10 Reasons Why California is Years Away from a Housing Bottom: Rebuttal to Those Calling for a Bottom for California Housing.

Housing in California is years away from a bottom. Let me make that clear and if you have any doubts, after reading this essay you will have a better understanding as to how I arrived at that conclusion. This article is longer since it will try to answer many of the arguments from those calling for a real estate bottom here in California. After looking at multiple sources of information like income, demographics, sales, psychology, and the economy there is no logical evidence for a housing bottom in California. It is well worth the read and certainly provides more information than a 1 minute sound bite. Recently I have noticed a resurgence of bottom talk coming from professionals in the field but also through e-mail questions.

My assessment is this renewed energy has come from two primary culprits. The first is of course the Housing and Economic Recovery Act of 2008 that provides $300 billion in loan refinances and also bails out Fannie Mae and Freddie Mac. In addition, there are many provisions in the bill to juice the market all of which will have very little impact on California. Both Fannie Mae and Freddie Mac announce earnings this week and the news isn’t going to be good. Freddie Mac lost $821 million in the second quarter and announced that they will be slashing their dividend from 25 cents to 5 cents to conserve capital. This wouldn’t be such a big deal except the U.S. taxpayer is now on the hook and a loss for Fannie Mae and Freddie Mac leads us one step closer to a bailout.

The second reason for the upsurge in bottom talk at least for California is the massive price drop we’ve seen this past year. A drop in the median sales price statewide by 38.38% is bound to get the attention of anyone. Yet simply because prices have fallen steeply in one year does not signal that now is a good time to buy. In fact, I will give you 10 solid reasons in this article why we are years away from any bottom in California.

We really are living in a once in a lifetime bubble. It is highly probable that none of us will see a real estate and credit bubble of this size ever again. There will be minor jumps and dips in the future but nothing on this level. I think the best way to conceptualize this extremely large fiasco is to think of someone who is massively in debt. Everyone knows of a friend or family member that spends way beyond his or her means and is usually in major debt. They have nine credit cards, a $700 car payment, a $4,000 mortgage, and yet seem to shuffle debt around like musical chairs. At a certain point, this game ends and some accept the reality and confront the issue head on and others live in denial.

Those that confront the reality sometimes meet with a financial professional or a debt counselor usually with advice to cut up the credit cards and develop a sustainable budget. A prudent plan. If you are serious about correcting negative cash flow situations, you really have to create a budget that takes into account how much money is coming in and going out. In the case of our country, it has gone into debt counseling, was told to cut up the credit cards but is refusing to do so and is actually applying for more credit cards!

What you will not hear from bottom talkers is any mention of incomes from the vast majority of people. Sure they will use random examples of those in Bel Air, Brentwood, Laguna Beach, or Newport Coast but that is a tiny fraction of the population. They cannot use income as a measure of support because it will demolish their bottom theory. Let us now move on to the 10 reasons why California is years away from a housing bottom.

Reason #1 – REO and Foreclosure Phony Numbers

Here are some stunning figures:

Q2 of 2008 Notice of Defaults for California: 121,341

Q2 of 2008 Foreclosures in California: 53,943

Yet when we look at the overall inventory on the market and sales, it looks like overall inventory is decreasing. How can this be? First, there are shady things going on. Can we prove this? Not with a definite yes but using multiple sources of data we can see something is not matching up. It was hard to “prove” massive fraud in the subprime markets as it was going on but we knew it was there.

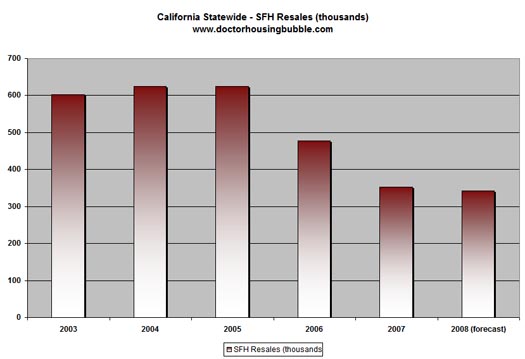

First let, us look at statewide sales for the past few years:

*Source: C.A.R.

This chart is very important because it covers the entire yearly sales for California. Sales have been falling steadily since 2005, long before the mainstream media echoed any sentiment about a bubble in California. So this number is clear. We will use the sales figures for 2007 since those have already been recorded.

Now, let us take a look at the raw sales numbers for Los Angeles County for 2007:

Total Sales for Los Angeles County in 2007: 74,722

Total California Sales in 2007: 352,800

So Los Angeles County made up 21.1 percent of all sales for California in 2007. The point of this is that in a county with 10,000,000 people and 88 cities can be looked at as a microcosm of the entire state with low, middle, and high income neighborhoods. Let us now look at the latest data for Los Angeles County:

Los Angeles County second quarter NODs: 21,632

Los Angeles County second quarter foreclosures: 9,609

Current Inventory August 2008: 51,315

LA Sales in June of 2008: 5,678

Months of Inventory: 9 months

These numbers should be pointing to the fact that we have not reached a bottom. The June data for sales is normally the highest month for sales in California for many counties. So far for the first six months in Los Angeles County we have seen this many sales:

First 6 Months Los Angeles County Sales: 27,268

We are including the highest sales month in this data so we can easily see that we are nowhere close to approaching the 74,722 homes sold in 2007. Keep in mind the fall is a slow selling season and summer is almost over. We can safely assume that sales for Los Angeles County for 2008 will be approximately 50,000 to 56,000 when the year is said and done. Take a look at the NOD and foreclosure numbers for the second quarter. The fact that nearly 8 out of 10 homes that receive a notice of default in California turn into foreclosures should tell you that we are on the verge of seeing an onslaught of inventory hitting the market in the next few months.

