Here comes the inventory: Southern California unsold housing inventory now at 6-year high. Housing starting to plateau.

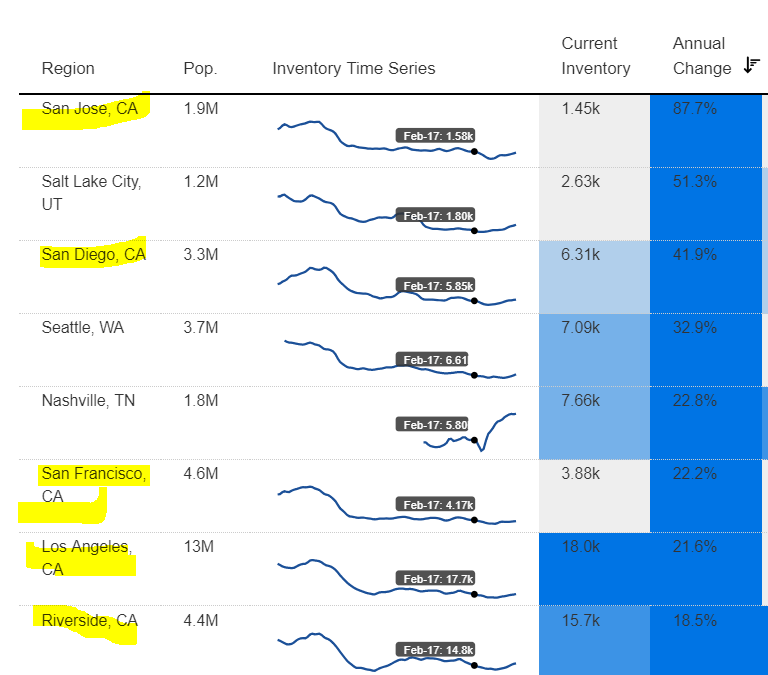

It was only a matter of time before inventory started hitting the market and unsold homes started to pile up. Not that home sales ever saw big volume increases but given the low inventory, any normal amount of homes sales pushed home values into the stratosphere. So here we are with unsold housing inventory now hitting 6-year highs. The problem of course is affordability causing a decade long shift for households into renting. The Southern California News Group came out with 36,923 listings in the four-county region which amounted to a 22 percent year-over-year increase. Housing markets are slow to shift and this bull market is getting close to celebrating a decade of moving up. The troubling sign is that real estate is now in a boom and bust cycle and with rates still near historical lows, there is little ammunition from the Fed should things go south.

Inventory is back in SoCal

“(OC Register) New cracks in the housing market are demonstrating that the cooling trend is here to stay,†wrote Steven Thomas of ReportsOnHousing that tracks homebuying patterns found in real estate broker networks.

Thomas’ biweekly report found a stark change in the market for existing homes as of Sept. 20 vs. a year ago: selling time was 26 days longer as listings grew by 22 percent. ReportsOnHousing watches supply (active listings); year-to-date increase in supply; demand (new escrows in past 30 days); and “market time†(a measure of selling speed, estimated days it takes a typical listing to enter escrow).â€

Inventory is moving up in many California areas:

Part of this has to do with slowing sales and also people trying to cash in while values are high. The market is incredibly frothy and sellers know this. There is now almost a uniform consensus that home prices will not go down or the other variant that believes home prices will moderate down in a controlled fashion. Of course as we now know the market is highly unpredictable but what we can derive from the data is that recent buyers are using high levels of leverage to buy. There are many artificial barriers in California that have pushed prices up and now we hear talks about rent control. One of the largest issues in California is the high levels of NIMBYism

Sentiment is important in housing and the tide is now turning. You have to remember that housing values are hovering near current levels thanks to near full employment, extremely low interest rates, constricted supply, and tax cuts. Yet we do have major issues pending in that we are running ridiculous deficits, have a national debt that will never be paid back, and continue to have this insatiable addiction to uncontrolled debt. In a complex economy as our own, Black Swans are itching to come out.

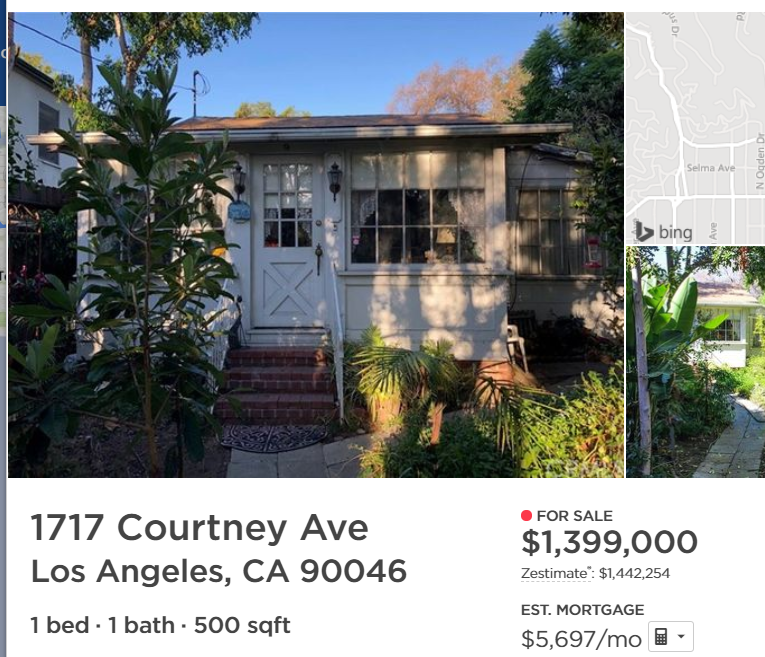

Want an example? Here is what you get for $1.4 million:

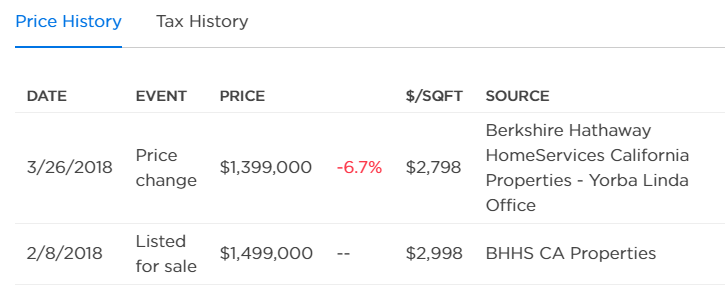

Nice place for you. And of course we have a price cut here:

$100,000 off the original list price. The market is shifting. Inventory is back. Buyers are being more cautious with their tight resources. Market cycles are real and we are definitely seeing signals of a plateau.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

387 Responses to “Here comes the inventory: Southern California unsold housing inventory now at 6-year high. Housing starting to plateau.”

Tide has turned. Peak was this summer.

Its just a gully 😛

What an amazing experience for us millennials. We have seen the last crash in 08, started our careers, profited from the bull run and have now the perfect set up for the next big crash. Just ten years later! I can hardly wait.

How quickly the story changed. I remember just a few month ago RE cheerleader called me crazy because I said the low inventory story is a myth. Here we are: every RE website is reporting rapidly increasing inventory. It shows very clearly that housing data is lagging and slow.

RE cheerleaders also told us day in day out how interest rates will have no impact to house prices. ROFL. We haven’t even entered a recession yet and the market is already turning so quickly. I enjoy visiting open houses, look around and chat. Every single agent is telling me the seller is very motivated. Some even say, “in this market we can low ball emâ€. Agents, especially those who have seen this all before, know exactly what’s to come. They also tell me how sellers base their unrealistic expectations on comps from several month ago. Again, lagging indicator. Sellers haven’t gotten the memo yet. This is going to be so fun to watch how some sellers/flippers will chase the market down (first it sits too long as ask for premium dollars, than you see price reduction after price reduction and open house after open house. Eventually, it has written “no one is interested in buying me†all over the listing).

Let’s see what RE cheerleaders come up with next or if they just disappear/remain in the background. Can’t describe this as a “normal slowdown after summer†forever; especially if summer itself was slow. Lol

Millennial, I know at face value it might be better for you if house prices were to crash. However would your job be secure? Would the money you have be safe? Not disappear with stock market falls or ATMs refusing to work? Would you be able to get a mortgage?

I’m not throwing the gauntlet down at you. Im just really interested to see if you have thought about my comments.

Cromwelluk,

good questions.

“However would your job be secure?”

