SoCal Correction: House prices fell in Los Angeles, Orange, and San Diego counties on a year-over-year basis, the first time in seven years.

The real estate correction is now showing up where it matters for the press, in home prices. Inventory has been growing and sales have been declining putting pressure on sellers. For the first time in seven years home prices have declined on a year-over-year basis in three important counties in SoCal: L.A., O.C., and San Diego. This will now put a pause on the FOMO rhetoric that if you don’t buy this year, prices will surge once again next year. Of course, more people are priced out of the California housing market because household incomes simply do not support current prices without aggressive mortgages or policies that artificially keep rates low. So now that the trend is shifting and the correction is here, how deep will this go?

Prices starting to meet reality

The market is definitely shifting so it will be interesting to see how the psychology shifts:

“(OC Regsiter) March’s price and sales declines occurred even though the economy remains strong and despite recent drops in mortgage rates, said Jordan Levine, a CAR senior economist.

Low mortgage rates may yet reignite demand during this year’s spring homebuying season, when sales typically are at their highest, he said. “It’s tough out there,†Levine said, “but there’s no reason (for sellers or their agents) to panic.â€

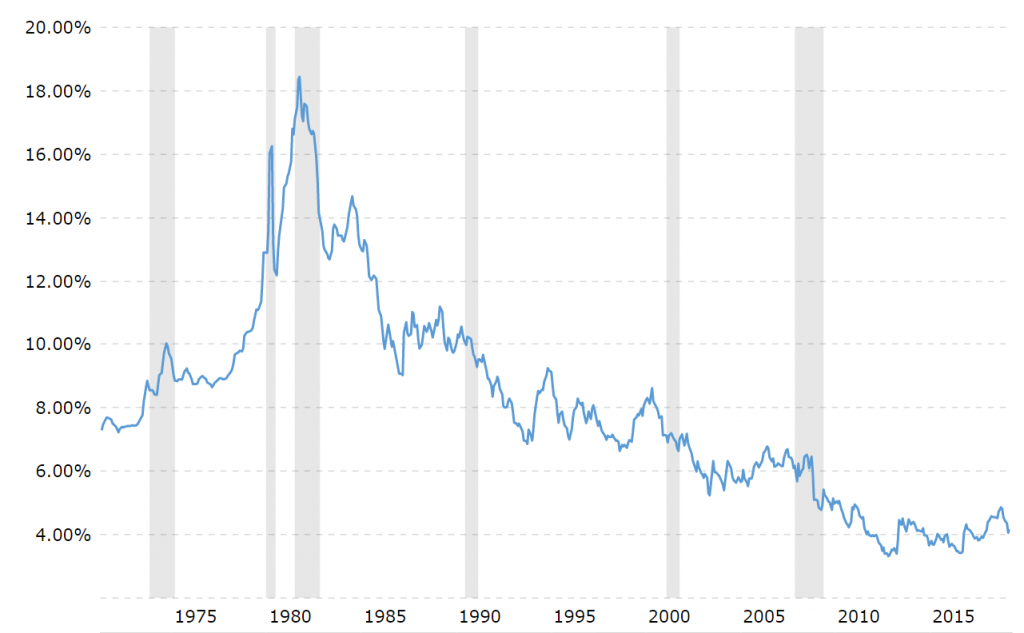

It is interesting how little is mentioned about prices tracking income gains or inflation as was the norm pre-housing bubble days (aka 2000 and before). There is now this dependency on the Federal Reserve in terms of engineering low interest rates. This is problematic because the Fed should use monetary policy to keep the economy healthy, not to keep a real estate bubble inflated. By the way, mortgage rates have been historically low for well over a decade now so we are already in “low†territory. Take a look at this chart tracking the rate of a 30-year fixed rate mortgage (the Adderall for the modern day home buyer):

From 2000 to 2010 the rate had a range between 5 and 6 percent. This is when the housing bubble grew to epic proportions. From 2010 to the present, rates are hovering between 3 and 4 percent. What you need to take away from the chart is that a low rate environment isn’t necessarily what is normal and looking at history, we are already near a record low level. Point being, I’m not sure how much low rates can do to reinvigorate the housing market when they are already very low.

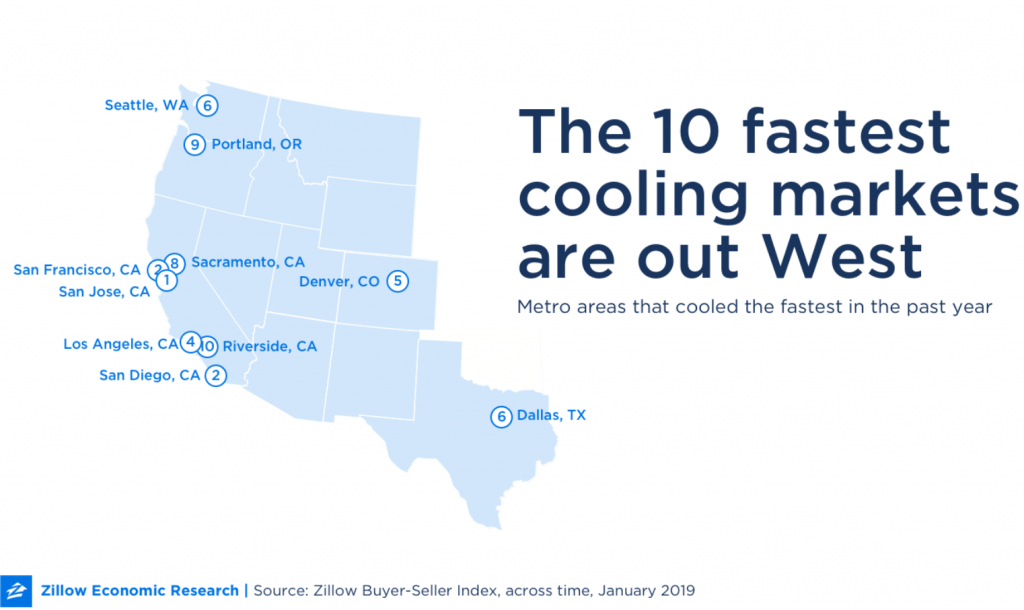

It should come as no surprise that the markets that are cooling down the fastest are in the west:

And most of the cooling areas are in California. All of this is expected. Things have gotten out of control. But with real estate the trend is your friend. The trend now is neutral to cold. And things just don’t turn around quickly in housing. So the question now becomes, how deep this correction will go? In California, there has been a major shift to renting households and many will vote accordingly. Even if Millennials do end up buying homes, so much of their after-tax income is going to go to paying the mortgage that there will be a hit to the economy in terms of where this disposable income would otherwise go instead of servicing a mega balance on a 30-year fixed rate mortgage.