If sales are falling and foreclosures are growing, how can months of inventory be declining? First, those that do not need to sell are probably thinking twice about selling their home thus artificially lowering the overall inventory numbers. Second, we have lenders who are overwhelmed and simply choose on purpose or for whatever reason not to add the foreclosure as an REO and sometimes these homes do not appear in the MLS thus keeping certain homes off inventory lists.

You can do the math. This is no bottom. In June only 35,202 homes sold statewide. For the peak month of data, this is a pathetic number.

Reason #2 – The Walkaway Pay Option ARM Test

It seems like the mainstream media is finally catching on that Pay Option ARM mortgages are a disaster waiting to happen. The state of California is waiting to see who will blink first. I’ve been sounding the Pay Option ARM alarm for a very long time because I really do think that this is the next major crisis. To a certain extent, the $300 billion bailout given the current guidelines is something many can swallow bitterly because it would force lenders to writedown mortgages and also the borrower will have to share future appreciation with the government. Not exactly ideal but given our government it is probably the best that we can come up with.

There is literally no way to justify the Pay Option ARM mortgage debacle that we will head into. These loans turned thousands of Californians into futures traders by making their mortgage into an options contract. How so? First, these loans allowed borrowers with a few flavors of payments. You had your 30 year fixed vanilla payment. Your 15 year accelerated payment. Your interest only option. Or the most popular and most widely used, the negative amortization option. Many borrowers elected to make the minimum payment because why make the full payment if you were going to the flip the place in a few years?

These loans also offered longer recast dates masking the problems for years. 5 to 7 year “anniversaries” were common where a loan payment had the potential to double once the recast date hit. The only thing keeping this gig up was massive appreciation. The lenders got to book the deferred interest as income and the borrower kept making the lowest payment. This game was good until prices started to fall. Now, many of these lenders barely recovering from the subprime mess are anxiously waiting to see how borrowers are going to respond to their recast anniversaries. I can assure you that borrowers are going to let that option expire worthless.

This of course is easily explained. Why would a borrower keep making a payment on a $500,000 mortgage when the home is now worth $300,000? If they went zero down, the only incentive for them to keep making their payment is their credit history. In many cases as we are going to find out people flat out lied and never qualified for the loan in the first place. There will be no bailout for these people and this means:

(a) Lenders are going to take some massive losses and will do some serious balance sheet rebalancing.

(b) There is pent up demand alright. Pent up demand to get rid of these toxic mortgages. Many lenders are going to implode under the wait of their horrible mortgage underwriting.

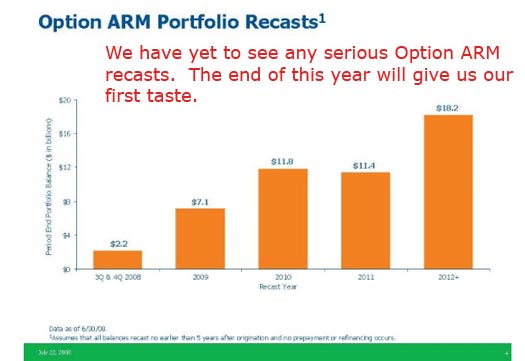

We are going to find out how pervasive and extensive this fraud network is. To paraphrase Warren Buffet, the tide is going out and we are going to see who is swimming naked. Most of these loans fall under the Alt-A category and many lenders are deluded thinking these are much better than subprime loans. They are not. How many of these loans are out in California?

Total Alt-A loans as of June 2008: 688,975

Average Balance as of June 2008: $419,790

Number with a prepayment penalty: 302,909

Number with a second lien at origination: 206,216 (these are most likely worth zero)

Number with interest only payment: 252,329

Number with negative amortization: 198,385

Percent with at least one late payment in last 12 months: 27%

Percent ARM loans: 70%

*Source: New York Fed

Think about those numbers for a second. This one point is enough to quell any bottom talk. Take a look at WaMu’s Option ARM portfolio, half of which is in California and you’ll realize that we haven’t even seen the start of this mess:

What is the actual notational value of the Alt-A junk floating out in the state? How about $289,224,815,250 as of June 2008. Those of you wondering where that $300 billion figure comes from, there you go.

Reason #3 – Free Rent?

It is hard to believe that we are even in this situation but we are going to see unintended consequences galore. First, lenders are going to realize that buyers are not going to stay current on their mortgages because:

(a) The economy

(b) Recast/payment shock

(c) Psychology

And when we say walkaway you need to realize that this is going to take on a new meaning here in California. The foreclosure process here in the state is incredibly slow. It can be anywhere from 250 to 300 days from the first sign of a problem until the sheriff comes to your door. The idea most have of walking away is that someone is going to send their keys to the lender and are going to vacate the home soon after. That is not the case.

Most people are going to walkaway psychologically first, then they’ll give the keys only until the very last moment. Many borrowers already know that the market in California is in the tank. It is not coming back. Many are now realizing that come the anniversary date, they are simply unable to cover the payment. With lenders being inundated with late payments, the process is going to be delayed. If anything, borrowers have a few months maybe even a year of “free rent” as some articles are pointing out.