The short answer is no. And thats exactly the reason why I dont buy before the crash otherwise i might lose the job AND the house.

The longer answer:

I have almost been ten years at my current employer, got several promotions and are well known in my field. During a recession, the company has an excellent opportunity to clean house (get rid of non-performers and older employees who cost too much and can be replaced by younger ones that perform the same and cost less).

If i happen to be laid off, i would just find another job (my field of work is always needed but i might have to take a pay cut). Or, if i cant find another job, i can ride it out. My overhead costs are very low. No debt.

Would the money you have be safe?

I am sitting mainly on cash in several bank accounts (FDIC insured)

Not disappear with stock market falls or ATMs refusing to work?

I hope for a hefty stock market crash so i can buy in cheaper. I dont care much about my 401k. The company contributes 100% of my contributions. Just dollar cost avg. if the market goes up great. if it goes down, even better.

ATM’s not working

If we get a bank run, i will not buy a house, i will buy guns 🙂

Would you be able to get a mortgage?

Sure, there are always lenders, family or someone else that has cash and would lend me money. And if not, i simply dont buy. If i cant get a loan, the majority of people wont get one. I have no debt, cash and 800+ credit score. If we get a massive crash, i wont even need a loan. I just go all in.

Thanks for answering all of my questions. I say respectfully that you have thought it through clearly.

I laughed out loud at your answer to ATMs not working and society collapsing.

If things got that bad would you consider going to work for Tina Turner(Mad Max Beyond Thunderdome)? I assume she lives in California?( Sorry being sarcastic and abit silly 😉 ).

It’s cute the millenial has so much resource yet is one of the few that doesn’t already own the smartest investment asset that they could’ve had for the past decade. ThirtyKMilllionaire is the term

Sigma,

I was desperately trying to find a reason to buy! I think over the past few years I heard every sales pitch in the book. There was no financial reason to buy as renting was so much cheaper (rental parity). Now, that the market is turning quickly I might have a reason to buy within the next 3 years when the market is down (way down).

Can you provide a bit more than buying is the “smartest investment� Any numbers that back this claim? Any examples? Anything but an empty phrase? I already know you won’t reply. RE cheerleaders are very easy to predict.

Not a cheerleader, I actually agree there is a big potential the prices have topped out. If you haven’t already seen the proof that real estate in the past decade was the smartest investment, no amount of data will convince you. My returns in RE investments the past decade has net’d millions and astronomical % but you can convince yourself that you didn’t miss out. It’s cute.

Missed out!? Rofl. Stocks? crypto? (my litecoins made 5,000% in 2017). By not buying overpriced real estate I saved a ton of money each month. I have now a nice war chest ready to invest. People who recently bought RE will be screwed financially and most likely default strategically when we get the crash. And sure, all REal estate cheerleaders are millionaires and none ever lost money. But somehow they hang out here on housing bubble websites and tell everyone now is a great time to buy. That’s not cute but laughable.

Oh stop kidding yourself. Even with your petty crypto investment how good could it be when you still yet to own the most basic investment any amateur investor should even have. It’s laughable, but again, very cute.

You are correct, Real Estate is still missing in my portfolio. I havent had a buying opportunity yet. As soon as we get another 2009-2012 buying opportunity i will buy real estate 🙂

Although I suspect the market has topped out, the probability of there being a 2008 like burst is highly improbable. Even 20% drop in prices off would be extremely optimistic. And if that happens it will be because of the interest rate increases, which means your monthly won’t change anyway. It’s all a give and take. The black swan is the Chinese. If they all dump their holdings all at the same time then maybe something amazing will happen in your favor but if you wait for that you might as well wait for the lottery.

Your statement actually shows me you don’t understand California real estate cycles. Now, I thinking you highly exaggerate your wealth. Or, you are just like all other RE cheerleaders that need to tell everybody including themselves that everything is fine and this time is different.

In 2005/2006 people said buy now or be priced out forever. Now, people say, there might be a drop but it’s going to be very small. It’s all geared to have joe avg buy now instead of wait. You know what, it actually works with joe avg. but even if a thousand people tell me this all day, for 365 days, I would still keep saving and waiting for the reset.

The longer I wait the more I see it play out. Just look at the market now. It only took a few tiny rate hikes to peak the market. We don’t even have a recession yet and sales and loan apps are way down. Lending staff is being laid off, inventory is increasing and asking prices are going down left and right. Again, if you are in denial about these facts it shows you are not what you claim to be. Or you are heavily invested and your emotions don’t let you accept the facts. Denial is actually very common at this cycle phase.

Cute! The guy who doesn’t even own the most basic investment asset is accusing others who do of not knowing how it works! HAHAHAHAHAHAHHAAHHAHAHA CUTE!!!!

Buying alone doesn’t make you an expert. Why would have 7MIO lost their home during the last crash – they all bought? Anybody can buy something overpriced. They offer zero down payment loans with bad credit again.

You gave it away with your comment about interest rates (“its all a give and take”). You seem to not understand the basic principle that it is much better to buy a lower priced home with higher interest rate instead of overpriced home with lower interest rate. I have explained it many times here. In your head its the same because your initial monthly payment might be the same. That’s an indication for me that you are not that savvy as you claim to be.

House prices were ‘too high’ 5 years ago… They are ‘way way way too high’ at the moment. So anyone who bought 5 years ago and sells today made a nice profit, plus bragging rights about using the real estate asset class to great effect! If I were about to sell, I would probably not mention the possibility of a big crash though – not until the deal is closed. So you both make sense. 🙂

Most millenials I know are broke as shit. There certainly are a few that are in good financial shape (chose the correct career path, super disciplined savers, help from parents, etc). Woohoo, the highest inventory in 6 years. The fact is that inventory is still VERY low relative to historic norms. That is all you need to know. We’ll be fighting over that beach close property when the 70% off sale starts. 🙂

Blankfein,

i dont know why anyone would “fight” over a property. The moment a property goes up in price due to a second bidder i am out.

Houses are not like Musk’s flamethrower, were you have limited supply.

BTW, I wanted one but the 20k sold out too fast. He promised, “Works against hordes of the undead or your money back!” You can basically buy one and turn around selling it for a nice profit.

https://www.cnet.com/news/elon-musks-flamethrower-is-real-and-yours-for-just-500/

https://www.boringcompany.com/not-a-flamethrower/

Fighting over a house makes no sense. You just skip that one and look at another one.

However, once i have a portfolio of houses and unload some during a peak, i would def. welcome a bidding war on my property. But participating in one? No way.

Milli: What an amazing experience for us millennials. We have … profited from the bull run and have now the perfect set up for the next big crash.

You speak for all millennials? From what I hear, many are in debt, with less than a months’ rent in savings.

How quickly the story changed. … every RE website is reporting rapidly increasing inventory.

I’m not aware any website is reporting “rapidly” increasing inventory. You added that word.

the market is already turning so quickly.

“so quickly”? Again, you added that phrase.

I see some rising inventory. And a decrease in the asking price for homes. Which is not the same as decreasing prices.

Consider this scenario:

2010 — House sells for 1 million.

2014 — House sells again for 2 million.

2018 — House is listed at 3 million. Won’t sell. So seller cuts price to $2.5 million. Then it sells.

Seller One got $1 million gain in 4 years. Seller Two hoped to also get a $1 million gain in 4 years, but had to settle for $500,000.

That’s not a crash. That’s a slowing in the rise of home values.

SOL,

Dont be a debbie downer 🙂 I dont think you appreciate the change in direction of the market.

Who said anything about asking prices? Just look at this one, posted by Woody. (Median Sales Price of Houses Sold for the United States). If it doesnt help I’ll provide more.

https://fred.stlouisfed.org/series/MSPUS

I am somewhat glad you are still denying. During the peak you have euphoria, after the peak you have anxiety and then comes denial. Its absolutely normal behavior.

https://images.search.yahoo.com/search/images?p=psychology+stages+market+cycle&fr=mcafee&imgurl=https%3A%2F%2Foptionalpha.com%2Fwp-content%2Fuploads%2F2011%2F04%2FInvestor-Cycle.png#id=3&iurl=https%3A%2F%2Foptionalpha.com%2Fwp-content%2Fuploads%2F2011%2F04%2FInvestor-Cycle.png&action=click

And that all sounds totally sustainable and NOT a fucking bubble………..god damn are we in trouble….you’re talking fucking millions to people who barley have enough money for fucking $1,000 a month rent.

I’ve said it a million times, some here are delusional.