California housing prices were due for a correction. Now that we have our first year-over-year decline in seven years, the question is how low will it go?

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Subscribe to feed

Subscribe to feed

222 Responses to “SoCal Correction: House prices fell in Los Angeles, Orange, and San Diego counties on a year-over-year basis, the first time in seven years.”

In Orange County, the homes are still moving….even out towards the IE, the prices in my realtor sent emails are small, insignificant reductions of 10k or so. And these homes still sell.

Yeah, you are probably right. Kind of seeing the same thing here. Bro-in law listed their place in Fullerton a month ago, sold in about 2 weeks with multiple interest. At this point, I think maybe only a nuclear or meteorite strike for house prices in SoCal to even have a chance go back to normal. Losing all hopes here, perhaps it’s pessimistic but do I honestly believe the system isn’t so rigged by the Fed that interest rate will never normalize? If it does, wait another 30 years?

I think it’s sad that most people on this forum (and most Americans in general) fail to see that the United States real estate market is trending towards markets in third world countries where the middle class has vanished. The overwhelming transfer of wealth and heavy influx of global money in RE in the last decade has decimated the middle class so this is the new norm like it or not. If you can afford it, buy, if not rent for the rest of your lives and have nothing to pass down to your heirs. Do you think serfs in the Middle Age were sitting on the sidelines waiting for property prices to come down? You can look at historical trends in the last 60 years thru a narrow lens or you can look thru a much broader lens and see what’s really going on here. 2009 was outright robbery by the wealthy elite and globalists, they got what they wanted it’s not happening again just lay it to rest and move on.

It’s a New Age people.

When the avg joe thinks that this time is different it’s usually a good indication that the peak has been reached. It’s in line with what I have been saying, downhill from now on. Get your cash ready 🙂

New age is right!

Of course there can be another black swan event (2008 financial crisis) but New Age is probably right….

sitting on the fence for 10 years, hoping for another crash is probably not going to pan out well for first time buyers. Like last crash, the investors will swoop in with all cash offers and then rent them out to the next generation of rentier class.

Looking at this graph over the past 30 yrs, there was only 1 major crash.

https://fred.stlouisfed.org/series/LXXRSA

Sitting on the sidelines and buying low is the best strategy. Many bought during the last crash. The RE market crashes every ten years. Never buy high and you will be okay.

“Real estate crashes every ten years”

Ladies and gentlemen I present to you complete disassociation from reality. When your real estate investment strategy is based on the arbitrary idea that the market is on a timer and will magically crash every decade then you will never achieve prosperity. Poor Millennial has been so psychologically traumatized by the Great Recession fire sale and all the wonderful once-in-a-lifetime opportunities that he missed out on. He’s probably sitting on the floor in a fluorescently lit room of a mental institution yelling at the top of his lungs “ANY MINUTE NOW!! 50%-70% OFF!!” as he frantically looks at his wristwatch. And when reality hits that it’s already been a decade since that fateful day, he’ll simply rewind his clock to 2016 and continue his maniac laughter. Let’s start a Go Fund Me for him guys. This is just too sad.

Most people know that economies go through cycles. It’s Econ 101.

2001 dot com bubble, 2008 housing bubble, 2019 everything bubble.

Roughly ten year cycles (plus minus a few years). Nothing goes up forever. If you don’t believe me, don’t waste your time here. Go out and buy 🙂

Millennial- you miss the point. Everybody knows the market goes through cycles. What I can’t understand is how you can bring yourself to say 50-70% off without providing any supporting rationale. I mean, 70% is way below 2012 levels here in the O.C. There would need to be an economic catastrophe, worse than 2009 in order for prices to come down to those levels. What do you specifically see happening that would cause such a devaluation of asset prices?

It’s not really a devaluation of assets. Housing will just come down to a realistic value. It’s highly overpriced at the moment and when the crash happens it corrects to the levels it should be. That’s what a bubble is, prices are disconnected from reality and when the bubble pops prices normalize.

Millennial — thank you for your response, but would you please help me understand what specifically would precipitate a 50-70% decline in prices?

Milli,

Real estate crashes every 18 years, give or take. Don’t mix up your asset classes.

i’ve lived here in Southern California all my life. In my own history of owning five homes is that every 7 to 10 years the price of my homes went up and then went down. Its been about 10 years of prices basically going up so based on many years of my own history i would bet prices will drop anytime soon. Does anyone really know what will happen?

La lost 13,000 people and OC gain only 6,000 people while Riverside gain 33,000 people. US census data, if LA and OC combined for a lots of 50,000 in the next few years see some houses and rent head down. LA is not the only place with population lost, New York City and Chicago.

I just sold my home 2 weeks ago in the IE , bidding war I sold 30k over asking. Housing crash 2019 this time for sure!

In my experience living here in southern California for many years prices go up and down about every seven to ten years. Bought in 1968 sold at the top in 1973, sold again on the upswing in 1978 and bought in La Habra, sold at the top or so in 1990 and bought in Chino Hills at the top. Saw value drop over $100,000 over next few years (33%). I was buying income property with 15% down in late 80’s when i should of not been buying at all as the market dropped and i lost around $5,000,000 of apartment buildings thru the early 90’s when rents dropped 33% or more. I believe houses began to go up in late 90’s then crashed huge in 2007. Its been 10 to 12 years now since housing prices have not went down. I dont know about charts and graphs but we should be seeing a drop in housing prices anytime soon just based on past experience. Does anyone really know?

