Tell me the Sales Data: You Can’t Handle the Sales Data!

2006 will be known as the year real estate hit the breaks. Many people for one reason or another seem to be astonished that this shift has occurred. But let us look at the data released by DataQuick for September 2006 to see what really is going on:

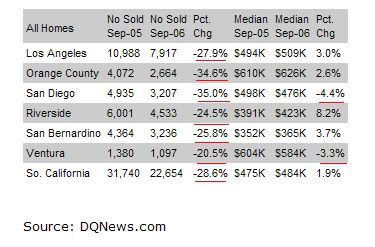

I’ve underlined the key points that are causing the market to trend lower. On average, sales are off on average by 28.6 percent. In some areas like Orange County we are off 35 percent year over year! That is correct, sales have dropped by an astounding 35 percent and apparently no one seems to care. Add the increase in inventory and many folks pulling off their houses thinking that in spring 2007 things will be better. Guess how may folks are thinking like this? And what do you think will happen when massive inventory hits the market, less buyers appear, and appreciation is now negative?

Now you may ask, why do I have any credibility talking about real estate? Great question. During my undergraduate years, I actually worked two years for a local broker and still have an active real estate license in the state of California. I am no longer in the industry but still have a strong interest in real estate like many of you do. Yes, maybe I’m a wolf in sheep’s clothing but the reality is I transitioned into a very different industry and have a graduate degree. During the time, let us say it was part of the boom years, I was making a decent income for an undergraduate. The licensing test was absolutely the easiest thing I had ever taken – essentially, I bought a Tom Vu self study course and taught myself real estate. The music reminded me of those 80s movies with synthesized music playing in the background. Real estate was fun and there is definitely a lot of potential in the field. And it is very hard to be a good real estate agent so let me tip my hat to those out there. And this will only become harder as there are +510,000 agents in California alone (and still growing by the way).

http://www.dre.ca.gov/stats05_06.htm

But coming back to why the data is so important in what DataQuick has produced. Information now travels much more quickly. Even a few years ago when I was in the industry we did not have places like Zillow or Ziprealty accessible to us. The advantage as a realtor was that we had a stronghold on the MLS and we had previous sales data. Even though previous records are public, how many people are going to go down to their local Registrar to do research? Not many unless you are a serious real estate investor. But with these new tools, you can see that the trend down will accelerate because of ease of information flow. By the way, this is record year over year sales decreases for Southern California. Even the N.A.R. who in the beginning of the year claimed real estate gains of 5 to 10 percent is now recanting; good job considering we are two months from year’s end! I think my 7 year old cousin made that prediction in July so maybe she should get a prize too. You can do your own research digging up their old predictions (thanks to Google cache) but they have pulled or modified their current forecasts.

These numbers are large and in charge like my uncle used to say. They command attention and are a better litmus test of what is to come. If you are looking to buy there is no reason for you to jump in right now. Heck, even rates are holding steady or even going down so don’t let the mantra of “rates will zoom up†scare you. Ultimately housing is about value, equity, security, and location. These things have an economic value and most can understand that the current value is out of whack thus creating a bubble. In a future article I will discuss the massive increase in land value over the last few years as opposed to an increase in housing material costs. A definite marker of housing speculation. Even John Law made out speculating on land in Mississippi until it all went bust. What is your takes on the current market numbers?

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Subscribe to feed

Subscribe to feed

44 Responses to “Tell me the Sales Data: You Can’t Handle the Sales Data!”

up 1.9% in Southern California is hardly a “bubble”.

Larry:

September 2006 So Cal Median: $484,000 = YoY +1.9%

September 2005 So Cal Median: $475,000 = YoY +16.1%

September 2004 So Cal Median: $409,000 = YoY +22.1%

September 2003 So Cal Median: $335,000 = YoY +20.1%

September 2002 So Cal Median: $279,000 = YoY +18.2%

September 2001 So Cal Median: $236,000 = YoY +10.8%

The bubble started long ago. Just because we are seeing the peak does not mean we are not in a bubble. We have had seven years of double digit appreciation for the last six years. In dollar terms houses have literally doubled. Or, an aggregate increase of 105 percent over six years.

I’ll let you or other readers fill in the following headline:

September 2007 So Cal Median: $????

I have a good feeling that those positive signs on the YoY will no longer be there.

“We have had seven years of double digit appreciation for the last six years.”

Actually it has been for the last seven years only DataQuick does not have public data past 2000.