What will this do to the market? Well, lenders are going to get reamed because of this. First, some of the bottom callers won’t see these numbers reflected as inventory but those that actually look at the data realize this is only pent up supply that will be unleashed in the next 1 to 2 years. These people are on borrowed time and so are the lenders. Instead of speeding up the process, there is even talks about making it longer! In fact, Freddie Mac only a few days ago announced that in 21 states it would extend its foreclosure timeline to 300 days from the first missed payment and 150 days from the initiation of the foreclosure process. Is it any wonder the free rent meme is now spreading?

Reason #4 – The State of California is in Recession

Many of those calling a bottom forget one simple thing. The state of California is in a recession! We are seeing a unique two hit housing collapse here. In the past housing bust here in California, the economy first declined then housing followed. In this bust, we see housing declining first, the economy following, and then housing getting hit a second time. This is the lull I feel we are in. We are simply on a plateau until we start seeing prices start falling again because of the economy. The bottom callers tend to gravitate toward economist and politicians that still technically feel we are not in a recession.

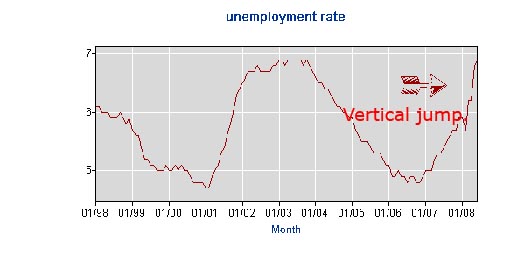

The California Governor came out with a strong hand laying off 10,000+ part time state workers, calling for hiring freezes, spending cuts, and is now in a battle trying to bring 200,000 state employees down to the federal minimum wage because of the budget impasse. Oh yeah, we have a $15 billion budget deficit here in the state and the budget is now weeks over due. Does that really look like a sign of a good economy. Plus, we have one of the highest unemployment rates in the country:

The fact that 10,000+ people were just let go, you can rest assured that the next month of data is going to put us squarely over 7% for the unemployment rate. Somehow those calling a bottom forget that you also need a healthy sustainable economy for people to jump back into the market to purchase homes.

Reason #5 – Federal Reserve and U.S. Treasury Smoke and Mirrors

The Federal Reserve, who in large part was fundamental in creating the easy credit that fueled this entire mess in the first place, doesn’t care about the U.S. Dollar. In fact, the U.S. Treasury doesn’t care about the dollar either. How so? First, they do their charade every so often by beating on their chest that they support a strong dollar yet do actions that actually harm the dollar. For example, recently they have started talking about their “concern” about inflation. There is a simple solution to that. All they need to do is hike the Fed Funds rate. Yet what do they do? Nothing.

The U.S. Treasury instead of punishing the egregious lending that went on for a decade decides to push the largest housing bailout in history on a weekend and extend credit to the two largest mortgage entities to purchase crap mortgages from the tiny mortgage entities! As we saw with Freddie Mac, the U.S. taxpayer is going to take it in the shorts and in the end, it isn’t going to do a damn thing for the overall economy. Freddie Mac is already bleeding red and this program doesn’t go into full effect until October 1, 2008! It will help a few people purchase some nice golden parachutes but the average citizen is going to quickly realize that stimulus gimmicks and bailouts do cost something in the end.

How does this apply to California? This is going to be the ultimate shock. The bailout package won’t do a thing to help that $300 billion Option ARM tsunami just waiting on the balance sheets of many lenders. Some borrowers are going to want to cement that minimum payment as their 30 year fixed payment. Bwahaha! That can’t happen. Try calling your credit card company and telling them, “yeah, I’m only going to give you $20 a month even though I owe $10,000 because that is all I can afford.” Do you really think they are going to say, “okay, we’ll writedown your balance to $5,000 just cause we like you.” Each writedown is a major loss that needs to be reported and we have nearly 700,000 of these loans in the state alone.

Reason #6 – It’s the Income Stupid!

Another major point that tells us we are years from a bottom is incomes still do not reflect the median price of homes in the state. In California the median household income is $53,770 if we look at the three-year average from the latest data at the Census Bureau. The median price for a home statewide is $368,250. That gives us a ratio of 6.8 which is still too high. It makes you shake your head when the peak price in April of 2007 was reached at $597,640 giving us a ratio of 11.11! Freaking unbelievable.

So from a relative perspective, yeah that 6.8 ratio doesn’t seem so bad but anything seems better then the ratio of 11.11. Let us use the hypothetical numbers of this median income family buying the median priced home with a conventional 30 year fixed mortgage:

Median Income: $53,770

Median Price for a California Home (June 2008): $368,250

30 year fixed mortgage with 5% down

Down payment: $18,412

PITI: $2,594

Net Take Home Pay: $3,607 (filing as a married person with 2 exemptions)

At this rate, 71.9% of the household net monthly income is being taken up by the house payment. Even if we use gross monthly income, this person would not qualify for the underwriting in government-backed loans. Now that income does matter and income is a direct reflection of the health of the economy, we are going to enter the next phase of the housing market. The first phase was the bubble bursting creating the economic decline and prices falling, the second phase is going to be the uncovering of the fraud and toxic loans while recasts hit at the most inopportune time.