Chinese hot money flow into residential and commercial real estate has slowed to 2012 levels. For domestic buyers the song remains the same …. prices will follow the availability of cheap affordable credit. When that constricts, look out below.

The “bright side” ( * cough * ) is that 10-year Treasury yields have no place to go but down, given the horrible state of consumer and governmental debt loads . The Fed is cornered into cutting …. again.

The Chinese money has slowed due to the trade war.

The trade war has not affected much here in China. Only 15% of china’s exports go to the US, and this has been compensated by adjusting the currency exchange rate. What Americans are seeing is the crackdown on corruption. It is hard to move illegally-gotten funds out of the country without calling attention to yourself, and bringing on an investigation. Xi told Party members to stop flaunting wealth. This caused an immediate dropoff in the business in Macau and other venues for living large.

Question for the more experienced landlords.

Would i be better having one high quality rental property or several cheaper ones?

How do you prefer your headaches, rarely or small and often?

Cromwell, I can answer your question based on 3 decades of having rental properties in all demographics; that and extensive research I did.

First, you have to keep in mind that the quality of your cash flow is as good as that of your tenants.

Second, the market is like a pyramid – more people are poor that rich. Those of the bottom are the most affected by globalization – salaries not keeping up with inflation while your cost to maintain these properties goes up with inflation or more (why more? That is another extensive subject).

Try to serve the solid middle class or upper middle class. I noticed that white collars keep the houses/units in better condition than blue collar. ALWAYS try to meet the tenants. Don’t leave up to property management companies because they will ruin them (they don’t care). Look at the tenants cars – not how expensive they are but how clean (inside and outside). If they don’t care about their personal property, they will care even less for your house. Watch out for those garbage cans on wheels!

Always try to have very nice properties, well maintained, with nice landscaping. It attracts a better demographics who actually pay the rent. With bad neighborhoods or properties, you get an attractive return just on paper not in reality – very high maintenance and legal cost (for evictions). When I was younger and inexperience I thought that I will never again buy rental properties. However, with experience and research, over the years I made excellent returns (better than I dreamed). Even today I am still acquiring properties if I can get 12% or better gross return on very low maintenance cost, or 10% or better net, after expenses. The property appreciation over time is just the icing on the cake. These properties are not easy to find, but I don’t have money all the time for the ones I do find.

In conclusion, better a very good one than ten bad ones. Better no headache than ten times the headache. Put yourself in the tenant shoes. Would you rent it? Why not? If you don’t like it, the good tenants are not going to like it. Would you like your wife or your girl to live in that neighborhood? You don’t want to compete on price but amenities and safety. Competing on price is a race to the bottom where the “quality” of the tenants gets worse and worse. I like being a landlord but I don’t like to be slumlord. Long term I think I make more money, too.

Flyover, where are you getting 10% net returns today on rental property? Maybe if you bought 10 years ago. Today you’re lucky to net 6-7% in Southern Ca. not including appreciation. Considering today’s interest rates 6% ain’t bad. I’d give my left arm for 10-12%.

Grasping, his question did no mention SoCal and I took the question as posted. I did not say anything about SoCal and I did not mention for him to invest in my state. I invest in multiple states, wherever I find what I am looking for. Currently, I don’t have anything in SoCal where I believe that it is a bubble. You are correct about the rental market in SoCal – you can not make the numbers work. For me, I do not care where my cash flow comes from if it is high and secure/quality.

I prefer higher end and not in California. We rented both times we lived in CA, 5 years in LA and 2 in Santa Clara. Both were dropping markets. In CA it is easy to find a very nice rental either apartment or house. In flyover states people look down on renters and often treat them poorly. As a result there is a shortage of very nice rental houses. We can be very picky because there is so little competition. There are many reasons to rent besides poor credit and irresponsible living. We often get executive types who move every few years. The ROI is much higher than CA. We sold our one CA rental a bit over a year ago as we wanted to get out within the bubble. We had made enough on the house to be happy. The amunt of paperwork and the hassles selling there were staggering. They “lost” the tax payment from closing and tried to double bill us for the $11k we paid. There were involved documents required at closing and luckily I have an excellent accountant who handled it all and chased down the lost tax money. It was not enough for us to prove we had paid at closing. CA it out of control

You are so correct Liz. I learned that through experience. I find people like doctors, pharmacists who can not find any place to rent and willing to pay a premium for a nice secure place (especially if they have children). Some of them are new in town, young, they have to pay down mountains of student loans, etc. Eventually they do buy their own homes, which is fine – new one are coming in. Meanwhile I do enjoy very high ROI with high quality income stream and no headache. Their income is so high that they are not forced to live paycheck to paycheck; they pay me in advance. Sometimes homeowners or business owners sell their expensive homes and it takes a year or two to build a new custom dream home. Meanwhile they pay me a year in advance with very high ROI. They don’t want to live in slum while they have hundreds of thousands or millions in the bank. Even with turnover, in four years my vacancy was zero even with the higher rent.

I’m not sure where you guys are investing, but currently I own rental property in S. CA. I have experience with the high-end rentals, mid-range, and low-end. The high-end has a large price tag to enter, is difficult to rent, properties often require high maintenance, and even though you make more money the ROI is usually less than the other two tiers because of costs. The low-end is where the highest ROI percentage is made, but also has the most headaches. You can make a lot of money as a slumlord in the less-than desirable areas of LA but be prepared for high turn-over, constant headaches, and legal fees including evictions. I have had more than one visit with the police at these type of rental properties. The mid-tier or working class neighborhoods are my preferred. These are the neighborhoods with a excess of service vans parked in the driveways. Plumbers, electricians, cable/telephone repairmen, etc. There you find hard-working people with recession proof steady jobs. I also focus on SFH’s vs condos. I find the HOA’s to be just another headache. I don’t see a lot of opportunity at the moment. Property prices are currently too high compared to rents. Maybe it’s possible in parts of Riverside County, but you’ll be lucky to net 5%. Maybe waiting until the next correction is best. IMO owning good rental property is the key to having a well-diversified portfolio and a steady stream of income in retirement.