Great blog! Sept 2007 is anybody’s guess but I’m with you in that there’ll be a negative sign there.

bubble?

Bubble as in:

You mean the dirt can go from $400,000 to $4,000 almost overnight?

Or, that insiders can sell while pumping up the house’s value on TV?

Or, they can issue more shares in my house?

Or, the analysts can keep a buy rating on my house, while confessing in private emails that my neighborhood sucks?

Or, we can be attacked again and they can close the housing market for a week?

Or, they can cook the books on my Schedule E?

Or, maybe they could issue title to my house to 7 people at a time?

How about moving my loan off-shore thus removing it from my personal balance sheet?

A stock is a click of a button or a call and you are out. There is no clicking in RE transactions. However, let’s say the bubble pops next week……my property still exists, the land still has value, my rent still gets paid and my mortgage payment remains the same.

Unlike stocks, whose leadership always changes with every new bull cycle, real estate (housing) can always be cured by time. Think about that.

http://millionairenowbook.blogspot.com/2006/09/what-does-it-look-like.html

plug in a negative sign, no problem. Does that translate into a financial bubble or something else?

Larry Nusbaum–

Throw your “my property still exists, the land still has value, my rent still gets paid and my mortgage payment remains the same” argument in the same bag as “there’s a shortage in housing” and “land is scarce, so you better buy now before it’s too late”.

* “my property still exists” – Look how many people bought with 100% financing in the last few years. Yes your property might still exist, but if people owe more than what their property is worth, they tend to walk away.

* “the land still has value” – sure, but the same value that it was purchased for? Especially given the popularity of 100% financing? I think not.

* “my rent still gets paid” – I assume you’re referring to an investment property. Unless you bought more than a few years ago or threw a huge downpayment towards your purchase, rents in socal are nowhere near enough to cover carrying costs of property purchased in the past few years. People can either choose to bleed for years or cut their losses, and frankly I’m seeing a lot of option #2.

* “my mortgage payment stays the same” – what year are you living in? Have you ever heard of an ARM or option ARM? Yes, those hugely popular (30-40% of new mortgages in most areas of CA) fun loans that adjust after a certain period of time. Yes, those loans (option ARMs) that were/are so popular and add onto your principal balance when you make the minimum payment like the majority of people. Surprise, surprise, you’ll see a lot of adjustments, especially come 2007. Let’s see how someone refinances into a fixed rate loan they can afford when they owe 100% and they are used to making the minimum payment on their option ARM.

“real estate can always be cured by time” – Hmm let’s see, how long did Japan’s overinflated housing market take to recover? around 15 years? Do you really think that people will be able to hold out that long when they are barely making payments on their adjustable rate mortgages and their houses are either stagnant or declining in value?

We are in the year 2006, not 1999!

The California job market continued to expand slightly faster than the national rate, with year-over-year employment growth of 1.5 percent in second quarter 2006. Growth was widespread, with every sector except manufacturing and information adding jobs in the quarter. (source: FDIC)

Anonymouse: comparing the U.S. to Japan is idiotic and empty.

“Look how many people bought with 100% financing in the last few years.”

How many, Einstein? Give some numbers and tell me what the consequences are………..

(I’ll post as Blue Boy, because I’ll be the one holding my breath)

Larry Nusbaum–

Comparing the market to Japan’s is not idiotic–Japan’s housing market experienced a massive bubble followed by a massive depreciation. Here’s a quote from Mish’s blog that sums it up nicely:

“OK, so “The US is not Japan”. I have heard all the arguments a dozen times. Yes the demographics in Japan were and still are horrid. But US consumer debt is far worse. Also there was very little land in Japan on which to build but there is plenty of land in the US relatively. Japan did not have Global wage arbitrage to worry about (during the crash) and Japan also had an internet boom to look forward to during the decline. All things considered, things look bleaker here than Japan. In the meantime, he who procrastinates longest wins.”

http://globaleconomicanalysis.blogspot.com/2006/08/procrastination.html

It doesn’t take an Einstein to realize the prevalence of 100% financing. It doesn’t sound like you have much direct contact with the Real Estate industry. If you want to see some numbers here’s a quote from business week:

” Most of the pain will be born by ordinary people. And it’s already happening. More than a fifth of option ARM loans in 2004 and 2005 are upside down — meaning borrowers’ homes are worth less than their debt. If home prices fall 10%, that number would double. “The number of houses for sale is tripling in some markets, so people are not going to get out of their debt,” says the Ford Foundation’s McCarthy. “A lot are going to walk.””