Reason #7 – Renting is Hot

Renting or leasing a place is going to look a lot more attractive. In fact, in Los Angeles County the majority of people actually rent. Take a look at some of the rental rates for certain counties:

Households that Rent (per county):

San Francisco: 65%

Los Angeles: 52.1%

San Diego: 44.6%

Fresno County: 43.5%

Orange County: 38.6%

Riverside County: 31.1%

As you can see, the amount of homeownership in a county is not indicative of a healthy market. One of the most battered counties Riverside has a high home ownership rate at 68.9%. San Francisco which is one of the last areas to fall and has held up stronger than most California counties only has a 35% homeownership rate.

What this should tell you is that renting in many places has already been a solid alternative. In places like San Francisco and Los Angeles the majority of households do rent. This is because even before the boom these were very high cost areas and after the boom they simply went into wonderland territory thus keeping the renting numbers high or stable.

Many people who would have qualified under the “fog a mirror” guidelines during the past decade will now have a hard time landing a loan. Given the overall median income of the state the buyer pool just shrunk on a massive scale. Another argument I have been seeing looks simply at the supply side assuming everything will once again play out simply because the inventory count is decreasing. So what. Look at the phantom shady REOs and the pent up supply that will hit the market shortly. Take that plus the market demanding more stringent loan requirements and you just took away a large portion of your market. The only way to get the housing market in California roaring again is to bring back the shady mortgage loan network and the complicit Wall Street backers hungry for loans to sell off to unsuspecting foreign buyers. Do all foreigners think all Californians live in Beverly Hills? Apparently, Wall Street wanted them to believe this because stuff rated as AAA in areas with Real Homes of Genius makes no logical sense.

Now renting doesn’t seem like such a bad idea and many of those that will lose their homes will become renters. Many others simply do not want to buy given the current market prices.

Reason #8 – Demographics

California has 36,457,000 people. That is approximately 12% of the U.S. population. The argument is a simple one for many bottom callers because the raw number of people is growing in the state of California. Yet given our overall economics this will not help the housing market. First, much of the demographic growth is not with people who earn high incomes. Most growth is in lower to middle income households. Yes, these households do require housing but they aren’t going to be paying $400,000 for a shack. They are either going to do two things which they already are:

(a) rent or lease a home (see Reason #7)

(b) purchase a lower priced home

There is demand but for Affordable Housing in California and the unseen benefit is that this market correction is starting to do what politicians and builders couldn’t do. That is, create a surge of affordable housing through the real estate crash. You really have to love how the politicians scream and stomp their feet about affordable housing yet when prices start coming down hard they do everything they can to sign in legislation to keep prices unaffordable! This backward logic is the reason our President and Congress have ratings that are tanking faster than housing prices.

The idea that the sheer number of people coming into California is going to keep prices sky high is an absurd argument. If that were the case, China with 1.3 billion people would have $1 million dollar homes in every single corner. In addition, the fact that our budget is so poor we are most likely going to see higher taxes which will impact businesses further and additional state cuts creating more job losses. From most recent reports we have actually seen a net migration of middle income earners from the state.

Reason #9 – The Real Estate Feedback Loop

It wasn’t uncommon to hear during the bubble days of California loan officers making $20,000 to $30,000 a month with a high school diploma. That made the lender happy but also made the state happy when they collected their income. The agents that were selling those median priced $597,640 homes were happy when they got their 6% cut. The appraiser, escrow officers, title companies, and sellers all had smiles on their faces in the mania which was the California housing market. Much of this income was a once in a lifetime opportunity. Wall Street through their sophisticated gambling racket of mortgage backed securities and all the synthetic derivatives based off these loans figured out a way to fool the world into believing the rate of growth in real estate was somehow sustainable.

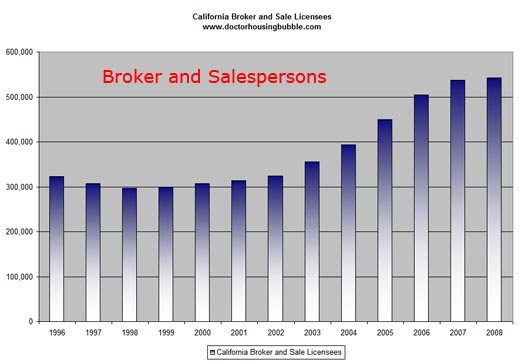

Just to give you an idea of how many people jumped onto this ship, take a look at the number of broker and salespersons licenses given out by the Department of Real Estate here in California:

There are currently 542,267 broker and salespersons licensed in the state. This for a state that saw only 35,202 sales in June of 2008! In June of 1998 there were only 297,359 licenses in the state. So basically the number of people jumping into real estate doubled this decade while the population went up slightly:

1998: 32,987,675

2008: 36,457,000 (an increase of 10.5%)

So our economy suddenly turned into one fueled by real estate. The government was happy because it was collecting beaucoup tax receipts from the decade long spending orgy. Incomes kept going up as the Ponzi housing scheme kept growing. That is the predicament we now find ourselves in. A state so dependent on real estate for everything is now facing a market that is collapsing. We didn’t diversify and we are now paying the price. Jobs connected to real estate that are now going away include:

Construction

Agents

Brokers

Banks

Home Repair

Insurance

Finance

These were good high paying jobs. Not only do these people face the pain of seeing their income fall sharply but they also do not spend hurting our “consumer” economy. These were the people buying luxury cars, clothes, and eating at expensive restaurants. The ripple effects will be felt throughout the country. Those cars made in Detroit will no longer be purchased here in California at the same level because people simply cannot spend money they do not have. The fact that fuel has surged has only accelerated the decline. Fuel is ticking lower slowly and this is good because it will bring attention back to the number one issue, which is the housing and credit crisis.