Liz – From what I’m seeing in LA and San Diego County, most properties would be generating negative returns as rentals. From an investor prospective, housing prices would have to drop 25% before it made sense to buy.

Buyers are driven entirely by FOMO and the bigger sucker theory. Sellers are taking the money and running to neighboring states and driving up prices there as well.

You don’t want extremes. Low end = low end people with many problems. High end = probably not going to cash flow well and maintenance/repairs will me much higher than you think they will be. And harder to rent out, especially if there is a recession.

Find that middle sweet spot where the properties are nice in good neighborhoods, but not luxury. Rent to people who can afford to buy but choose not to, as opposed to people who want to buy but can’t.

And as always, you want the cheapest house in the most expensive neighborhood, NEVER the other way around. You also don’t want the $40K bathroom or $60K kitchen in your rentals. You want basic but nice. Remember, tenants will do damage to things. You want damage done to the $2/sq ft carpet not the $6/sq ft carpet, that sort of calculus. You don’t want the cheapest, but you don’t want anything too nice either.

I’ve been doing this a long time and know of what I speak.

You are correct on all points. I go through that every time I acquire a property.

Thank you all for the comments and advice. I have a low end property that I rent out and will be paid off in a few years. So wasn’t sure whether to buy second one or sell it and use deposit for a more expensive house.

March closings are contracts that were signed in February and January. Remember there’s typically a 30-45 day period between a house going under contract and a close. So March’s data is really telling you what the market was like in Jan/Feb. This was before the big drop in interest rates that occurred in March. The effects of that won’t be seen until the April and May closing data. If April and May see declines, then you’ll know this decline is real. But I have a feeling April and especially May numbers will disappoint most readers here.

“Big drop in ratesâ€

You know the market is in trouble when RE cheerleaders call a tiny rate decline a “big drop“. That’s what gives you hope the market is not tanking?

Landlords big drop: May 2018 4.55% versus 4.17% in April 2019.

Pathetic.

https://ycharts.com/indicators/30_year_mortgage_rate

Millie,

Mortgages were 5% in the fall/early winter and now they are 4%.

I know your generation learned “new math” and so it’s hard to understand. But the difference between a 5% mortgage and a 4% mortgage on $1M home is $700/mo. Still think that’s a “tiny” change?

Yes,your “big drop†in rates is totally pathetic. To even consider it and putting all your hope into a tiny rate drop shows how desperate you RE cheerleaders have become. Wake me up when rates are negative. That would save the market – maybe.

https://www.cnbc.com/2019/04/17/mortgage-purchase-applications-hit-highest-level-in-9-years.html

Considering how much of an impact these drops in interest rates are having on home buyers, I’d say perma-bears like Millie will be extremely disappointed.

perma Bear? I am a real estate bull – long term. Short term I am a realist. California’s housing cycle is about ten years. We are due for a big one. Wait and see. Your .5% drop in mortgage rates is not gonna save you.

Hi realist, my name is Delusional and I tripled my net worth since 2015 while you were crying wolf. All of the money I made is Monopoly money of course because obviously you just can’t win in this RE market.

Triple your net worth….Sure. Why is a mega wealthy multimillionaire on a housing bubble blog telling us now is a great time to buy? More likely you are a desperate house flipper or realtard getting nervous about the housing data during the hottest season (supposedly)? Looking at the data we see decreasing sales and increasing inventory. Not supposed to happen. Remember our economy is strong (low unemployment and strong stock market).

It feels like we’re at that point of the party, where the smart people have stopped drinking, because they’re (rightfully) concerned about how big the hangover will be tomorrow.

Sure, there’s still a few people shotgunning beers and downing vodka shots. You know those people who think the party will last forever, and they’re emotionally invested in ‘the moment.’ But the party always ends.

The longer and bigger the party, the worse the hangover will be, and the bigger the cleanup crew needed.

Good luck to everyone in the coming months and years, especially those who are still inebriated.

The club reopens tonight and as usual there will again be people lined up outside. Party on.

Speaking of people lining up……has anyone visited an open house lately? It’s like in that Netflix show black summer. After the zombie virus spread, foot traffic is dead. Nobody to see at open houses besides that poor realtor desperate to find the last sucker. He/she always get excited at first. When I start answering their question and sharing my knowledge about increased inventory YoY and muted demand they quickly notice: “snap, not someone I can sucker into buying at 50-70% overvalued asking pricesâ€

50%-70% overvalued?! Ok now you’re just messing with everyone on this forum. I get what you’re doing and I admire it: Get everyone to believe your BS and spread fear so you can snatch up RE for yourself. I think you’re smarter than most people give you credit for. Touche Millie

Spread fear? Not even close. The normal ten year correction in housing is just that: normal. Nothing to fear about unless you bought recently. But most people don’t care if they are underwater with a few hundred k. Most people don’t look at the financials or rental parity. You can’t have a housing bubble without dumb people who buy at the top. These people will never even research or make it to this blog. So, I don’t think your theory makes sense. I am simply a realist stating the facts. If you wait a couple more years you can buy half off. Nothing new or dramatic about it. Just the boom and bust cycle. Savvy people can even buy 70% off. Therefore, I am given the range of 50-70%.

New Age,

You’re new here so you lemme fill you in….our in house perma bear, Millenial (colloquially known as Millie) believes housing will fall by 70%. He’s been predicting this every year going back…I don’t even know how far to be honest.

Still not sure if he’s serious or trolling. In either case, he is entertaining.