Try starting your list in 2006. Now how does it look.

I am not quite sure about your scenario, I have been looking at homes in SJC and Coto, I see houses purchased in 2002-2004, and 2013-2105 selling for 25% less

@Truth….Evidence please. Post links to listings where homes in San Jose just sold for 25% less than they were purchased for in 2002-2004 and/or 2013-2015….We’ll be waiting

“I am not quite sure about your scenario, I have been looking at homes in SJC and Coto, I see houses purchased in 2002-2004, and 2013-2105 selling for 25% less

@Millenial

“What an amazing experience for us millennials. We have seen the last crash in 08, started our careers, profited from the bull run and have now the perfect set up for the next big crash. Just ten years later! I can hardly wait.”

Nearly all Millennials are still poor though and all are still much much poorer than their parents were at the same age. They’re generally not financially positioned to be able to take advantage of any low prices at the bottom of a crash, the rich are. In fact most Millennials will be hit badly by the economic downturn induced by a crash.

And “just” 10yr later???? WTH a decade is a very long time!! That is a large chunk of the average worker’s money earning time period. And they’ve spent that time mostly just barely scraping by. They’ve got no savings generally and tons are still forced to live with their parents for a reason man.

This is gonna get ugly.

Hey Doc:

let us know when that Black Swan event comes… in the meantime, there will be no crash.

Well median prices of sold homes have fallen all the way back to the Q4 of 2016.

https://fred.stlouisfed.org/series/MSPUS

Months of supply of homes is the highest since Jul of 2014.

https://fred.stlouisfed.org/series/MSACSR

It’s not a crash yet but there has been a pretty significant correction.

Let me tell you why this signal is likely incorrect: (even though I am not even questioning the validity of the data)

1) Decrease in national median is most likely increased volume on lower priced properties and decrease on higher priced properties. Nation-wise. This is mathematical definition of median, and many on this forum are not strong in math. If anything, it might indicate a significant increase in volume of lower priced homes Nation-Wide.

2) Such things must be tracked locally AND preferably per category.

Example:

If I have:

1) 20 condos priced at 200 and sold

2) 20 townhomes priced at 500 and sold

3) 20 SFRs priced at 1mln and sold

median = 500k (middle point)

If all of the sudden, I have 30 condos sold at 300, only 10 townhomes at 600 and homes are going for 1.2mil now.

All prices increased, but median is 450k now.

In this case, price increases are driving more volume on lower end.

Decrease in median across nation/price category is not even close to telling the whole story.

First off your being obnoxious now.

So let me tell you why you are wrong. If the sampling size were smaller like an individual neighborhood or maybe a small city your argument would hold weight. When the sample sized used is every house sold in the entire country the errors you are talking about are negligible.

You are confusing mean and median.

Mean over large samples size will “absorb” errors.

Median on the other hand can create significant (or reduce) significant noise.

The result can be interpreted as rising prices are pushing more and more people to consider lower cost alternatives (1 bedrooms, condos, different areas). Relative Volume (and price) for lower cost areas is increasing significantly, while relative volume for prime areas is low (Because of affordability and availability). Some sort of price compression.

Basically, buyers are lowering their expectations.

To truly track prices, you need to track them “Prices Sold” and narrowed down to specific market AND property category.

QE abyss,

No need to search for the black swan. When it’s here you will see this on every news channel. Just be patient. The RE market is headed downhill already without a black swan.

Every time a Republican President transfers wealth through TDE we have a crash. Each time it happens quicker too.

AJP,

That’s a bold statement……to bad for me I bought in 1991 and lost value every year until Bush 2.0 come on scene……so it appears the partisan in you is making shit up, lying or trolling……you pick which.

The president might have influence on employment but zero on interest rates. The FED already raised the interest from the low of Obama years many times and they will continue to do so till they crash the economy. Then, all people will blame Trump for telling Powell many times not to raise the interest.

Please… please… no more “Black Swans”! I posted this link before but I’ll do it again:

https://curiousmatic.com/top-black-swan-events-recent-history/

Another Real Estate Bubble Pop isn’t a Black Swan event, but something that happens periodically. There are enough people predicting it to make it not unexpected. Stock market crashes and other such economic crises happen cyclically and we should all plan for them. Martian invaders (Sic Fi notwithstanding) would be a Black Swan in that our current scientific understanding of Mars is that it is uninhabited.

Yeah I can’t help but feel like RE peoples optimism is bullshit. I was buying my current condo in December 2017 and the RE guy is like, you can refi in like 6 months if you hit 75% LTV to get the better interest rate. And I looked at him and said, “I am happy with my current rate, rates wont be this low in 6 months.” He replied, ” That it wasn’t likely they would rise”. Or some stupid shit like that. All I could think is we have had almost a year of fed rate hikes, you can pretty much count on interest rates going up….

Then bullshit blogs were saying that higher interest rates do not mean lower prices… which obviously too felt like bullshit. Its like they couldn’t even ponder the possibility that maybe the current price hikes were in part due to years of astronomically low interest rates and that a reversal of that would dampen enthusiasm.

The same thing can be said with the stock market as well.

Spot on RangerOne.

You can spot a RE cheerleaders pretty quickly. Its bullshit phrase after bullshit phrase with just one intend…..to get you to buy now.

I have a good bubble 1.0 story that I’m sure could be reproduced now as bubble 2.0 starts to implode.

I sold my house – was way ahead of the crowd and chose to downsize and rent closer to work so I was also selling lots of “stuff” on craigslist. Its amazing how much you can accumulate just to fill the space you have. Anyway, a guy calls me up interested in a few things and we meet in the evening. Turns out hes early 20s and a RE agent (I’m early 30s at the time) and he asks why I’m selling the stuff. Told him I’m selling my house and renting. He tells me I blew it, I should have refi’d, bought another place and rented out my current house – he could have “gotten me a deal”, lol. His car was full of stuff – he had just “bought” his place and was combing craigslist all day and driving around buying stuff to fill his new digs. When he showed up he asked “what were you selling?” – he had so many people he contacted he couldnt keep track of it all.

My house was bought by a flipper who sank 100K+ into it and even with that it took a good 6-8 years to get back to the price I sold it for. I always wondered what happened to that kid, mr. slick RE agent kid.

Oh yeah, I’m still just chilling in a rental. Picture a house like the one in this article, but bigger, nicer and in a much, much, much nicer location. Grand a month. Yeah I may not get to paint the walls (for those that are into that sort of thing – do you get high off of it?) but I get plenty of living in, and I think thats what its all about.

thanks for sharing Govinda.

Many people that are in the field of RE dont see whats happening. They are like most people, spend too much, dont live frugal and cant take advantage from downturns. You would think they read the signs the market is giving or have better insight. Some RE I talked to (and i talk to a lot – each weekend i meet new ones) are very aware of whats to come. One even told me he sold his house for prime dollars earlier this year and is now renting and waiting for the big one to buy back in.

Another anecdote, from last week.

Was taking a walk after work, saw a house which has a good design, I look up the property records online to get an idea of size and layout. Cost of construction wasnt too bad, but that was in 2011 so I looked at some comps and noticed costs are up 50% +. In that same time frame my rent has gone up 5%. NOT 5% per year, 5% since 2010. I have no idea what people are thinking nowadays.

Still not tired of winning!

Guy who bought in 2011; he is winning, his capital is well protected as there is a lot of downside protection from next crash.

Landlord who has not raised your rent (most likely an individual landlord); he is also winning, he is probably cash flow neutral yet probably a massive equity in that home.

If savings few hundred bucks a month is winning for you, ok.

@Govinda, you timed your sale prior to bubble 1 perfectly. But you totally blew your chance to re-enter the market back in 2010-2012 before the big run up. What have we been saying about market timing? It’s nothing short of guessing and gambling. Buy a house you can afford and plan on staying for the long term, then tune out the noise. This is what the VAST majority do.

Back in the late 70’s and early 80’s when mortgage rates were increasing into the double digits, housing prices did not crash. They kept going up but at a much slower rate.

The reason for that was inflation was also rising at a double digit rate and people were getting raises at a double digit rate. Even Social Security was rising at nearly a double digit rate. Everything was rising at near double digit rates except for property taxes of people who owned homes since they were capped at 2% increase by Prop 13.

Housing prices went up but not at the rate of inflation at that time.

This could happen again if wages start increasing again.

If that is the case then housing will not crash though it may overshoot and until wages catch up.