This is the feedback loop we are now in and will be in for many years. As you can see from the chart above the real estate economy here in California took a decade to build and will not dissolve into the economy over night. Where do the bottom callers think these people will find jobs? The few sectors that do show growth, those of healthcare, leisure and government have their own nuisances:

(a) healthcare – requires advanced training

(b) leisure – much lower paying jobs typically in the service sector

(c) government – Arnold said a hiring freeze so no luck there

I’m not sure we are looking at the same data. Many of those seeing a bottom also thought the subprime mortgage mess would be contained. There is nothing contained about this multi-front onslaught of credit and wealth destruction.

Reason #10 – Consumer Psychology: Why Buy Today when Tomorrow it will be Cheaper

I talked about certain trends that are emerging. The idea of the “all hat and no cattle” mentality is something I talked about at great length in a previous article. To blame only one sector is unfair because this was a collective spending orgy. There was the powerful line that agents used of “national prices have never fallen” that is, until they did fall. This was the first time that we have ever seen a national median decline in price since the Great Depression. In fact, this decline in sharpness and strength is actually hitting at a quicker speed then that of the Great Depression. So that mantra is no longer true.

In states like California, how do you explain a median price drop of 38% in one year? I love the new argument that goes like this, “well the few sales that are occurring are distressed properties and don’t accurately reflect the overall market.” Newsflash. The entire state is distressed. Unless you are selling prime property in the Hollywood Hills get accustomed to distressed sales. The number one issue on the minds of Americans is the economy. The vast majority don’t feel like buying homes when the economy is in the gutter.

Also, let us assume this is the bottom. What in the world will cause prices to jump up in the next year? If anything you can rest assured that prices are going to stay the same for a few years. I would argue that prices in California won’t bottom until May of 2011 and those that are betting with their money in the futures market are in the same boat as I am.

After looking at the above reasons, you can rest assured that many of those buyers sitting on the fence are aware of some of the 10 reasons. One reason may be enough to keep them from buying. 10 reasons are enough to keep you from jumping into a bubble that still has plenty of air to release.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Subscribe to feed

Subscribe to feed

37 Responses to “10 Reasons Why California is Years Away from a Housing Bottom: Rebuttal to Those Calling for a Bottom for California Housing.”

A friend of mine has been looking at houses near Sacramento. There are many foreclosures and short sales to choose from. But the funny thing is that, even after making a full-asking-price offer on a short sale ($350K), the seller/lender is just sitting on the offer. She later found out that the seller/lender has gotten offers over the asking price, yet they won’t let the property go. What’s with that? What are they waiting for, the market to miraculously rebound so they can take an offer of $700K? Don’t they have to pay the real estate agent their commission on a bona fide full-asking-price offer even if they don’t sell?

You’re a genius. I like the way you break down your argument so that the common folks can understand your way of thinking. It was a great read. Thanks!

Thanks for the post Doc. You are still leaving out an important factor… the price of everything we use is headed up dramatically. From tires to eggs, just about everything we touch is related to energy. Cride prices appear to have recently moderated but we are in compitition with 2 billion in the third-world that, thanks to “Free Trade”, are fighting for their piece of the pie.

The truth can be so disconcerting. Quick, turn on CNBC for the daily dose of “this is the bottom.” Or, how about one of those crap-ass “financial” shows on the Fox weekend lineup. Surely if we can just force blue collar wages a little lower while cutting taxes at the top we’ll soon have a healthy economy. And oh by the way, reason #9 isn’t the true story of the economic death-spiral we are locked into. Nope, uh-uh, this is the bottom. We’re sure of it this time. And don’t trouble yourself over the fact that we have apparently only been over 800 on the S&P while supported by planet-sized bubbles, we’ll surely be making new highs any day now. Happy days are here again.

The State of CA, Counties and Municipalities all have a check book and it is call the CAFR. This stands for Comprehensive Annual Financial Report. All of these entities must report their net worth annually. The Governor of CA, with his budget shortfall needs to look at the State’s check book to see how weathy, instead of how poor they are. This is true for all 50 states. My Municipality, being Woodbury, MN has a 2006 net worth of $500 million for a city of 50,000 citizens. Our County being Washington County, MN has a net worth of $250 million. That is not chump change.

SORRY ABOUT NOT THINKING THAT 700,000 THAT WENT TO 350,000 ASKING BUT NOT WORTH 125,000 OF MY CASH WHICH NEEDS TO BREAK EVEN IN PURCHACE POWER AFTER 20 YEARS OF SUB PAR BELOW INFLATION RATE OF RETURN in relation to everything including avacados that should have breen planted from seed all over that state to bring back the 10 for a buck price and cut the more than a dollar for one todays price………….inflation rate not accounted for…………….

Another bulletpoint to add to #2 is that it now appears that the 2007 vintage loans are doing the moonwalk away from properties: http://calculatedrisk.blogspot.com/2008/08/freddie-alt-and-default-by-year.html

The current theory is those who bought in 2007 are already underwater, and so are walking away. But those in 2006 arent AS deep under (or arent at all in few select places), and are holding on. As they get deeper and deeper, it may cause 06ers to start mass migrating away from their mortgages. So you have the ‘front’ of the line walking away due to negative equity, and the ‘back’ of the line being shoved out due to recasts. This is a double whammy that not many people had thought of!