You can have fun reading the rest of the business week cover story here:

http://www.businessweek.com/magazine/content/06_37/b4000001.htm

How about a map for your pleasure as well:

http://www.businessweek.com/common_ssi/map_of_misery.htm

Enjoy the read Einstein. Before you make your broad comments, I’d suggest doing some more research.

Must be having tea with David Lereah.

larry nusbaum said:

“A stock is a click of a button or a call and you are out. There is no clicking in RE transactions. “

Very true. However, most real estate investors are going to face a terrible lesson in how ILLIQUID real estate can be..

larry nusbaum said:

“A stock is a click of a button or a call and you are out. There is no clicking in RE transactions. “

Absolutely and this is another thing that in a market favoring buyers, real estate can be a dangerous deal if you are not planning on staying put for 5+ years. Think of it this way. You buy Wal-Mart stock and realized it was an absolute bonehead decision. The stock is now 10 percent below where you bought it. Assuming there is some market which there normally is for stocks, on major exchanges you will sell it that day. But in a down market for real estate you may have to wait (possibly months) and your options are limited to the following:

1. Sell at whatever is offered to you.

2. Lower the price to create a market

3. Hold out for a certain buyer

And since most real estate is never all at once in circulation unlike stock with countless numbers and all being equal (one share of Wal-Mart in L.A. is the same as a share in Sri Lanka), the market is rather limited for real estate. If sentiment is that real estate produces 0 percent year over year gains and is vastly overpriced what do you think buyers will do? In addition, what if many sellers realize they missed the peak, which they have, and all get that same feeling as that person that bought Wal-Mart stock and puts their piece of property on the market? Now you have two DIVERGING forces. Less buyers and more inventory. Even in basic economic terms this will create a pressure on supply and push prices downward.

However with exotic financing, speculation, overpriced areas, and many people realizing they will wait out the market this supply demand curve can change extremely fast as we are seeing in San Diego, Florida, and the Phoneix areas.

Keep in mind that all the supposed experts from the N.A.R. and the C.A.R. all predicted modest double digit gains this year. Still believe the experts?

1. I don’t have a clue as to what was said by CAR or by NAR and when. I know what I have said and done for 20 years in my two markets: SF and Phoenix

2. Your very last post is nice theory, but not how individuals actually perform/act in the stock market when a “mistake” is made. All people need to do is compare real life experiences (and not the predictions of what might be) in the stock market and in the real estate market over the course of their lifetime and they will find the truth about the “bubble”.

3. “However, most real estate investors are going to face a terrible lesson in how ILLIQUID real estate can be.. “

It’s always been illiquid and that’s been one of the saving graces of property. But, when you say “most”, you lose all credibility. Because, according AARP & PMI, most people have 30 year loans and most people have about 50% in equity.

4. http://millionairenowbook.blogspot.com/2006/09/call-to-arms.html – this shows that it’s really concentrated in California, which is still pretty healthy:http://millionairenowbook.blogspot.com/2006/10/california-august-home-sales.html &

http://millionairenowbook.blogspot.com/2006/10/housing-how-california-goes-so-goes.html

Also:

http://millionairenowbook.blogspot.com/2006/09/housing-slowdown-worse-in-midwest-than.html

Larry said:

“1. I don’t have a clue as to what was said by CAR or by NAR and when. I know what I have said and done for 20 years in my two markets: SF and Phoenix

2. Your very last post is nice theory, but not how individuals actually perform/act in the stock market when a “mistake” is made. All people need to do is compare real life experiences (and not the predictions of what might be) in the stock market and in the real estate market over the course of their lifetime and they will find the truth about the “bubble”.

3. “However, most real estate investors are going to face a terrible lesson in how ILLIQUID real estate can be.. “

It’s always been illiquid and that’s been one of the saving graces of property. But, when you say “most”, you lose all credibility. Because, according AARP & PMI, most people have 30 year loans and most people have about 50% in equity.â€

1. Nice way to avoid addressing the topic. You would think that the National Association of Realtors and the California Association of Realtors may have a little more knowledge about the California market and the overall national market than you Larry wouldn’t you say? You just admit that the only two areas you have an expertise in are San Francisco and Phoenix. And following that real estate is local, you may have no idea how Florida or for the large part how Southern California will react. After all, we are talking about 15 million people in the larger metropolitan L.A. area afterall. Your’s is just a theory as well. And the reason I bring up the N.A.R. and the C.A.R. is that they were predicting year over year gains close to 10 percent in the beginning of the year and have only recently started singing a different song. Could it be that these “experts†are wrong with all theories at hand? And wouldn’t they have something to gain singing the clarion song for real estate? I’ll let those reading this blog answer that on their own.

