sycamore-creek-65-sqft.html

$65/sq.ft. … and as all those option-ARM’s go into foreclosure it’s gonna go WAY down past THAT-

I predict $40/ sq.ft. on lovely IE houses like this by 12/2009. Any takers???

And while it seems kind of unfair to be able to feast so generously at the carcasses of such human tragedy hey vigilance and personal responsibility should have SOME tangible rewards-

SPEAKING OF TEMECULA, I JUST BOUGHT A FORECLOSURE 50% OFF.

How much more can I lose, are housing gonna be $75,000, I don’t think so. My mortgage on a DREAM HOUSE is $1,300.

Glad I waited, I’ll gladly pay $1,300 a month to live my dream.. Even if houses drop to zero….

Great post. Dr. Housing Bubble, I live in Venice and the prices are still incredibly expensive – small 2 bedrooms are going for $845K. You mentioned that prices are down to 2003 levels, does that apply to the Venice/Santa Monica west of Lincoln area? Where do you see prices going in this area? Will it be possible within the next two years to buy a home that is not a matchbox is the 500K range?

Most of the cerebrally challenged you are referring to learned this idiotic thought pattern from FOX news, Rush and Shaw.

POLO

You haven’t paid attention. Millions of others who bought before the bubble extracted money via refis and HELOCs. The bubble goes much deeper than you indicate.

Go to RealtyTrac and search Traficula/Murietta foreclosures and preforclosures.

It an eye opener. So, do you think all of those pending foreclosures will drive prices down further or have no effect. I’ve been in this area a long time and 50% off may be an enticing number but is totally misleading. This is an area that is far away from good jobs and was a major target for the “investors” who would come in and buy 5,10, 20 houses in a tract in hopes of becoming the next Trump. A 2200 sq’ tract house sold for $160k the first few years into the bubble and was considered too high to locals. It has to go below that to get to historical norm. The average wages in this area are low.

Doc.

I’am gonna break this down to who’s culpable so that people don’t get the wrong impression and therefore come up with the wrong solution.

First, follow the money. Who prints the money? The Federal reserve. This is the first place to start. The Fed lowered interest rates and reserve requirements to “goose” the economy through a recession that should have taken place in 2000 and through the terrorists attacks of 911.

This forced the “savers” the other end of this transaction of securitized mortgages to take undo risks in a bid to outrun inflation. The banks flush with lowered reserve requirements, loaded up their balance sheets with any paper under the sun to the tune or 60 times their cash reserves (Bear Stearns). The government in its usual inefficiency missed the whole deal because after all they’re functioning at “DMV level” throughout the entire beaurocracy.

Testimont to mans ability to create, the bankers put the savers and the borrowers together in ever increasing complex relationships add in ratings agencies who were anything but “consumer report” types and were basically cheerleading with ratings that made CCC the new AAA. And an ENTIRE society that was willing to play ball, and you have the current mess.

I want to focus on the forest though and stop hacking at the trees. We are a spoiled, pampered, foolish and nonsensicle people right now. We need to get back to REALITY!!!! Life is HARD! Ask the other 4.5 billion people how hard it is and it would BLAST your soul! We aren’t in just a credit bubble, we’re in a REALITY BUBBLE!! Five dollar lattes! government retirement for life at age 50! Firemen making 175000 a year!! Hedge Fund managers making HUNDREDS of billions of dollars for shuffling papers and punching buttons on computers!! Everyone with a DISABILITY!! Are you kidding me? This economy is an Fing JOKE!!

It’s rotten. It’s been rotten and its because WE”RE ROTTEN! So, don’t bend to the facile argument that its this….or its that…..PARTICULAR person. Its most if not ALL of us and whoever suffers the most from this cycle will have benefited the most prior to this event.

So, if you find life is getting hard, look back on allllllll the years you benefited from a temporary insanity that wracked the nation and try to figure out YOUR part in it and how you can educate your fellow citizen by example of how to live a productive and virtuous life.

Alan Davis-

You’re totally right. Check out the upcoming data for Orange County! http://img172.imageshack.us/img172/9496/26984246wx9.png

A minimum of 50% total decline in all areas is in the bag. The real question is how much will we overshoot the norm? And how long will it take?

That’s a scary chart!!

I think the 20k foreclosure wil produce more foreclosures.

Temecula values

1998 value = $130k

2000 value = $160k

2002 value = $250k

2003 value = $350k

2004 value = $450k

2005 value = $550k

A 50% reduction of the 2005 bubble peak value is $225k, which is still $95k above the historical norm.

Figure in the inevitable over-shoot to the down side, and you get lots more pain ahead.

“Housing will not look much better at the end of this year than it does now, but “we do expect ’09 will be the bottom,” the chief economist for the National Association of Home Builders said Tuesday.” -National Association of Builders.

~

HAHAHA! This is from the International Builder Show this past week in Las Vegas. I was at the show last year and the NAHB claimed that there was a less than 50% chance of a recession in 2008 and that the economy would pick up in the second half of the year (this was after the recession had officially begun). Note to self, whatever the NAHB, NAR, etc. says, do the opposite.

Dear Comrades,

Why are the “media expert talking heads” always wrong? Simple. Their job isn’t to inform or even be informed. Their job is to please the advertiser, who relies on maintaining the illusion that all is well. The people thus hypnotized are expected to go out and buy things.

It’s all part and parcel of our Potemkin economy. The only trouble is that, first, people have no money and, second, all their credit has been either used up or revoked.

Now we hear about obama mimicking the bush idea of creating a “government bank” to simply “buy” (meaning squander our tax dollars,) at 100 cents on the dollar, all the toxic worthless crap the banks are hiding. They’ll do anything to avoid revealing how bad this is.

Well, do svidaniya!

What are you talking about or referring to?

Anne, I live in the Beach Cities area: Redondo Beach, Hermosa Beach, and Manhattan Beach, and I was wondering the same thing. People are still asking for ridiculous prices for their modest, middle class homes. If I’m going to pay a million dollars for a house…It better look like a million bucks! I am wondering what it is going to take to be able to buy a decent home in this area for 500 K which I still think is a ridiculous amount of money for a house. There are lots of people here, in the Beach Cities, who don’t believe the prices will drop much more. They all believe that most people here make a lot of money, or have a lot of money. I’m not convinced that is the case. I think most of them are way over their heads in debt. I would really like to be right on this. I did move out here from Houston, TX in 2001 so that might be why I am disgusted with the prices here. The housing boom didn’t really seem to effect the Houston area. I still visit the area yearly and have tried to keep up with what is going on there with real estate. It is a different animal real estate wise.

Dear Dr. HB;

By any chance could you direct me to a site that would have this type of info on SLO county, specifically Northern county? The closest I have found is SLOcounty homes.com but it isn’t nearly as informative, truthful nor as in depth as yours. Thanx in advance.

Hey dafox, Alan Davis,

Any idea where to get that default/foreclosure information for other counties? Up here in NorCal some counties (SF, for example) have very few foreclosures, while others are bleeding and down 50+%.

Thanks,

Will

Well, it is November 2009 and yes home prices continue to fall. We too started looking to buy a starter home, but after seeing that a lot of these banks refuse to go lower on their homes for sale and also are refusing to put out all their foreclosures (as to avoid a complete flood of them and thus lower prices) we have stopped looking. These banks are obviously out of tune with reality. These home prices need to come down and reflect our economic situation.

Leave a Reply to PSPS