Our Millennial will not find a good deal in housing if this happens. However, someone who bought a house recently will benefit with a fixed rate mortgage at 4%, a wage increase, and a cap of 2% on property tax increases.

IMHO, I think the Fed is turning the inflation and interest knobs up to make this happen in a controlled way. Inflation also helps with the national debt. However, any disturbance during this time could cause instability and a crash.

People like myself and Our Millennial may be sorry to be holding cash during slowly rising inflation.

I fear at times that I am watching this like a frog in a pot of water on a stove under low heat.

Seen it all before, Bob,

In the eighties the median house was 47k. I take 13% interest any day for buying at 47k. Median California household income rose 96% to $35,798 between 1980 and 1990. The house price back then wasnt even 2 times your annual houshold income.

Nowadays, house prices are 5, 6, 7 times more what people make per year. Asset prices are already highly inflated today and have a long way down.

Increasing wages across the board will just be a dream.

https://www.motherjones.com/kevin-drum/2018/08/chart-of-the-day-inflation-keeps-going-up-but-wages-are-going-down/

BTW,

If you havent gotten a raise during this bull market its very unlikely you will get one during the upcoming crash….

During the boom, you can negotiate if you are in a field of high demand. Negotiation can sometimes mean you need to interview externally, get an attractive offer letter and go back to your employer. Meet with the right people. Its incredible how quickly things can change if they fear you are inches away from leaving. That worked for me but it was a bit risky. In case they tell you, we regret your decision and dont try to counter offer, you know they dont value you much. Than you should leave.

Millennial, you weren’t born yet but the reality in Santa Barbara in 1988 was 35K for an engineering salary and we bought a 200K 3 bd 2 bath 1960’s tract home with a 11% 30 year/10 year adjustable mortgage.

The ratio of income to home prices was 1:6.

Not far from today so I’ve seen it all before.

Seen it all Before bob.

You are either lying or whoever wrote that mortgage should be in jail. You make 35k before tax as an engineer and yet just the interest payment from the first year is 22k.

Seen it all before bob,

Can you prove that you bought a house at that time for 200k? You must have bought the most overpriced house during that time if that’s true.

131 total comments so far. 24 of them from ‘Millenial’, without counting how many posts are either responding to ‘Millenial’ or talking about ‘Millenial’.

We have a problem.

Millennial says:

“Can you prove that you bought a house at that time for 200k? You must have bought the most overpriced house during that time if that’s true.â€

LoL, basic middle class homes in freaking south Orange Country were selling for $250-350K in 1990. With double digit interest rates.

$200K in Santa Monica in 1988 is no big deal. Learn something, please just once Millenial.

Nope, this ain’t an alternative fact.

My wife and I bought a 200K )160K mortgage) house in June 1988 . As a starting engineer, I was making 35K. We needed my wife’s parents to co-sign on the loan or we wouldn’t have got it. My wife was making about 16K after she graduated and started working. Total income was about 51K a year after we bought. No kids or fancy cars at the time.

Santa Barbara where I worked and got my first job out of school was very expensive.

We sold in 1993 for 260K. For tax purposes, that was breaking even with the improvements we put in. For rental parity, the interest was killing us at 10.1% and our PI payments were about 1.5K per month. Taxes and insurance were about $300. Total was about $1800 per month.

First year at 10,1%

Interest: $16.1K

Principal: $870

Compared to the first year of a loan at 3.5%

Interest: $5500

Principal $3000

Just think though, if we were like Our Millennial we never would have purchased at this rate. However, 3 years after we bought, rates dropped to 8% to give us some relief. We sold in 1993 due to 2 kids and very cramped space and had about 80K in cash on the deal to spend on the next house.

Now this 1000 square foot house is going for 800K. We should maybe have kept it. It did drop to 350K in 2011, so it would have been possible to buy it back but we would have had to wait 13 years for a crash.

There were no housing crashes between 1988 and 2008. The biggest drops during this time were about 10%

I hope Our Millennial does not have to wait 10-13 years to buy.

Sorry about my math.

There were no crashes from 1988 to 2008 more than 10%. That is 20 years (not 10-13 years). I hope Our Millennial doesn’t have to wait that long to buy.

For proof, here a a good link. It doesn’t show interest rates but you can get that elsewhere. In 1988 we got a 10 year adjustable for 10.1%.

http://www.michellecook.com/blog/a-brief-history-of-median-sales-prices-for-santa-barbara-montecito/

One more thing. I just can’t stop.

Santa Barbara and S.CA was not that expensive in the early 70’s.

My Silent Generation parents sold a 35K house in the Midwest and bought a house in Santa Barbara for about the same price in 1972. That same house recently sold for $900K

Interest rates were about 7% in the 1970’s. I was jealous because our house was 7X the cost and we were paying 10.1%

My point is that the people able to buy a house in the early 1970’s had a great deal. The late Boomers and early Gen-X generation were seeing a 6:1 house/income ratio and to top that, a 13% fixed rate mortgage by the late 80’s.

You Millennials have it good now with such low rates and the same income ratio.

The Silent Generation and early boomers had sane prices.

Millie is a modern version of energetic vampire

Affordability has 3 components, housing average price, average income and average financing cost. If financing cost goes up, then income has to go up or price has to come down to maintain the same level of affordability. Of course California affordability is so low that normal economic truths don’t seem to apply now. Either we are in for a very rough ride, or the one number that is most difficult to track (income) is bogus in today’s statistics (underground economy anyone?).

Definitely more inventory BALANCING the market. It really all depends on the property, listed price and location.

Have 2 different escrows right now. First one sat for 60 days at around 300k (Inland Empire) and dropped the price to 290k and buyer came in and got offer accepted.

Second one, (in Orange County) first weekend open house; 3 offers at or above asking price. My buyer got it at 605k; original ask was 595k.

Generally I don’t see this as a completely tilted sellers market like the last few years, and buyers are a little more picky now, but, I would hardly call this a “crash”. It’s nice to see a little more balance where the seller doesn’t have such control.

“Have 2 different escrows right now”

I feel so sorry for those 2 people right now, been there, done that. Good for you to get out at the top though.

Still amazed on how quickly things changed from just a few month ago. I would have never thought the RE market can turn the other way that quickly. Fascinating to experience this in real time.

Dan, do you have stats on increased inventory YoY and price reductions MoM?

I love being flooded with emails from zillow, redfin and others telling me price drop here, price drop there. Thats fun!

I received 10 notifications from Zillow today about 1% – 4% price drops in the Temecula area. My dream house with my dream weather may become a reality. 🙂

There’s also the possibility of a 20-40% drop and then go sideways for three or four years. Don’t celebrate just yet Mille.

Milli: Still amazed on how quickly things changed from just a few month ago. I would have never thought the RE market can turn the other way that quickly. Fascinating to experience this in real time.

It’s easy to be amazed when you’re fantasizing. In “real time” there’s been no “quick” change. A slight change, at slow speed.

I love being flooded with emails from zillow, redfin and others telling me price drop here, price drop there. Thats fun!

There’s no “flood.” And it’s only fun if you’re buying. Which you’re not and won’t.

The problem is the banking sector has removed the natural business cycle and replaced it will a credit cycle. Credit is either expanding and causing an economic boom of mal investment or it’s crashing. Whenever I hear people talking about leveling out I just laugh since they clearly have no understanding of how money works in our current debt based dollar system.

Millie,

No, I don’t have those stats. I will leave those to the statisticians on here or the doc. I can only report what I am seeing and hearing from the 30-40 agents I work with.

Yes; inventory is rising and sellers generally do not have the power or leverage they once had. Buyers can be more picky or ask for seller credits or repairs to be done where before sellers would balk, they now are agreeable. Some sellers are unrealistic and list high which causes the property to sit.

Overall, from what I see, there is definitely more balance in this market right now. Some areas property may just sit, while other areas properties will go fast (if priced right). It is interesting to see as it became noticeable about 5-7 weeks ago.

Turn what other way? You’ve been denying the inventory data for months and suddenly you’re acknowledging it? The only thing turning here is you.

SOL,

a “slight change” huh?

First we heard its the “normal after summer slowdown”. (except that summer wasnt hot, it was quite the opposite of hot)

Now we are hearing its just a slight change.

Keep in mind, a few month ago, we were told this spring season is going to be epic.

Maybe an epic fail was meant by that?