2. From Wikipedia:

“An economic bubble (sometimes referred to as a “market bubble”, a “financial bubble”, or a “speculative mania”) refers to a market condition in which the prices of commodities or asset classes increase to absurd or unsustainable levels (that no longer reflect utility of usage and purchasing power). It occurs when speculation in the underlying asset causes the price to increase, thus encouraging even more speculation. The bubble is usually followed by a sudden drop in prices, known as a crash or a bubble burst.â€

Hmmmm, sounds an awful lot like real estate wouldn’t you say? Most important thing that bubbles have is a speculation component. And figuring that recent stats from the MBA say that all purchases in 2005 where by “investors†or for second homes, I would venture to guess that it is safe to say that we are in a overpriced real estate market. And like Greenspan said a few years ago, bubbles are only defined after the fact. And your AARP and PMI stats are old and outdated. A recent stat from your area of expertise Larry, San Francisco:

1. The following chart shows the percentage of Bay Area loans that were interest only or Option ARMs (know as negative amortization).1

Year Interest Only Option Arm

2005 42.6% 29.1%

2004 43.7% 9.6%

2003 20.3% 0.8%

2002 12.0% 1.7%

2001 2.9% 1.6%

1 Kathleen Pender, Mortgage options explode, SAN FRANCISCO CHRONICLE, April 13, 2006

And the data is a little more recent than your outdated information but who am I to burst your bubble. Here’s a little more data refuting your everyone has fixed mortgages:

“As of September 2005, Adjustable rate Mortgages (ARMs) accounted for roughly 70% of the prime mortgage products originated and securitized and 80% of the subprime sector.*â€

*2006 Global Structured Finance Outlook: Economic and Sector-by-Sector Analysis, FITICH RATINGS CREDIT POLICY (New York, N.Y), Jan. 17, 2006 at 12.

Wow, seems like we are reading different sources. I ask readers to go to the links and do their own research directly. And by the way, the PMI, the source you quoted believes the following:

“PMI Scores are reflected on a scale of 50 to 1000. A score of 100 means there is a 10% chance prices will decrease in the next two years. A score of 560 (SF) means there is a 56% chance of a decrease in the next two-years. PMI is in the business of protecting its money; it is risk management on the behalf of lending institutions. Flip a coin because it will be anyone’s guess how low prices will go. Here is the data:

Below are the risk scores for the top 50 metropolitan areas, minus New Orleans:

San Diego-Carlsbad-San Marcos, Calif., 599

Nassau-Suffolk, N.Y., 589

Boston-Quincy, Mass., 588

Santa Ana-Anaheim-Irvine, Calif., 588

Sacramento-Arden-Arcade-Roseville, Calif., 585

Riverside-San Bernardino-Ontario, Calif., 583

Oakland-Fremont-Hayward, Calif., 582

Los Angeles-Long Beach-Glendale, Calif., 575

Providence-New Bedford-Fall River, RI-Mass., 568

San Francisco-San Mateo-Redwood City, Calif., 560â€

So basically they are betting that there is over a 50 percent chance the market will go down. And this data was posted in May 2006. The numbers are now higher since summer didn’t seem a big boom.

3. Do not misquote me. When I said “most†it was in this context “And since most real estate is never all at once in circulation…†meaning not all units are on the market at once. This is merely stating the obvious. Do not try to debunk my arguments by using a strawman. Most readers can do their own due diligence and connect the dots…try not to connect the dots with made up arguments and restating my assertions. You have a point Larry and many respect that. I have one to state too but seeing my references and direct links to sources many readers can go and verify for themselves. But throwing out errors of logic and argumentation only make you look like you are grasping at straws.

Read your post again.

You keep saying “real estate”. Do you mean to say housing, because, as I have posted several times on my blog real estate is doing incredible, while the housing sector has cooled and the homebuilders (15% of housing sector) has dropped off dramatically.

Talk about painting with a broad brush……….