Totally agree. 50-70% is the normal correction we will see within the next two years. The only point I disagree with is that I am not a housing bear. I am a real estate bull. But short term we will see a correction.

The Dr. referenced the year 2000 as pre-bubble prices. Extrapolating on that assumption, “normal” San Diego prices with a median home price of $276K in 2000 would be:

$483K @3% annual appreciation

$579.6K@4% annual appreciation

$698.3K@5% annual appreciation

Another point of comparison…building a home in CA will run @$250/SF for structure only, decent finishes. Then there are site costs, drawings and permits. General contractors told me if I waited until the market cooled, build costs may go down to the $200/SF range.

Those are pretty sobering statistics. Even 3% annual appreciation (which is very low for decent parts of socal) will make things very expensive over long periods of time. Also, mortgage rates in 2000 were 7% from the chart supplied by the Dr., they are 4% today.

20 years of price increases that match inflation and mortgage rates getting cut in half result in today’s 600K plus socal crap boxes. And this doesn’t account for population increase, supply and demand, onerous building codes, etc. We’ll see if Millie gets his 50 to 70% decline, I wouldn’t hold my breath!

A 50-70% decline in house prices is very conservative. It’s pretty much a given. The only question is when. As many experts predict, we will get a nice big crash within the next two years. Buy now and be screwed (financially) forever.

At least the ghettos are getting nicer because one day they will go up 30% more. Buy now before its hipsterized. Don’t mind the gang bangers.

Anyone looking to take exposure to home prices staying level, much less declining, might consider CME Case Shiller home price futures. Contracts can be traded for LA, San Diego, and San Fran. DM for details.

Zillow (aka RealTards online) just downgraded “Zestimates” in my neighborhood (Sacramento Eastern suburbs) by $50k/ 10%. Previously they were hawking “expected to increase 7.5% in the next year”. Now they’re saying a DECLINE of 5.6% lol.

2 houses on my street alone have been sitting on the market for over 4 months, with no bites and sellers refusing to lower price. Still in denial I see.

Its 2008 all over again. Some people never learn

Yep! The cycle ends again. What goes up comes down and what gets manipulated up crashes down. 50-70% price drops from the peak coming our way…mark my words.

You used to say 55-70% price drops. 55% was your minimum. Now you’ll be satisfied with 50%

It used to be 55-75% drop but we already had a 5% reduction in home prices. 50-70% is the target. With a 100% certainty.

What is the best website to use for information on real estate in the inlan empire? I am getting tired of Zillow, Redfin, and others all talking about the market is expected to increase 5% this year. blah blah blah

I am watching 4 homes I am interested in and all 4 have had price drops.

Doesn’t look like the RE shills get their red hot spring selling season they longed for. soon they tell us that the sales declines and negative YoY prices are “ seasonal ..:D

Ive Seen It All Before, it’s different this time. lmao, yup, yah gotta be pretty dumb.

https://www.youtube.com/watch?v=VQXzn-WCmy0&t=1172s

All the trolling aside…

Houses are sitting longer but they are still getting sold.

Most of them below asking price but not drastic, I am talking about 10k-20k at most for a house that’s in the 6-800k range.

There’s some posters here that keep showing Santa Monica homes as selling ABOVE asking price, using that as an example of how well the market is and its only going UP, UP, UP.

Let’s be real here, that’s distorted BS.

If I list a property below market knowing damn well its going to be in a “bidding war” and it sells above my asking, I guess you can use it as an example at how well the market is doing right?

– Market is slowing, some might even say its correcting

– Houses are sitting longer than usual

Wait for the reports for spring and summer to arrive then you’ll really have an accurate measure of the market due to spring/summer being the times people buy most.

… Buy now or forever be priced out …

oh and

… 50 to 70 percent correction COMING!!!…

did I get it all?

“ 50 to 70 percent correction COMING!!!…â€

Spot on!

I don’t think there will be a 50% crash. It is all about liquidity and there is still a lot of it.

My house I have lived in has only appreciated from 185k to 295k in 19 years. 4 bedroom, 3200sq ft. That is 2.49% yoy appreciation which is not even keeping up with inflation. I live subdivision that has a grade school school that kids walk to, the school district is very good, and lots of shopping and restaurants. Unemployment in this city is 2.6%.

No way my house drops 50%.

Liquidity dries up during a crash. No, your house probably doesn’t…..where do you live? in Idaho? In California, there will be a 50-70% (coastal area). Just like every time the market turns after a steep run up.

As much as I’d love to see a 50% correction in SoCal, I’m not holding my breath. Sure, you may see that in the less desirable areas but no way there will be that big of a correction in desirable areas. At peak-Great Recession in SW Pasadena I saw prices correct 10% one year and they were back to where they were pre-recession by the following year. Riverside was a totally different story tho. Prices there corrected 50% and you could pick up a decent short sale for low-200s, but that’s because far fewer people are willing to buy a life of misery commuting on the 91.

Well I am not seeing prices drop in the nicer parts of downtown and midtown Sacramento! I see asking prices selling for 700k plus for crappy old 2 bedroom homes.

Zillow and Redfin are bombarding me with price drops and new listings. Have you entered a search on those websites so they send you updates frequently?

I am not in Sacramento but have seen price drops across the board in my area. Also, foot traffic has been dead at open houses….must be seasonal or due to weather. Or maybe people had to prepare for Easter for the last two month and couldn’t make it out to an open house.

Used to live in Sacraghetto. $700K for a crappy old two bedroom in Midtown with all the homeless hordes defecating on the streets?

It must be the over paid Democrat socialist politicians and state workers who pay those ridiculous prices!

It is interesting how things will evolve in the next few months – the strongest selling season of the year. Meanwhile this is the report so far for the last 13 months (all four seasons, good and bad):

https://www.zerohedge.com/news/2019-04-22/us-existing-home-sales-slump-13th-straight-month

Seen It All Before and still to dumb to see it coming again!