A few questions:

Have you visited an open house lately or talked to agents? 6 months ago they sounded A LOT different from what they are saying now. You havent noticed a change in their message? (what they are telling me is “Sellers havent gotten the memo yet, they base their asking prices on comps from 5 months ago. the market has changed/cooled/turned/shifted”.

Does inflection point mean anything to you? https://www.geekwire.com/2018/redfin-ceo-warns-slowing-national-real-estate-market-frustrated-buyers-sitting/

You are not being flooded by zillow, redin emails about price reductions? Are you signed up with these sites? Do you save favorites on these sites? Are you sure the email you entered is correct? Have you visited any new home models, signed up for their newsletter and receive their emails about increased incentives and price reductions?

“Turn what other way? You’ve been denying the inventory data for months and suddenly you’re acknowledging it? The only thing turning here is you.”

What you see with your own eyes (more open houses, more homes for sale, more inventory in new homes, houses sitting longer on the market) can be very different from what you read on blogs dominated by RE cheerleaders. The current state is a confirmation for me.

Month ago when the market started to turn I challenged the There-is-no-inventory myth. Its one of the RE cheerleaders remaining sales pitches to get you to buy high. Here we are, months later, and the news are reporting it (rising inventory). The delay in reporting is somewhat expected due to lagging indicators.

If you dont believe the market is turning (despite all the articles/recent news), just put your house on the market. Base your asking price off of comps from 5-7 month ago and see how many offers you get.

Last year you would have gotten 10 offers flying in. That’s no longer the case. Houses (not just in Temecula) sit much longer, listings expire or sellers give up and take it off the market and try to rent it out.

Millennial is a dishonest shill. The very same inventory data he denied a while back he now is acknowledging. I point it out and he then spins the truth of what he claimed in the past. He has an agenda to sell just like jt and lord blankmind.

I would say it this way: I denied the fabricated story during summer that there is no inventory. That’s because i saw more inventory, more listings, more open houses, more new construction, houses not selling as fast as last year and a change in communication when talking to agents. I don’t deny data, I use it. But as i often say, housing data can be a lagging indicator. “boots on the ground” see that earlier, before you see it on your screen. These agents see that foot traffic at open houses slowed down, less buyer interest, less offers etc. Some agents are transparent, some dont. But by talking to a lot of agents and lenders you filter out the generic sales pitch and identify the trend.

3 Month ago, RE cheerleaders were repeating the same line about inventory. You dont hear that anymore, do you? Some here give me credit, some are sour grapes. That’s ok. Just move on and adjust to the changing market.

If you need to sell, you might want to price a bit below the market and throw in incentives. Otherwise, you might find yourself chasing the market down. Prices are only going down from here on now. (due to rising inventory, higher financing cost, bull market cycle ending, upcoming recession, impact by new tax laws (SALT, increase of std deduction).

Millennial is still pathetically spinning and shilling hard. He’s so deep into it that there’s no way out aside from admitting it so he spins even harder.

The way he does it is by putting up a strawman argument against something no one was actually saying. No one who is anyone was saying there was no inventory. What was claimed is that the inventory was historically low. It’s called months’ supply and that’s the common metric which has been used for decades. Millennial wouldn’t know this first hand because he was still shitting in diapers only two to three cycles ago. Instead of saying LOW inventory he says NO inventory. See how he does that? It’s a distinction with a difference.

The other thing he does is that he won’t clarify which market he’s referring to when making claims. He makes general sweeping statements as if it applies to housing across the country. Maybe he’s talking about bumbfuck central valley CA or maybe he’s talking about wannabe manhattan beach adjacent…..who knows? He purposefully won’t be specific and when cornered defaults to bitching and moaning about real estate agents in order to distract the conversation. Just a bumbling moron this guy.

https://www.corelogic.com/blog/2018/06/us-economic-observations.aspx

Darn it! Now there is another Millie and nobody will know who we are insulting anymore.

Our Millennial has been trolling us for over a year but he has excellent points. He is almost the only person on this housing bubble blog who thinks there is a housing bubble.

Our Millennial and I agree that there will be a housing drop. With the economy the way it is, I think 10-30%. An 80% drop will require more than stagnant wages and record employment.

But Hey! If Trump starts a real war with bombs, well, that will cause at least a 50% drop.

Why else do we need the Presidential Alert to be online and functioning?

We will all suffer to MAGA because there will be some very good reason that it is justified. WMDs or something else. Our Millenial and I will be buying our homes at this point and hopefully not be labeled war profiteers.

Otherwise, housing will drop 20% and then flatten and inflation will rise at 8% for the next 8 years and like frogs in a simmering pot of water, we will endure like good Americans have done in the past.

Bob,

Millie is just a copycat. People try being like me. Not surprised.

Insults? Lol, what insults?

And I thought you said before I am just semi-trolling… what changed?

I’m sorry, Millennial. That was a typo.

You are still a lovable semi-troll in my opinion with many good points coming from your naivety. This housing bubble blog has many housing bubble deniers. You are standing your ground and doing a great job. Keep it up!

“lovable semi-troll in my opinion with many good pointsâ€

🙂

I think Trump;s trade wars are hurting the Chinese market. It will take some time but the interest rates have to keep going up.

I think I’m getting in tune of how and what is playing out and China is a big part of it..

We have seen this play out before in California and other states before. Cycles play out over and over again….a correction in housing with chinese market cycle down will force margin calls, a lot of them….

The Chinese were big time buyers in Vancouver, too. Now Vancouver just experienced 44% (Y-O-Y) drop in sales during peak selling season. Same for Hong Kong, Seattle and NY. These are prime international markets not flyover country.

China is going to play a big part in this move down, I see some cycles repeating, think I have a good handle of outcome. A different player to push hard….

Same thing is happening in NYC (as reported a few weeks ago):

https://streeteasy.com/blog/price-cuts-hit-record/

The most listings posting a price cut since 2009. Good for the little guy I guess: if the real estate market doesn’t take everything else down with it and we all lose our jobs again…

1.4 million for a 500 square foot house? A real home of genius it is! If that doesn’t make me want to pick up and move to SoCal I don’t know what will.

Respectfully, the house is a shabby tear-down. Go to Zillow and look at the photos. Also, per Google Street View, it’s next to an older 40s-50s apartment house, so it’s a possibility for a multi-family. The neighbours will almost certainly object to that, so the the likely alternative is a substantial update and expansions in line with the other houses on the street, many of which seem to have been updated as well.

Supposedly it’s in a low crime area of the Hollywood Hills, so that’s probably driving a good bit of the price as well.

That doesn’t mean that there’s not a bubble in process overall. Rather, it merely highlights that it’s in a relatively good area

Hope this helps.

Just a thought.

VicB3

I’m waiting for a nice crash so I can buy a nicer home and rent mine =). This is the reason why I bought my current home solo and my wife kept her credit and income separate on everything!

I’m waiting for a nice crash so I can buy a nicer home and rent mine =). This is the reason why I bought my current home solo and my wife kept her credit and income separate on everything!!!!

Ummm. This is NOT even fun yet. Wake me up when RE is down 30%. These tiny little reductions are meaningless. Most people are overextended and can’t afford either rent or a mortgage.

Irvine prices continue to increase. Although there is definitely more inventory prices are not showing any signs of slowing down.

Irvine, compared to a number of high-profile markets, is driven more by employment/housing balance and less by speculation (though far from none). So it’s a little more resilient to the sentiment shift lately. It will follow if things continue, though.

Same here in San Mateo county, no price slow down in sight and still low inventory. Still $1mil. for a 1,200 sq ft. outdated crap shack. It seems the most desirable locations in CA are bullet-proof during and since the last crash and even if prices fall elsewhere they will stay strong, even within the same county or region.

For example if the Big Millie crash does happen places like Anaheim and Garden Grove will drop 40% or whatever and Irvine and Laguna Beach will only drop 0-10% or up here in the Bay Area Petaluma and Santa Rosa May drop 40% but San Mateo, Hillsborough and San Francisco will probably hold strong,etc. I could be wrong but it seems that some of these areas are so desirable with limited inventory even a crash can’t hurt them much at this point. Im sure there will be plenty of areas near and far from these spots where prices significantly enough to open the market back up to those of us that are priced out but then other issues such as reasonable lender financing and competing with investors,etc. will come into play.

According to Millie, those 1M houses will be going for 300 to 500K after the collapse. Just be patient and keep your money in that 2% CD. What could possibly go wrong with that plan. Interest rates may be approaching 5%, if home prices aren’t budging that means monthly payments are going up and up for new buyers. Those 3.5% rates from a few years back with home prices 30% lower look like absolute bargains now!