This could actually be good news for those of us wanting to buy (and waiting for affordability) – it means this mess could be over sooner than DrHB (and others) had thought. It wouldnt change the price at the bottom, merely help maintain the acceleration to the bottom.

To Cowboy Bill: Woodbury’s net worth is 500 million for 50,000 citizens? That’s 10 grand per person, or 40 grand for a family of four… And the county as a whole has only half of that? That IS chump change, my friend. That means that all your 400k and 500k houses have less than 10 percent equity, implying that the average Woodburian is mortgaged to the eyeballs, or has a negative net worth.

Also, those numbers are at least three years out of date, collected at the top of the housing market. The county net worth is much less now…

My sister works in a Woodbury law office specializing in foreclosures… that must be why she’s been up to her eyeballs in work for the past few years.

Just look at RealtyTrac and you can see that banks are sitting on tons of REOs they refuse to put on the market. They are carefully adding just a few attractively priced homes on the market at a time so that the too eager fence sitters bid them up.

I can’t wait till these knife catchers get spent out so sensible, price to earnings housing prices can return. Until then keep ventilating those hands you eager beavers!

Must reading. Unfortunately it will not be understood by REALTARDS or politicians who seem content to watch Rome burn.

After marinating in the reality blogs (Dr.Housing/Mish/Calculated Risk, et al) for some time, I am struck by the lack of real solutions being presented. Sure some want abolishment of the Fed (not going to happen) or destruction of FNMA/FHLMC (also not going to happen) but what then are 10 realistic steps away from the abyss? To be sure, I don’t have the answers. Curious to see what you suggest.

My .02

There seem to be some inaccuracies in #2.

1) I don’t think the future appreciation is shared between the home borrow (“owner”) the government, I think it’s shared between borrow and bank.

2) Pay option ARMs don’t typically allow the loan balance to double. My understanding is that they may allow the loan balance to grow by 10% or so before triggering fully amortized payment. (Thus, the 5-7 year period is probably longer than the effective period until “recast” for someone paying the minimum from month 1 forward.) See #9 & #10 at: http://www.bankrate.com/brm/news/mortgages/20070529_ARM_rate_reset_glossary_a2.asp

Outstanding summary — a great refutation for all the bottom callers. One technical correction: people in California have not bought cars made in Detroit in a long time (besides jacked up monster trucks in the 909).

Cowboy Bill:

it looks like I will be moving the family to Woodbury, MN.

Wow! Wow! Wow!

I found your blog through Peter Viles’ blog, which is on the Los Angeles Times’ website. Thanks Peter for the link, and thanks Dr. Bubble for this article. You’ve taken all the bits and pieces that I’ve read about from different sources, and put them all together into one, well thought out piece.

I live in Los Angeles, and watched dumbfounded, as year-after-year housing prices increased by double digits. I kept wondering: How can people afford to buy such expensive houses? The answer is now evident that they couldn’t.

This article gives me considerable hope that in a year, or two, or three, my wife and I may be able to buy a home of our own. We’ll just sit tight, and wait for the right time to make our move.

Many thanks.

tew-

I caught that “…were common where a loan had the potential to double once the recast date hit” part as well. I think there’s a bit of a typo there – I believe he meant to say “were common where a loan PAYMENT had the potential to double once the recast date hit.”

The payment of the loan doubling (or near it) is quite common if you look at the min pay vs the ~25yr @ 110% fully amortized payment.

I am not impressed with your financial evaluatons based on what the local tax assessors say. This is a tactic used to make more income for the local government and has no basis in reality. I know of people, personally know them, who have had their property asessments raised arbitrarily soley for the benefit of more money for the tax fund. It is not necessarily grounded in reality. Those boys on the country work crews, you know, where one guy works and seveen guys watch, need to keep eating you know. Gotta recycle those groceries! Most governments are broke or will be soon enough. But they will fight like hell to get you to pay more taxes so they can continue on with their bullshit. You better wake up and smell the coffee!

Michael

mboone@rtccom.net

I have a comment on the discrepancy between the numbers of REOs and listed properties.

There are a number of empty properties in my area. The ones out in the more rural areas are boarded up, but the ones within neighborhoods are denoted by highly recognizable landscaping.

Most of these are not showing in the real estate sections nor do they have sales placards.

I think the reason is simple.

The banks do not want to flood the market with distressed properties. They are already sitting on a stinking pile of manure, and letting people see how much inventory is really out there will drive the prices even lower. I think people who are on the fence financially will have more reason to walk away if they see the flood of properties.

I’m around many people everyday. I hear people talk about holding on long enough so that they can break even when they sell. They’re hoping for enough of a recovery just to get out. These people are listening to the government boosters on the TV, radio, and paper. They really don’t understand what is going on.

I think (if I am incorrect, please let me know) that as banks sell properties at a loss, it also affects their bottom line. That’s public record. If people really got wind of how very insolvent their banking institution is, there’d probably be a run ala IndyMac.

tew —

actually, the Dr. is completely correct in that “The U.S. Government” will share equity in these refied homes as part of the new bailout. In fact, if there is any equity in any one of these homes upon a sale – after the bailout refi, the Govt equity schedule is as follows:

1st yr: Govt takes 100% of equity

2nd yr: 90%

3rd yr: 80%

4th yr: 70%

5th yr: 60%

anytime after the 5th year, Gov’t gets 50% of the equity – even 20-30 yrs later!!!