Existing-Home Sales Slide 4.9% in March

https://www.nar.realtor/newsroom/existing-home-sales-slide-4-9-in-march

This Santa Monica house sold for $51k over asking: https://www.redfin.com/CA/Santa-Monica/1717-Robson-Ave-90405/home/6776071

* 1 bath

* 1,028 sq ft house

* 5,100 sq ft lot

* In Sunset Park (i.e., not one of Santa Monica’s better areas).

Thanks to OrangeManBad, we have a once in a lifetime economy right now. Unemployment and mortgage rates at 4%, with GDP growth at 3%. It doesn’t get any better than that. Literally, we have never had this perfect economy before.

And yet people are talking about a housing crash?

LOL

Yes, strong economy. the tech company I work for had a record year and very strong Q1. I have never gotten such a high bonus and salary increase before. And no slow down in sight. Yet, the housing market shows signs of weakness. During the last few years you had Asian cash buyers who have disappeared now. You also had changes in tax laws (unfavorable to home owners in blue states). Also, we don’t see millennials buying in droves (must be the $200 avocado toasts). Most importantly, you have a big change in buyers sentiment. Ask anybody if housing is currently overvalued and if it’s a good time to buy. Most people will tell you it’s the worst time in history to buy and that housing is massively overvalued. You can easily see it by comparing rents to PITI. Rents are a bargain compared to buying simply because the base (house price) is overvalued by 50-70%. They are building everywhere. Boomers are dying/retiring and millennials aren’t buying. With so much supply coming online while having muted demand at the same time it’s not hard to see what the future will bring for the RE market.

They listed the property 49-55k below market and got what the house is worth now.

If I listed a home for one dollar and it sells for one million, I guess it was sold for 999.99k OVER ASKING too yes?

And by me getting over asking price the market must be in good shape huh?

@ SOL

Over $1500 square foot is nuts…..that house sold in a couple weeks…and on a busy cut-thru street too. Tiny lot with a tinier house. Not a lot of upside. That was a crap buy for some poor buyer…the seller is chuckling all the way to the bank.

On another note: Why oh WHY are home sellers paying 5-6% for realtors fees???? Is there any good alternative? Put these hucksters out of business. 90% of RE agents are absolutely USELESS. Cant believe there is not a riot over the amount of money they are making for no work!

About that housing crash……

“A sprawling waterfront estate that served as an art collector’s paradise has sold in Hunts Point for $37.5 million, smashing the record for the most expensive home sale in the Seattle area. The sale of the mansion and grounds that span 3.27 acres at 4053 Hunts Point Road surpasses a $26.75 million estate that sold in Medina last year, which had been the priciest home sold and recorded by the Northwest Multiple Listing Service across Western Washington.”

Right now in California, year over year we have double digit inventory increases, double digit sales declines, and negative prices. What is a housing crash suppose to look like?

I could list foreclosures and say the market has crashed, based on your post as an example of over all market opinion. smh

Ive Seen It All Before, but i’m to dumb to admit it.

Just like in 2018 we were told by our RE cheerleaders how this will be the hottest spring season. Instead, the market hit a wall in 2018. Doesn’t look much better for 2019 despite the monster, mega drop of mortgage rates (.5%) which causes our cheerleaders to get wet.

Some data:

https://wolfstreet.com/2019/04/22/lower-mortgage-rates-no-relief-for-us-home-sales/

One metric I would be interested in, would be to see the fall in housing prices by price point. Basically low, mid range, and high end. The wealthier areas seem to be doing very well and homes are still being torn down to build ever larger mansions.

In fact, the only weak sector of the higher end property market, seems to be retail space. Might be time to rethink several retail areas and turn them into housing space.

“Might be time to rethink several retail areas and turn them into housing space.”

Who amongst us hasn’t wished it were possible to live in an abandoned mall?

The high end is doing terrible. There is over a year of supply of houses valued at over 1 million.

March new home sales up 4.5% in March

My goodness this is worse than 2008, amirite?

LOL

New home sales in March are reflective of March ultra low mortgage rates, that pre-existing sales in March are not reflecting yet, since those sales went under contract in January and February.

You misinterpret current rates as “ultra lowâ€. If a house is priced at 1mio but is only worth about 300-350k your 4% interest is not ultra low. Sure, if you compare it to 15% interest rates from the 80’s a simple mind would think it appears low. But that same house only cost maybe 80-120k back in the 80’s. The base (house price) is what matters if you talk about percentages. With highly inflated house prices even a minus 1% interest rate is still too high.

It’s always better to buy a correctly priced home with higher interest rate instead of buying at highly inflated prices with a low-looking interest rate. You can always refinance later. But The house price you paid and the associated property taxes can not be changed. If you buy high you are screwed forever unless you walk away and eat the down payment you invested.

New homes sales data has been terrible the last 1.5 years. A tiny spike that gets revised later isnt really a good reason to unpack the cheerleader gear.

Smart money has begun the dump.

That’s what I think I see too! At this point anybody who is jumping in are simpletons, who will be left sitting in underwater mortgages and complaining it is “unfair” the got duped again.

A lot of pointless discussion about this and that house going over asking or current stock market going up. Whether or not to buy the home you live in is a long-term financial decision that should be driven by your long-term outlook for the economy and real estate market. That outlook is not good right now considering demographics and overall economic climate.

The stock market will be in deep doodoo by end of 2020 – one way or the other:

https://www.theguardian.com/business/2019/apr/23/us-stock-market-boom-us-china-brexit (good short article by NYU professor that sums up the risks):

“…while investors’ latest love affair with equity markets may continue this year, it will remain a fickle and volatile relationship. Any number of disappointments could trigger another risk-off and, possibly, a sharp market correction. The question is not whether it will happen, but when.”

The housing market, that is already on shaky ground in this “hot” economy, will then go off the cliff. This has been my point of view for a while.

The Fed should have never re-inflated the bubble after the last crash. It did and the reckoning will be historic. If you don’t own, I would not touch real estate now, considering the downside risk is huge and upside potential is minimal. If you own, I would try to cash out.