Lord Blankmind,

yes, 5% mortgages are almost here. I am sincerely hoping for 6-7% mortgage rates for the 30y conventional. Remember, you want to buy a lower priced home with a high interest rate. not the other way around (inflated home price and low interest rates).

Some here know this already: low interest rates inflate asset values. High interest rates are no issue. You just re-finance later. To say that low interest rates are a bargain works only on fools.

We’re targeting the peninsula and are starting to see price reductions in Belmont and Burlingame. There are many more houses in the 1.3-1.6 million dollar range than there have been in years because these didn’t sell at 1.8. The Peninsula is slower than say Santa Clara, but it’s far from immune. A stock market crash and 6% interest rates in 2019 will knock it down to size.

“Some here know this already: low interest rates inflate asset values. High interest rates are no issue. You just re-finance later. To say that low interest rates are a bargain works only on fools.”

Millennial is the one with a blank mind on this point. High rates means less paid down toward principal over time for borrowers so it’s a real issue especially now that you won’t be able to claim it in high tax states…gee the timing must simply be coincidence that the Trump reward goes to the low tax states.

Either way high prices low rates or low prices high rates there is no free lunch it’s the same suck at both ends. Good lord blankmind this Millennial guy has the gall to talk about fools!

Your statements show you must be new here or you simply don’t understand basic real estate principals. I’ll help you with it, one by one.

“Millennial is the one with a blank mind on this point. High rates means less paid down toward principal over time for borrowers”

Over time? Over time the borrower has the opportunity to re-finance when rates are lower. Higher rates mean lower purchase price. Lower purchase price means you pay less interest over the duration of the loan. In case you struggle with this, i’ll make it even clearer: Think of the purchase price as your base. Unless you pay in cash you pay interest on that base (loan). If the base is lower, you pay less interest, if the base is higher you pay more interest.

The beauty of having a low base (derived from a low purchase price) is that your overall cost will be lower. Less property taxes and less interest (just re-finance down the line).

“so it’s a real issue especially now that you won’t be able to claim it in high tax states…”

That’s not an issue, its a bonus. Taking away subsidies is a good thing. Subsidies and artificial low interest rates inflate the market. In an artificially inflated market you overpay for the same house. We want a deflation of the market so that i can buy in at a low price.

“Either way high prices low rates or low prices high rates there is no free lunch it’s the same suck at both ends.”

That’s a fallacious argument. Low prices and high interest rates are much better financially for the above reasons. To say it in other words (sometimes that helps): A purchase price can never be changed once you signed. Interest rates change over 30 years – constantly.

You might have a certain agenda or its just poor analysis which makes me believe you must be new here. Lack of experience is another potential reason but in that case you should probably post less and research more.

Meant “principles“. I blame my phone for the typos.

IrvineGirl

Could you kindly share your data source(s)?

Can you cite just of couple of MLS #’s that have posted recent price increases?

I have lived in Irvine for 40 years and follow the market.

For all the MLS listings I track (mostly in Turtle Rock and Shady) I note a steady stream of price *reductions* on a daily basis.

Rarely see a price increase anymore, and even then I think these increases are Realtor fantasy maneuvers.

I get my daily feeds from Redfin and Coldwell.

I’m not an expert in the Irvine RE market but I do have some experience there which should lend me a little bit of credit. I used to work as a quality control manager for Ol’ Man Donald Bren and Irvine Company from 2013 to about 2015 and Irvine was absolutely BOOOMING during those years. We did a market study because this was unusual compared to the surrounding areas and found that 90% of buyers were from mainland China and 75% of those buyers were buying 2 or 3 houses at a time, all cash. Obviously this isn’t very surprising but one can deduce that Irivne is largely driven by the Chinese economy and their monetary policy. I haven’t been back in Irvine since then but I would imagine a slowdown in that market is likely considering the current state of the Chinese economy. However, Irvine has always been and will continue to be highly desirable by the Chinese and they will continue to fuel that RE market. I’ve always said that Irvine is like the SF of Socal (in terms of price movement). SF didn’t drop much during the Great Recession and I simply can’t see RE prices dropping in Irvine either.

If you look at the banking, corporate, and consumer debt in China you realize none of these houses were purchased with cash. There are loans on top of loans financing those things. It probably looked like cash because of the complicated financing they used to get the money out of China.

If you go on zillow and do a search u can then toggle show price reductions. I. Consistently seeing 20% or more of listed homes showing price reductions. Just ran this search for Santa Monica up to $10million and then down to $1m and points in between. Consistent reductions across the pricing range.

You have to be careful with price reduction stats. In markets like this, many sellers get greedy and price their homes well above comps. After a few weeks, reality sets in and the price is lowered to market value and the home sells. Here in the South Bay, anything at market value goes quick. No rocket science here.

I rent in Monterey, Ca. I moved out of my last home on June 30th, because the homeowner wanted to sell the home. The for sale sign went up on July 2nd, listed at $798k. I thought it would sell within 30 days. It sat on the market for almost 3 months, and the seller lowered the price 3 times. I drove by the house about one week ago and it was no longer for sale. It was for lease. The owner didn’t want to lose any more money. The market is turning! Big time. It’s 2008 all over again.

How is this 2008 again when owner decided to keep the home because he cul not fetch the price (inventory not increased)?

If you are renting, it is likely that you will never own a decent SoCal home. You would be better off moving to a home on the outskirts of SoCal, or head to a different metro area. Just to get a 50s ranch house with a back yard on in a decent location starts at 1.5M. You need a 150K down payment. Then, you will be making payments of around $8600 per month which includes taxes. Add in PMI, and you are north of 9K per month … for 30 years. Good Luck with that one.

There was a shot in 12 and 13 to get in. For example, east Manhattan Beach was at 900K for fixers, Now, those are approaching 2M. Even the 700K deals in South Redondo from back then are now starting at 1.3Ms. Still possible to squeak into west Torrance for 1Ms, but you are usually fighting multiple offers over there.

If you missed your chance, you can move somewhere like Texas. I just visited someone who moved there last year … they cashed out their SoCal home and moved after a job loss. Their new situation is very nice. Nice people. Fun places. Beautiful women. Great dance floors. And, their payment is reasonable. jobs are good. Sounds like a better life if you missed the SoCal housing market. Don’t waste your time here. Get on with your life. Life is short and you will be old with health problems before you know it. It is dumb to waste your life waiting for the unlikely huge price drop.

Sounds very tempting. Who doesn’t want to move to greener pastures…eh greater dance floors.

I’m gonna pass though, stay put, rent cheap, save and wait for a nice crash.

It was a good try though JT.

So us recent grads just starting to save are just going to forget about living in SoCal and leave? If that’s your theory then there will be reduced demand for housing and no one to buy your 1M+ shack. With wages not keeping up, there’s no way the price increases can sustain.

That is not right. If you are young and out of college, and you are a success, then by all means stay. A portion of people your age will land up making more than 300K per year. I would grab a small beach house and stay.

But, if you land up below 200K with no hope, then forget it. Not worth the trouble. Find a more affordable city.

We’ve been priced out forever

“We’ve been priced out forever.â€

Pretty much this^

Funny seeing people here comment on price reductions on houses over $1mil. Lol.

The issue in reality is that so many houses here in CA are close to or over $1mil. and aren’t even close to worth that and no normal people can afford to buy a home in that price range. Let me know when “price reductions†aren’t a $1.4 mil listing reduced to $1.2 mil but when a $950k crap shack rancher is reduced to $350-450k or a price that is feasible for anyone making under $250k a year etc.,etc. blah blah blah

“We’ve been priced out forever”

That is what people were saying in the late 80’s when S. CA prices were 200K and starting professional wages were 35K.

How can anyone afford a house when their PITI at a 12% fixed is over 20K and the wages are 35K?

This is how we overcame it in the late 80’s

1)Have a relative who will co-sign the loan.

2) No kids for the first 5 years

3) No fancy cars, boats, vacations for the first 5 years (10 years if you have kids).

4) Hope for high wage inflation. Us late boomers and Gen-X were lucky to have 10% yearly wage increases due to inflation In 5 years, the 35K yearly wage is now 51K and the mortgage is easier. Will the priced out wage earner who makes 200K today be making 350K in 5 years?

5) It won’t be as extreme now, but hope interest rates fall and the PITI drops to 15K/year. Our interest rate fell from 11% to 8% in 4 years.