It’s written right there in black and white in the 679 page bill!!!

what the talking heads seem unwilling to admit is something I’ve mentioned here before. There is a somewhat defined point when sales should pick up en masse but we are just not there yet. Please correct me if I’m wrong, but I would have to expect that when either (A) home prices AND interest rates/credit requirements allow a home to be affordable or (B) the carrying cost of a house is exceeded by the rent income available from the property that we would see an upswing in sales. And even then, it won’t necessarily mark a turning point for prices. They may stay flat or continue to slide, depending on just what happens with availability of credit and the number of REO’s flooding the market.

@Michael – note that in California, property tax assessments are capped by something called Prop 13, passed over 30 years ago. Other states have the ability to re-assess at will, but in CA, where DHB resides, government cannot.

A few weeks back over at Minyanville, Prof. Depew noted that “math is not a rumor”. Hard to fathom that so many people ignored the math – but there it is. We live in a country where ‘egghead’ is a derogatory term, where people who play sports are lionized and financially rewarded while the scientific method is twisted into ‘intelligent design’, and where kids who admit to liking math in school are social outcasts. No wonder math is a rumor, and so many have fallen into financial ruin.

I think you’ve got it right on #10 — people really need to realize that they don’t have to buy at the absolute bottom to get a good deal. There’s an old story in the stock market that when your barber tells you it’s time to buy, you should immediately sell that stock.

So what if you buy now and the price goes 5% lower? The price on my house has already gone 35% lower than it was two years ago — another 5% isn’t a huge deal. And the person who bought it will come out of it in a year or two with a great buy, and in five years will have a nice little pot of equity.

@Dick,

Cool, you’re willing to guarantee only another 5% drop to your buyer? What a great selling point!

There might be some pot involved, but I’m not so sure that it’s equity you’re really talking about. In the event you haven’t read them, go back to some previous posts by DHB, and look at the charts. It’s no 35% below 2 years ago – it’s from just a year ago. And in some areas, the math indicates another 15% to 35% to go.

If you’re going to sell your book, why not buy some space on DHB’s website and do it the honorable way?

” another 5% isn’t a huge deal. And the person who bought it will come out of it in a year or two with a great buy, and in five years will have a nice little pot of equity.”

Really? Your assumptions are rosy indeed. What if prices drop another 10 – 15%? What if prices then stay flat or just track inflation for 5 years or so?

Look at the timeline of the early 90’s bust. A co-worker of mine bought in a nice L.A. ‘hood at the peak of that bubble. It took 10 years for their house to be worth what they paid for it. Could it play out differently this time? Sure.

But my guess is that after 5 years there will be *something* in that pot, but it’s not equity.

I may be an idiot, but I sure ain’t gonna buy no book for $29.96 that isn’t even published yet, will never have pages, and whose seller and author can’t even put their address or name on their advertisement. You must think we all fell off that there turnip truck, Dick.

This is real time input for those of you who are not aware of the liabilities you have when you walk away from your homes.I am having to learn about the current value of all my assets because of the foreclosure on the Marshall CA home and the forced bankruptcy when the lien holders and the IRS come after the forgiven and unpaid debt. It is interesting that you have to pay 50% tax on the forgiven debt you didn’t pay and on money you never had in your hands, as well as be forced to sell all your assets to pay back the debt. All you can keep is $75k in your home equity or $22k if you don’t own a home or have equity.If you don’t have equity and sell your home for less then you owe, the irs tax’s you up to 50% on the forgiven debt.

So leaving all that wonderful news behind, I am forced to determine what my properties are worth and if they can be sold. The research indicates that housing values in Sonoma County have gone down 20% in the last 12 months. That is really bad and makes all my property up side down relative to the mortgages I have on them. The news gets much worse when you find out that the average actual selling price of homes for the last 12 months has gone down 40%. So the reality of the situation is that the stated 20% devaluation is far to conservative and is probably 40% plus, if you can sell your home. It is very unlikely that you could sell your home if a mortgage is required to buy it. Here is a wonderful quote from the article I added in below.

“The story for the US housing market is little better. The index has already fallen 23% from its peak in 2006. A reversion to the long term mean implies a further 38% fall in the average house price in America; while reversion to the pre-Bubble mean implies a further 41% fall.

”

Regarding the historical ratio of median income to house selling price which historically has been 3.2 to 1,, we can see what we are facing. Currently it is median income $53.7k and median house $369k. This explains what I have been saying all along and why we are headed for untold disaster in the future.Using the 3.2 to 1 ratio would make the median home $172,064. This means that current median housing values have to go down another 53% before people can afford to buy them and can qualify for a loan.

I am not sure about what we all should be doing to try to survive what is happening, but everyone should understand that it will be hard to buy the basic necessities of life in the near future because of inflation, devaluation of the US currency and our personal assets, and lack of credit of all kinds.

Bob

ps I am buying food,gold,guns and ammo,planting a big garden,raising animals to eat, and collecting things to barter with. I am also trying to figure out if I can keep any of my worthless property so I have a place to do all of this on. Worthless property my be a blessing in my case because no one wants it or can force the sale of it as long as I make the payments.

Great article! For someone who has been befuddled by the housing bubble, and have been following the market with ever increasing intensity, I came pretty much to the same conclusions, just lack the skills to put them into words so eloquently. Finally I can just point people to this site, when they try telling how the housing prices will be merrily bouncing back to former levels soon.