The housing bubble theories have been building strength for 5 years now and I have chronicled them back to March of 2000 by the WSJ. Someday they could be right (after the market has doubled and tripled)

But, with all this evidence of looming gloom, never a post suggesting what people are supposed to do once armed with such wonderful data: sell? buy? hold? move to Canada?

Add a “Therefore” to the data and it might make sense.

“You have a point Larry and many respect that.”

Actually, they don’t….at least around the millions of housing bubble blogs, etc. They need this bubble to pop, for some reason.

Yes, I know the Bay Area and I don’t see much sign of stress (as is happening in SD and Orange County) and I see no evidence of it.

You have a very informative blog Larry and I appreciate your perspective and point of view. And I agree, many of the doom and gloom blogs seem to hope that real estate will go down in this Apocalyptic fire burning scenario. I do not agree with that. However, I am a bear as you can tell from my writings and from your website, it appears you are a bull. Again, bulls make money, bears make money, and sheep get slaughtered. This site is merely observations of the market from my area. My stated intention was never to show people how to make money or tell them what to do. They can decide from their own ideals what matches their needs in life. In addition, people are observant and can judge for themselves how their market is responding.

And to be frank, in my profession, my hours and my career supersede real estate in terms of purpose and time invested. Hence my transition out of the field of real estate years ago. And when I say real estate come on Larry, it is semantics for the average person. When you talk to the general Dick and Jane on the street do you think they make the distinction between land, second homes, raw materials, etc? There was an article in the New York Times stating that only 25 percent of buyers in the last two years understand the terms of their mortgage. Think of the implications of that for the next few years and you can quote me on this one, you’ll be hearing many people say “my broker, lender, agent, or whatever other person in the industry didn’t tell me that!†So when I speak of real estate I do mean it in the broadest terms.

But I will give some general advice for 2006/2007 on how to make money, or at least how I made money on the last two years since I have been actively investing:

1. Options and shorting homebuilders (2005/early 2006). This strategy is now done since many homebuilders are down 50 percent year over year. I believe there may be some more downside to builders but the market is already heavily sold off. Short-term, do not plan to short. Could be a good time to go short on the positive side. But next year I see them going down a few more percentage points. This was a great way to leverage my view that housing would go down. Below was a chart that I followed:

http://finance.yahoo.com/q/cq?d=v1&s=bzh+dhi+hov+kbh+len+mdc+mth+nvr+phm+ryl+tol+fre+fnm

2. Healthcare. Excellent field to invest in. Number one field for growth in the U.S. for the next ten years. Look into it…

3. Undervalued property in fly over states. My number one rule is to get cash flow for a property using capitalization rates. What are cap rates? http://en.wikipedia.org/wiki/Capitalization_rate

Rates are low. Properties are still undervalued in many areas aside from coastal areas and secondary markets such as Arizona.

4. ALWAYS diversify. Again, markets go in cycles. Real estate has its cycle, stocks have their cycles, and so do other investment vehicles. Read a book in this area if you have not. A few books I recommend:

A Random Walk Down WallStreet: Burton G. Malkiel

Safely Prosperous or Really Rich: Howard Ruff

Rich Dad Poor Dad: Robert T. Kiyosaki

Sell Now!: The End of the Housing Bubble: John R. Talbott

Multiple Streams of Income: Robert T. Allen

I think it is important that you read all books because in the mix you will find perma-bulls and perma-bears that espouse great theories regarding their areas of expertise. The important part is that you find the right mix on how to invest for yourself. Don’t let someone force your hand in dictating your life.

5. Save more than you spend! How easy is this? But looking at how people are using HELOC and credit cards, they are NOT meeting this number one goal. You can also refer to the negative national savings rate.

Finally as a caveat emptor, this blog isn’t intended as a financial advice column. When I go to blogs, I go for musing regarding local markets and how the “person on the street†is responding to the market. And housing, especially in So Cal is the talk of the town. Everyone is a “housing-addict†and there isn’t a day that goes by when someone tells me:

1. The market is crashing

2. The market is booming

3. Housing is ridiculous here!

But there is a shift now. Last year it was about 70 to 80 percent of people bragging about their $100,000 year over year gain in their house. Now, it is about 60 percent bulls and 30 percent bears. The other 10 percent like a feather in the wind are at the mercy of the market and go wherever it may take them.

I am neither bear nor bull. (The beauty of being a long-term investor and a professional) I honestly don’t care…..