Last point, I always try to see what rich people are doing with their assets as a group, since they get good financial advice. As I drive through most expensive zip codes in San Diego , I see unusually high number of “for sale” signs. Why is that?

“The stock market will be in deep doodoo by end of 2020”

If Bernie or Kamala win the presidency, I agree.

My budding is listing his house that he bought 2 years ago in San Diego (he’s moving out to state for work). He’s going to be selling for at least 7% below what he had to pay 2 years ago. He’s in a decent, but not great area.

My impression is that houses in high demand areas that always command a premium regardless of what the market is doing are still selling although at less of an increase in price while areas that people had to buy in for affordability reasons are starting to have issues.

I’d rather wait since my rent is so affordable. No need to buy into a market that’s so overprice.

Even with the low interest, I see increase inventory, housing price reduces, and longer to sell. I’m not talking about highly desirable area (Santa Monica). Whoever want to buy in this climate know full well what they got them self into. Good luck!

Same here. My rent is an absolute joke. So freakin cheap. Yet, we hear every month from our RE cheerleaders how rents are skyrocketing. I had to laugh hard when some joker posted what rents are currently – supposedly. That made my day. Btw, if my rent would somehow triple over night I would just move back to mom and pops. There is always a strategy to win during a bubble. Best thing: save cash and buy low. Worst thing: buy sky high.

Oh Millie,

Stop pretending the rent is cheap. I have a friend moving to Los Angeles next month. They want to live where I lived in 2002 when I moved here. I looked up the price my old non-updated 2 bedroom in Hollywood. It rents for $3000 a month…. back in 2006 when I moved out it rented for $1450. Stop lying that rents haven’t gone up to absurd amounts.

Thank you for confirming how freakin cheap my rent is!!!!!!!!!

He pays 3k for 2bedroom? Holy smokes, I am paying less than half. Must be the deal of a century. I don’t live in LA though….which I call the armpit of America. I live 10-12 min from the beach depending on traffic and work at a tech company (well over 100k plus bonus), commute is around 20-25 depending on traffic. I am not gonna tell you exactly where otherwise you all move here.

Now, imagine I would be paying 3k a month for a 2 bedroom, do you think I would run around and tell people how cheap rents are? Fooling myself? How’s does that make any sense? If I would be paying 3k for an apartment I would be living my parents or in-laws for free. I always love when people post these numbers. Makes my day. Why walk away from the gift my landlord is giving me 🙂 thank you!

3k a month or for two month? For 3k a month you could rent a nice 5bedroom house in my neck of the woods. Sounds like I am not moving anywhere for a while. Renting for much less, which makes me a happy renter! If market corrects I may buy though.

I think you’re the type of guy that just spews whatever comes to mind without checking facts. Here are some facts: Back in 2002 when I moved to a town called Pleasant Hill in the East Bay Area we were paying $950 p/month for a 1 bdrm town house. That same place is now just north of $2100 p/month. That same $2100 is just shy of our mortgage payment for our house we bought 3 years ago not to far from our old apartment.

I bet you get cheap ass rent because your landlady feels sorry for your wife having to deal with your delusional beliefs we are approaching a 70% housing crash. She’s actually a genius. Keep giving Millie below market rent and let him believe he’s “winning”. He’ll pay off my house for me and I can retire with a fat bankroll….THANKS MILLIE!

You nailed it! I am getting below market rent prices and call this winning! Can’t lose by saving a ton each pay period and buying when the market crashes! I can do this for a long time.

SumTinWong, I question whether Millie has a wife. Or even rents.

I’m starting to think he’s a real estate mogul who comes here to f**k with people and have a little fun.

Everything I stated is true. Beautiful wife, well over 100k income and my wife works as well. Dirt cheap rent. Renting in a low income / bad school district. You gotta love bad school districts. Rents don’t go up and I don’t go to school :).

Just waiting for a nice collapse in the economy to buy my first house at a 50-70% discount. I am really surprised not more people have the same strategy that saves you several 100k. If you buy high you can never catch up to someone like me who saved in good times and invests in bad times. To me this is the only strategy that works and I can’t wrap my head around how so many people want to buy at highly inflated values. I guess it’s herd mentality / drive through mentality. You want everything now and can’t wait for buying opportunities. That’s why we had 7 Mio foreclosures last time.

You live in OC and get $1450 a month rent?? No way now you are just full of it. Even the worst parts of Orange county don’t get you that kind of rent no matter how nice your landlord is.

I just signed a 2 year lease. Dirt cheap. Prices will come down and I will buy with everything I got.

Respectfully, Mr Landlord, I think you are the Real Estate Baron with an undeserved Yuuge ego who has already disappeared once when the market crashed when your Yuuge investments in Amazon stock tanked 70%. It is hard for you to be wrong. You will disappear again if the market crashes 70% again.

Our Millennial is our vocal hero fighting for his people (who most can’t post because they are too busy working 2 full-time jobs to pay the rent and will likely launch Bernie into the White House in 2020).

IMHO, Bush and the Republicans crashed the economy in 2007 and left behind may of the people living in RV’s or in tents today. Obama promised “Hope and Change” and delivered it to homeowners and equities holders from the Great Republican Disaster. However, the homeless, and RV crowd were left behind. Trump promised MAGA (Ala the 1950’s and 1960’s where government projects like SS, Medicare, infrastructure building, (and a 90% tax rate on the wealthy were expanded)). However, he is a typical Republican and has cut these programs. The left-behind people now recognize Trump and the Republicans on who they are and will vote for Bernie in 2020.

If the FED is truly not political, they will raise rates again soon. The stock market and housing will drop 10%. Ideally, the Fed is trying to hold asset price inflation to the inflation of wages, food and other commodities. If they are political, they will follow the Republican leadership and let stocks and housing blow up just like they did under the Bush disaster.

If this is the case, Our Millennial will be the greatest prophet in history, and you will disappear again.