6) Huge mortgage interest deductions helped at 17K+ per year. Prop taxes were relatively low at around 2K.

That’s how people my age overcame the “We are priced out forever” We squeaked in and then with the economy and luck with high inflation, high wage growth, and lowering interest rates, life became easier in 5-10 years. Rental parity was blown away at that point since rents were 3K per year in less than 10 years due to infation.

Strange to say, but we were lucky with high inflation and high rates. It is likely we will see high inflation again and I hope wages rise at at least that rate. If rates go to 6%, they may fall again in 10 years and today’s Millennials can repeat.

We bought in 2013 and our house price has nearly doubled. We barely got in at that time. Our wages have gone up somewhat these past 5 years however based on today’s house prices, we would not be able to afford our house.

Wages increases have not been keeping up with true inflation rates. We barely make ends meet with regular life as everything has gotten so expensive to buy.

The Feds have done a good job of pushing housing and stock market prices with money out of thin air these past 10 years. However, inflation is roaring at 12% a year in Los Angeles. Check out the Chapman index.

Fed’s need to quickly raise interest rates to slow down the ridiculous rate of inflation. This will certainly cause housing and stock market prices to plateau of go down I think. Not sure.

The recession is still years away. Maybe 2020, maybe 2022.

It’s funny to watch amatures like Mellinial in real time.

A few months doesn’t make a housing market especially if you are comparing inventory over the last 6 years.

There have been several periods of softness in 2013, 2014, and 2016.

The question is how much will the housing market and rent run up before the next recession. Trump wants 1970s style inflation and he may get it. The next recession will see 15-25% price drops in the prime areas of Orange County and LA. In the less desirable areas you are looking at 25-50%.

The current state of the economy and housing is a giant nothing burger. There are still blue skies in sight. It won’t last forever though, follow websites like calculatedrisk if you want to time it correctly… still years away. I am not even on recession watch currently. I will change my name when that happens.

Notankinsight,

“The recession is still years away. Maybe 2020, maybe 2022.”

Nice, that’s not too far out. More time to invest and save.

“It’s funny to watch amatures like Mellinial in real time.”

Its amateur and Millennial or just Millie 🙂

May I ask what makes me an amateur and what makes you a Pro?

Because you read on https://www.calculatedriskblog.com/ and know exactly what will happen within the next 2-4 years?

“A few months doesn’t make a housing market especially if you are comparing inventory over the last 6 years.”

Nobody said that. You are looking for a change in trend (Inflection point). The hot spring season 2018 was supposed to be epic, remember?

I wouldn’t make fun of those following Calculated Risk for economic info… it’s a very very very dry boring site compared to this blog. Most of the data would go over your head. But, he nailed to the exact month when the housing market turned south and headed north. I always make sure to check in occasionally on his blog to see when he’s predicting the next downturn.

That’s good to know! I will check it out. I don’t think I made fun of the website. I am trying to understand why notankinsight thinks of himself as a pro.

My opinion is a recession just around the 2020 mark. But, that is a guess. And, I agree with the 15% to 25% price drop … but, this time there is a possibility that the price drop could be smaller if inflation gets rolling. With the trade wars, you might see an inflationary recession, which means the 15% to 25% price drop might be more like 5% to 15%.

The real problem is banks tighten lending standards during a recession. So, it takes a much much larger down payment to get in because lenders want protection against falling prices. During recessions, the appraisals come in very low, and you will be required to come up with a much larger down to cover the gap. That is a tough situation.

WOW, even JT jumps on my train now? Talks about recession in about two years and even mentions up to 25% price drops! A few month ago he told us that we need to buy now or be priced out forever.

“My opinion is a recession just around the 2020 mark. But, that is a guess. And, I agree with the 15% to 25% price drop … ”

“The real problem is banks tighten lending standards during a recession. So, it takes a much much larger down payment to get in because lenders want protection against falling prices. During recessions, the appraisals come in very low, and you will be required to come up with a much larger down to cover the gap. That is a tough situation.”

I would hardly call that a tough situation! Thats the perfect situation for someone who has cash. That’s why i have been living frugal, kept expenses low the last decade and saved, saved, saved. A low appraisal is a beauty! You negotiate the price down even more and cover the gap between price and loan with cash.

NoTank,

I would agree with your assessments. The environment we are currently in is NOTHING like 2006 right before the last big crash. We’ve had the most qualified buyers EVER the past decade. Add in super low unemployment, record stock prices, homeowners swimming in equity, an administration that is pro business…all this combined will make it very difficult for an all out housing collapse.

Sometime in the future, there will be a recession and home prices will decline. When and how much, nobody knows. And just like last time, strong hands will come in take what they want. To think your average joe sixpack will come out on top this time is laughable.

The administration is OK, but it scares me what the FED (Powell) is doing. He is maybe .25% from neutral rate. He said he is planning to go way over neutral rate into tightening territory. Add to that about 50 Billions monthly QT and he may blow up the bond market which is 3 times larger than the stock market. He may even blow up the treasury market which is the most senior asset class, the bedrock of the whole financial system.

With these people you never know what they pursue. For sure it is not the well being of the middle class. I know they pursue wealth concentration and transfer and for that they might create another depression.

The credit profiles have nothing to do with what is going to come. What we have is the most INDEBTED buyers of all time. That debt is what is going to cause the crash when they are no longer able to service it and creditors start to fail causing the monetary base to collapse. The collapse of the monetary base which was created by the banks occur all assets will get repriced.

housing always tops before the recession…..pti, dti and ltv too far out of whack….now you have Paulson and Geithner actively discussing rental pricing is killing the economy….expect housing to go down for a while….the fed has a new mandate…..

Berkshire Hathaway Home Services ? …….You might as well give up the fight right there Doctor. Vested powerful interests have high motivation to keep this bubble inflated….money printing, taxpayer funded bank bailouts (again), whatever it takes, but the housing market ain’t going dowm much.

“Did you ever get the feeling you’ve been cheated?” – Johnny Rotten

yep, same story on each cycle. This time is different. This time its a soft landing.

A little off thread, but wanted opinions..

Two interest rates I see often, my Bank’s CD rates and the Cap rates I get on commercial RE email offers I see daily in my inbox.

A few years ago, Bank CDs were 1% and the NNN Cap Rates I would see were 3.5% (on a bank branch lease, shopping center etc.) Now my bank’s CDs are in the low 2s and Cap Rates are being advertised in the mid 5% range.

If I can get 5% on a CD (which prior to 2005 was normal) what would the Cap rate need to be on commercial RE?

You know, even if real estate crashes, I’m not sure that I want to buy a house here any more. The housing stock is old and even if you do (expensive) updates, there’s no guarantee your neighbor’s ancient property won’t pass on the termites and rats it’s hoarding — I know that from renting. There’s also no guarantee somebody won’t build a McMansion or worse a 5-7 story apartment building 200 feet from your bedroom window. And of course there’s no guarantee that an earthquake won’t completely wipe you out. I’m starting to think I’d rather rent, save my money, and buy something nice someplace else for an early retirement.

“…neighbor’s ancient property won’t pass on the termites…”

Termites or no termites, the major killer these days as far as I am concerned is the traffic.

I have lived in SoCal (OC) my whole life. (70 yrs)

In the 1960’s I could drive the 5 freeway to WestWood to see a movie under a hour no problem.

Last Thursday, I went to Pickford Center for Motion Picture Study (near Hollywood and Vine) to see a documentary. Took me 2:45 (I logged the time). Average about 20mi/hr.

Parked and then attempted to walk down Vine St to grab a hamburger before the show. Just about add to trip over homeless people.

Maybe its me, but I keep asking myself if it is worth it anymore.

Would be interested in hearing from other long time SoCal residents about their own quality of life and does anyone have a solution?

I used to live in SoCal, but not for 70 years like you. Based on my travels, it did not take me too long to figure out that Flyover country offers a far better quality of life than SoCal.

However, if people love to be slaves to the banks with a millstone of debt around their neck to sink in despair, that is their choice. That means they really love their air pollution, traffic bumper to bumpers and all the homeless around them. Who am I to take that pleasure from them?

Productive normal middle class people have been leaving for years. Increasing numbers of established wealthy are leaving more recently. Third world poors, clueless young dreamers, and nouveau riche douchebags have been moving in. Any questions?

With the olympics coming up they are building out mass transit fast.. so you will soon have options besides sitting in heavy traffic.