People still haven’t gotten the bubble mentality out their heads.

The WSJ reports today that “Five of the nation’s largest credit unions are reporting big paper losses on mortgage-related securities, a sign that housing-market distress is spreading even to the most risk-averse financial sectors.”

Losses are so big they threated to wipe out all equity value for these credit unions. On top of that Fannie and Freddie are scaling back on participation in mortgage markets.

Real estate will not come close to recovery until credit recovers. We are very much on a tightening credit cycle, so to expect prices to recover is unrealistic.

You forgot a 3rd option under #8 – you can rent, buy a lower price home, or don’t forget – you can leave California and go to a better economy with normal priced homes.

We just moved to the southeast and bought a fantastic home for $200,000. Starter homes with a yard & 3 BR are around $50-70,000. The young adults in CA do not have the big down payments that will be required and they no longer have Mom & Dad’s equity to pull from, so I think you will see the 20-somethings taking off for better places to raise their children.

YOU SHOULD CHALLENGE THESE PEOPLE who are calling for a bottom to a public debate on national T.V.

When people are buying foreclosures, they are having their property taxes set at what the county believes is market (which is often double purchase price), not 1% of purchase price. Never saw that before, but now see it on foreclosure purchase docs. The government in this way is living in the illusion that prices will rebound, and that peple will not protest this scam.

Reason 8 Demographics, CA is going way more Latino, 50% drop out rate, 100% high means tested subsidy rates.

We also have the Baby Boomer home owner geezer die off sell off-with accelerating home sales for the next 20 years.

Ain’t nobody going to move into grandma’s gang infested Latino neighborhoods, the people that hold up property values will move to other states & new gated communities,existing home prices will drop a lot further.

Awesome summary Doc! I have become a real-estate-trend-junkie over the past 5 years and have not seen such an intelligent and comprehensive post or predictive mortem of the CA Re market anywhere… And, agree with Adam that you should be featured on a Network debate! I moved to CA about 6 years ago… own a small business… earn $230k gross ave per year… am single… have adequate savings and zero debt. Though I was tempted by exotic mortgage products, I observed the absurd increase in prices/home “values” vs basic fundamentals, and felt intuitively that something was going “way wrong”… So I chose to rent (a lovely home – for a fraction of what it would cost me to buy) in expectation of a seismic correction. Thank God for intuition… But, I admit it still feels a bit embarassing to be a professionally successful and responsible RENTER (5 letter word). I continue to hope that your judgements and predictions — which I also believe in — will prove my instincts and conservative approach to be right on this. I do believe in the American dream. And, am anxious to take my stake in a state I love. At a judicious time. Let’s hope that 2011+ predictions pan out… I sense, as you do, that they will. Here’s to a return to fundamentals — And a smart future for all of us… however painful for some.

Are you kidding me…why would anyone leave california. Thank you for the well written column. Great points. Only….Smitty seems to be dealing with other issues. What neighborhoods are you talking about Smitty. Sounds like you are not doing very well. By the way…..my neighbors to the left are Latinos who bring in over $200K/year. SMITTY…show a little class!

Dr. thanks for the ten reasons as to why California is far from hitting the bottom. You managed to very persuasive arguments to the discussion with great backing facts. I agree with you that our economy as a whole is far from a housing bottom because today prices are slowing increasing and we are beginning to climb back up. Many might think otherwise but we are in no slump. There are many external factors that will not allow for us to hit a housing bottom. Even today such as the new development of L.A. Live this will demand an increase in sales prices for condos, apartments in the downtown area because entertainment is where people want to be. The metro areas are helping out our economy. Even with the real estate prices at 10% less than they were last year, many of the metro areas in the nation are still experiencing price increases. This is largely due to first time home buyers who can still afford to purchase properties and retiring homeowners who are selling their homes and then either moving into a retirement community or purchasing smaller properties. Another important factor is buyers are at a great position to purchase real estate and people do not want to drift away from that. The credit crisis is already is easing. Yes, your credit has to be good to get a good loan from a lender, but loans are available. And the loans are cheaper. As you mention, home prices continue their decline but that will only fuel a turnaround once the market picks back up. Lower prices and lower interest is where it is at now ask yourself what more can a homebuyer want?

Whats up with the real estate agents now a days – you make an offer on a forceclose property and they say that someone else is making a higher offer or that they tell you that people are typically offering $10k to $30k over asking !….huhhh !!!???? i think thats a bunch of bs !! Are they trying to low ball ?Who would ever believe that when everyone knows that the house you’re trying to buy now will surely still go down at least for another year. Isnt it in their best interest to sell it now as oppose to selling it later when it becomes a lot less, whats up with that ???? very puzzling….dont make sense

==> My Municipality, being Woodbury, MN has a 2006 net worth of $500 million for a city of 50,000 citizens

Yeeeaaaaahhhhh …. mmmm kaaayyy. That’s like those homes that *were* worth $800,000 are now selling for $300,000. Like the DJIA that was trading at 14,000 is now trading at 8,000. Like the billion dollar hedge funds that are now worth *less* than zero.

==> That is not chump change.

You keep right on believing that.

Sgt.Sausage, show me any houses in the USA that were selling for 800,000 and are now selling for 300,000. I’m all in no matter where that is, where do I sign?…..All I know about CA is never give up on this state, it will always come back in some way you’d never think of….

Leave a Reply to dangermike