Larry

Two more points:

1. Foreclosure % increases should not be over stated. They are increases coming in a year where prices are flat after 7 straight up years. You don’t have foreclosures in up markets so of course the % increase looks big. It’s not. In fact, as I have posted, the bulk of the foreclosures are taking place in Michigan, Ohio and Indiana etc.

2. My opinion (with nothing to back it up yet) is that sub-prime borrowers, the most at risk, will have an easier time going back to their sub-prime lenders to get new loans than the A lender clients of Wells Fargo & BofA. Why? Because, they will be willing to stretch the rules of underwriting once again to earn their fees. The re-fi boom is on……

Larry,

You can only stretch the underwriting guidelines so much. When a house appraises for the same amount that the borrower owes (or appraises for less in many of these I/O and option ARM cases) the borrower has to come up with the difference.

I’m sure most of these people don’t have tens of thousands sitting around to cover this, as evidenced by the fact that they only make the minimum payment on an Option ARM or interest only.

Regarding subprime–the subprime rates are higher now than when most people got their loans. On top of that, subprime borrowers are much more likely to miss mortgage payments which lowers their credit scores which makes it doubly impossible.

I’d say that subprime borrowers are the ones who are the most screwed.

-blue boy

“I’d say that subprime borrowers are the ones who are the most screwed.”

This is not the voice of experience.

“You can only stretch the underwriting guidelines so much. “

They have and will continue to do so. You post like you have forgotten about the 125% lenders….they are still out there.

It’s always been illiquid and that’s been one of the saving graces of property.

I don’t see how having an illiquid investment (i.e. one that you can not sell, except at a severe loss) can be a saving grace.

[Link]

But, when you say “most”, you lose all credibility. Because, according AARP & PMI, most people have 30 year loans and most people have about 50% in equity.

As a counter argument, I would like to have you investigate the blog posts that have been made by ‘Calculated Risk’:

…

“The final graph shows the percentage of equity in household real estate. Currently households have a record low 54.1% equity in their homes.

That may sound like a high percentage of equity, but according to Robert Broeksmit, Chairman of the Residential Board of Governors, Mortgage Bankers Association (from the Senate hearing on Wednesday):

“More than a third of homeowners, approximately 34 percent, own their homes free and clear.”

This group is probably risk adverse and it’s unlikely they will borrow significantly on their homes to fuel consumption. So the debt burden falls on the other 66%.”

[Link]

“I’d say that subprime borrowers are the ones who are the most screwed.”

This is not the voice of experience.

No. But, this one is:

[Link]

“You can only stretch the underwriting guidelines so much. “

They have and will continue to do so. You post like you have forgotten about the 125% lenders….they are still out there.

This can no longer be the case now, since the Comptroller of the Currency has now changed the loan underwriting rules of the game.

[Link]

Yes, they (the mortgage scam artist companies) are still out there, but they won’t stay in business forever.

Now, as for all this refi activity that is supposed to be going on, I’m willing to bet that business is no longer ‘brisk’ for mortgage brokers and loan officers, in general.

And as a side note, everyday, I see lots and lots of moving trucks on the road when going to and coming from work. This, by itself, tells me that there is something terribly wrong with the real estate market and the local economy.

I hope you have some other line of business, besides real estate..

“I hope you have some other line of business, besides real estate..”

Me? I’m a commercial realtor and in case you haven’t been keeping up (It’s been posted to my blog several times) the commercial market is and continues to be booming. Recall my words: housing in one of several sectors of real estate. Most sectors are doing very well, TY

“This can no longer be the case now, since the Comptroller of the Currency has now changed the loan underwriting rules of the game.”

LMAO! It IS the case….

ORANGE COUNTY APARTMENT MARKET:

O.C.’s largest landlords got average rent hikes of 6.1% in the year ended in the third quarter, RealFacts reports today. The typical rent at a large complex is now $1,494 — up $88 in a year.

The only good news for renters is that’s this past quarter’s rise is the slowest annual rate of rent increases on a percentage point basis since the second qiarter of 2005.

Why can landlords continue to ask for — and get — these kind of rate hikes? Few vacant apartments, a byproduct of a healthy job market and home shoppers remaining skittish.

RealFacts reports that only 3.3% of O.C. apartments at large complexes were empty last quarter. That’s down from 4.6% in the second quarter and 4% a year ago. Industry experts think any vacancy rate under 5% is, theoretically, a “sold out” condition.