I did 17 years in SoCal, was burnt out after about 10-12. Traffic is too much and I would shine going to lots of events the last 3-4 years because the traffic would add 2-4 hours to everything. I even visited my family less because I dreaded the traffic. In retrospect maybe I should have taken the train more for those norcal/socal traverses, but I wasnt clued in to that at the time.

Its funny because I moved to “flyover” and while my commute was still high for a while (30-40 mins) there was never any traffic so I felt much less stress plus it was beautiful scenery – ocean, mountains, etc.

Bottom line, I think there are places in flyover that are much more attractive to live in than the “trophy” places such as much of coastal CA – unless youre already wealthy. I cant fathom spending so much time in traffic and working every second of my life to rent/own a shack I dont get to see that much anyway.

How do you get ocean on a fly over state? AZ, TX, LA?

Goodtimes – “How do you get ocean on a fly over state? AZ, TX, LA?”

You don’t. If you like ocean, you stay on the coast – Atlantic or Pacific. Just be ready to pay for it.

This is the difference between Calculated Risk blog and this one – due to the combination of participants on this blog, this one is very entertaining.

On top of getting information and opinions, I get a good laugh. Each one is funny in his own way.

“With the olympics coming up they are building out mass transit fast.. so you will soon have options besides sitting in heavy traffic.”

That’s the best joke we’ve ever seen on here….thanks for the laugh! Soon we’ll have more options to stand around waiting for an opportunity to be shoved up against the smelly general public in a box to somewhere that isn’t quite our destination! The third world lifestyle of dependency is gonna be so worth waiting for. Maybe we’ll get to star on a youtube video of ghetto degenerates berating fellow passengers. Private transportation is for squares!

I consider flyover to be any state where there are few to no elites who are high on their own “smug” (southpark reference). That could be Louisiana, Alaska, or a number of other states/territories.

millie called it..slum lord et all will still spin this info to benefit them…its their mo…remember millie, they’re soooooo smart…lol

🙂

Increase in price drops does not mean median prices are dropping. Just means sellers are too un-realistic (“greedy” for those who prefer to be childish).

Example:

Last year, home is purchased for 1mil.

Same home is placed on the marked for 1.1, but sold at 1.05 (price reduction)

You get both, price reduction (bears are orgasming) and YoY price increase (bulls are climaxing).

Price drops and time on market are transnational noise which is increased due to incorrect pricing.

Median YOY price change is what really matters (Among with affordability). Former is increasing, while latter is decreasing. (Although at slower pace).

The median price has fallen about 10% from Q4 2017 to Q2 2018 (it should continue into Q3 of 2018 but we won’t know till end of November). This is inline with the math on higher interest rates. As the bond rates continue their climb (which has increase lately) home prices are going to get pummeled.

not sure which locality you are referring.

Just about every county in California has experienced a price increase from Q4-2017 to Q2-2018. Does not mean it won’t turn at some point (of course it will), just has not happened yet and prices still growing.

I am referring to nation wide based on federal reserve data.

https://fred.stlouisfed.org/series/MSPUS

Due to the Trade War with Red China, the real estate market has peaked.

It was always and forever dominated by Red Chinese political criminals hiding their loot.

They drove Vancouver to the Moon… and many another place.

Now both the Russians and the Red Chinese no longer feel save parking their assets in the West: London, California, New Zealand, Australia, Canada.

Indeed, some are looking for buyers so as to move their assets further on.

This is the crowd that didn’t need to obtain a mortgage.

They shut out all ordinary buyers in those markets they wanted.

Just as predicted here… YEARS AGO.

That is true. I said the same thing before. Add to that the constant increase in interest and the QT (instead of QE) and it is not surprising that many markets suffer.

I am not sure how high the interest will go and how long the QT will continue. That will determine how fast and bad the markets will turn down. Powell is saying “a lot”. Remains to be seen – bluff or trying to emulate Volker?!?….The higher interest to be paid from the Main Street for the mountain of national debt will crowd out everything, including housing.

oh god it’s you again with the inane ramblings… do you have a point? If so would you please let us know what it is?

The Chinese have blown the largest bubble in the history of humanity. They are going to pay the highest price ever for it.

You also predicted Obamacare would tank the economy. You and Jim Taylor should start a blog and keep predicting the future. Lol.

This Santa Monica townhouse is typical of Milli’s “rapidly changing market”: https://www.redfin.com/CA/Santa-Monica/931-10th-St-90403/unit-B/home/8143000

2010 – sold for $1,350,000

2018 – listed for $1,995,000

2018 – sold for $1,860,000

Milli might say, “Wow! A price plummet of $135,000.”

When in reality, it’s a price increase of $510,000.

Milli gloats over lowered list prices (as though a list price means anything) and ignores the increase in sales price.

SOL,

I believe I can help with your confusion a bit.

Yes, the market is changing rapidly. We hit a wall in May/June. Affordability issues, a slowdown in foreign investors, rising interest rates are contributing to that rapid change.

Here some help to clarify things for you:

Sales volume:

Has plummeted. If you google it, you will find many articles.

https://www.cnbc.com/2018/07/24/southern-california-home-sales-crash-a-warning-sign-to-the-nation.html

No matter how hard RE cheerleaders try to sucker in the last buyers….the facts show there is an unbelievable reduction in sales volume.

Seasonality:

usually, spring/summer is the hot season. Not this year. Instead of houses selling above asking, we see houses sit longer on the market, asking price reductions, more open houses and increasing inventory. In the past you would see a slowdown in Aug/Sep after a red hot summer. This has been echoed from different locations (e.g. Seattle) not just SoCal.

Interest rates:

When rates go up, prices go down. Higher interest rates have translated into higher mortgage rates (there is a lag, meaning it takes a few month until you see the impact in dropping demand due to higher rates).

Asking prices:

Yes, its a great sign to already see drops in asking prices. That’s a sign that the market is no longer going up. Real Estate agents call it cooling, turning or shifting. Again, that happened during the “hot season”. Sure, that doesn’t mean we have a buying opportunity yet. The RE market is like a cruise ship, it takes a few years of price reduction until we have a nice buying opportunity.

Median sold prices:

They dropped to 2016 levels nationwide:

https://fred.stlouisfed.org/series/MSPUS

I hope this helped. Let me know if i can assist with anything else in terms of terminology.

Milli: “I hope this helped.”

No, because you contradict yourself. Above you say: “The RE market is like a cruise ship, it takes a few years of price reduction until we have a nice buying opportunity.”

Yet in an earlier post you said: “How quickly the story changed.”

So is the crash coming rapidly, or is it a cruise ship?

Anyway, my point was that there is NO “price reduction.” The SALES price of that house INCREASED $510,000 since its last sale. A reduction in ASKING price is meaningless. It’s an indicator of unrealistic sellers, rather than of a crashing house market.

SOL,

“So is the crash coming rapidly, or is it a cruise ship?”

Happy to elaborate. I can see how this confused you.

The answer is: Both.

The RE market moves like a cruise ship (Stock market is like a fighter jet, ups and downs daily). Once the RE sets a course, it stays there for a while (years).

It feels like the change in trend/housing story changed rapidly due to several reasons. Just look at this blog and how the conversations changed over the last month. We are now discussing if we already see price reductions (YoY) or just reductions in asking prices. Thats huge compared to what we discussed before and during summer! RE cheerleader no longer say its just zerohedge and its doom and gloom porn. Now, the news about a slowdown is reported everywhere. Not just in SoCal but also in other states and other countries!

As we see, the slowdown during summer (hot season) wasn’t expected by RE bulls. Also, many RE cheerleaders have disappeared from this blog or remain passive.

Maybe they are in shock over this rapid change or they are busy with open house after open house in order to still sell at a profit before its too late?

For me its not a buying opportunity. The market is way overpriced. Lets wait until next year for the market to adjust to further increasing mortgage rates and the trump tax changes. Its going to be an exciting journey for our RE ship.

“Lets wait until next year for the market to adjust to further increasing mortgage rates and the trump tax changes.”

He won’t say which market. He uses generalizations like “adjust” which doesn’t tell us much of anything.

You seem a bit hangry. What exactly is the issue? Did you bet on the market going up? You want all the details from me but who the heck are you and what’s your agenda or goal?

In terms of market specifics. It doesn’t really matter, everywhere you look the market is going down (Seattle, SF, Ventura, San Diego). There is not much you can do to change that. Let’s join the party instead of being so crumpy.