Larry said:

“O.C.’s largest landlords got average rent hikes of 6.1% in the year ended in the third quarter, RealFacts reports today. The typical rent at a large complex is now $1,494 — up $88 in a year.â€

Of course rents are going to go up. Orange County has one of the lowest housing affordability in the nation hovering between 10 and 15 percent of local residents. The current median income in the county is $71,062. However, for someone to purchase a home with a 20 percent down payment one would need $125,500 (and yes, we realize no one use 30 year fixed rates so the actual numbers would be higher below). So let us run a quick scenario. Someone purchases a starter home for $626,000 with 20 percent down:

Purchase Price (median OC home): $626,000

Down payment (assume 20 percent): $125,200

We’ll use a 6 percent 5/30 year interest only loan for: $500,500

Interest only monthly payment: $2,502

Monthly Taxes: $521

Monthly payment: $3,023

Keep in mind this is an artificial rate. The standard monthly payment would be $3,521 and this is a basic starter home. In addition we are assuming someone came in with a 20 percent down payment of $125,000.

So renting for $1,494 isn’t such a bad deal especially when you can rent a nice condo for $1,700 a month.

In addition, I think everyone expects rents to go up moderately while prices come down. This is common in a down market since there is a premium on renting. Why buy today if prices are going down 10 percent nominally per year?

Looks like Larry Nusbaum can’t handle the data..

from Retailtrafficmag.com, reports that with cheaper housing and job growth to be found in the rest of the Southwest, Californians are conducting a reverse gold rush to Arizona, Nevada and New Mexico. According to the University of Southern California Office of Demographic Research, 250,000 Californians move out of California each year. That’s what’s behind projections that the population in Arizona will double in the next 25 years, growing from 5.7 million to 10.7 million. In fact, three out of five new residents moving to Las Vegas and Phoenix each year come from California. In addition, many California based companies are moving their operations out of state to Arizona and Nevada because of their proximity to California, allowing these companies to move products quickly to California markets and executives to fly in and out in a day. Reza Etedali, CEO for Irvine based Reza Investment Group, expects this trend to continue for the foreseeable future. “Over the next 10 years, there will be incredible growth in the Southwest,” he predicts, noting that about one-third of his clients are now looking for opportunities outside the state. “The region could go through ups and downs, but long term, it’s poised to grow.”

I’m in San Diego, CA and real estate, especially commercial real estate, is not going up!

And as far as I can tell, it looks like Phoenix is going down, too.

[Link]

Same for Vegas:

[Link]

And Albuquerque, New Mexico seems to have turned down six months ago:

[Link]

http://millionairenowbook.blogspot.com/2006/10/phoenix-prices-sales-tumble-but-thats.html

Phoenix Housing is down .2%. That’s 2/10 of 1 %…..after being up 11% second quarter of ’06 over ’05 and after 47% for calender year 2005.

BTW, San Diego is the most overvalued of all housing markets, having gone up an amazing 127% from 2000-2005 vs a modest 52% for San Francisco and for Phoenix

Does “bubble-watcher” own or rent?

Larry said:

“BTW, San Diego is the most overvalued of all housing markets, having gone up an amazing 127% from 2000-2005 vs a modest 52% for San Francisco and for Phoenix”

Sorry Larry, you’re wrong on your stats:

December 1999 San Francisco Area Median: $420,000

December 1999 Bay Area Median: $374,000

September 2006 San Francisco Area Median: $746,000 (That equals 77.6% not 52%)

September 2006 Bay Area Median: $611,000 (That equals 63.3%)

Either way, not even close to your 52% figure. Just calling it as it is.

LMAO!

Phoenix is down more than San Diego, -9.5% vs. -6.6% YOY, in REAL TIME!!

You can only stretch the underwriting guidelines so much. “

They have and will continue to do so. You post like you have forgotten about the 125% lenders….they are still out there.

This can no longer be the case now, since the Comptroller of the Currency has now changed the loan underwriting rules of the game.

WRONG. Read my next post bubble_watcher

Lenders Loosen Standards

Even as More Loans Go Sour

Banks are making it easier to get mortgages as the housing market cools and borrowers struggle to make their payments. About 2.3% of mortgages were delinquent at the end of the third quarter, the highest level since 2003, according to Equifax and Moody’s Economy.com.

http://www.realestatejournal.com/buysell/mortgages/20061020-simon.html

“Phoenix is down more than San Diego, -9.5% vs. -6.6% YOY, in REAL TIME!! “

Also incorrect.

Leave a Reply