Our Millennial is our vocal hero fighting for his people (who most can’t post because they are too busy working 2 full-time jobs to pay the rent and will likely launch Bernie into the White House in 2020).

___

I thought Millie made $100K+. Now he has to work 80 hours a week just to make the rent?

LOL

We are in the midst of the greatest economy of our lifetimes and people like you are acting like it’s 1933. Give it a rest dude. If you’re not making bucketfuls of money in 2019, the problem is you, not Trump or any other imaginary boogeyman losers like Bernie or AOC is pushing. Give off your azz, move out of mommy’s basement and go make some money.

New age, my rent is actually less than 1450. Also, I don’t think I gave away where I am located. Usually, when realtors ask me at open houses about my rent I don’t disclose it either. They wouldn’t believe me. I still pay way more than someone who lives at home with mom and pops. I would do that in a heartbeat if my in laws or parents would live closer to my tech job.

At my level, you don’t need to work OT anymore (only during month end). I am salary based and don’t get Paid OT. Most weeks I work a little less than 40 hours and 1-2 days remotely. Well over 100k, bonus, free snacks, and fantastic benefits. Love my job. If I would work more I had less time to study the RE market, post here and visit open houses.

Apropos Open houses. It’s dead on the weekends…just me and a realtor. Poor realtors try everything to lure people in. “You can win a 100 dollars gift cardâ€, “free Hot Dogs and sodasâ€. Buyers sentiment has changed. People don’t fear of missing out or being priced out forever…..no, people fear of catching the falling knife if they buy now. The market is turning. I give it a couple more years.

Bob, there was NO difference in the economic policies of Clinton, Bush and Obama.

Bush sent Wall Street a bailout package in 2008. And when that wasn’t enough, Obama sent Wall Street another bailout package in 2009.

Clinton’s economic boom ended when the Dotcom Bubble burst. Bush’s economic boom ended when the Real Estate Bubble burst.

===========

Mr. Landlord, the U.S. economy has been running on smoke & mirrors for many decades now. Whether under Democrats or Republicans, we borrow, borrow, borrow. We borrow to boost consumer spending. We borrow to buy mo’ free stuff for citizens and illegals. We borrow for war and empire.

Our economic booms have been debt driven for decades. The national debt (don’t confuse that with the deficit) is ballooning to catastrophic proportions. It will in time tank the economy, regardless of who’s in charge.

Trump’s increased military spending is making matters worse. Especially if Israel pushes us into a war with Iran. And Bernie and AOC’s promises of mo’ free stuff for all — illegals too — will make matters still worse.

You say it’s not 1933? True. But the Great Depression was preceded by the Roaring Twenties.

New homes are selling when you cut the prices.

https://wolfstreet.com/2019/04/23/new-house-sales-cut-the-price-and-they-will-come/

Amazing…..who would have thought that you can sell more when you cut prices?

It’s like with Tesla. Why buy now if you can buy a Tesla 6 month later for several thousands less? Or, Why buy a house now if you can just wait and save 400k when buying the same house in two years?

I’m a long time reader but first time poster on this site, and this is how I view the current state of things:

I remember 2006 to 2008 extremely vividly, as they were the best and worst financial years of my young adult life. At the end of 2006, I was making between 11-13K a month online generating mortgage leads. This was in addition to a government job that I had with a public utility, not a great salary but my healthcare expenses were essentially paid for my family plus I was enrolled in the public retirement system. We had just bought a house in June of 2006; a 1776 square foot home on a 10,000 acre lot in the hills above Lake Elsinore, CA (Inland Empire) for 400K. We had new cars, new toys, went out to eat all the time… not a bad life for a 22 year old with a new family. Everything was great!

Until it wasn’t.

In July of 2007 I got laid off from my full time job. I was lucky to find another one fairly quickly, but by then my online mortgage lead income had started to dry up. The new job wasn’t nearly enough to support the lifestyle we had borrowed our way into. We ended up having to file for bankruptcy in 2008 and we lost pretty much everything. The implications from all that lingered into at least 2012 as we struggled to pick up the pieces from the mistakes that we had made.

I’m telling that story because things today feel eerily similar to how things were back in the end of 2006; stocks at all time highs, housing at all time highs, employment at all time highs… but fortunately this time we are in a much different financial situation and on our way to being 100% debt free in about 12 months, the majority of that being student loans. I see friends and family today making the same types of mistakes that we made back then when it comes to massive debt for houses and other things like new cars, vacations, etc. I know on the surface right now, everything seems great and everything will just up, up up… but that just isn’t sustainable long term.

The reality is, at this point something just has to crack the foundation of the last 8-9 years hard enough that things start to crumble. When (not if) that does happen, I believe it will happen very quickly just as it did in years past. While I’m not as optimistic as Millennial that there will be a 50-70% crash, I do think 30-50% is a real possibility especially in overvalued markets.

I remember looking at homes in 2006, when everyone was saying the same things they are saying now – Real estate only goes up, buy now or be priced out forever, etc… I have to remind myself of how quickly things turned around last time from being fantastic in June of 2007 to being absolutely horrific just a few short months later.

By the way, that 400K house in 2007 sold for 200K in 2009.

Great, helpful post! Thank you DebtfreeIE!

Thanks for sharing! I agree with you, except I don’t think the situation is similar to 2008. I actually think the situation in 2018 is a continuation of the 2008 mess that never got resolved. Bottom line: too much unchecked risk taking in the financial markets leading to over inflated assets. The reason – the Fed is not doing what is good for people, the Fed is doing what is good for the ruling class and the bankers, who will be able to pull the money out before all these bubbles blow up again and/or will demand/lobby that the tax payers bail them out. In 2008 it was messing with mortgage backed securities, in 2018 it is investing in tech unicorns that never made a dime.

I’m sorry you had to go thru that experience but it sounds like you have recovered since then and doing really well. I do, respectfully, disagree with one of your points. You mentioned that you bought your house for $400K in 2006. Adjusting for inflation that would be equivalent to buying a house for $512K today. Let’s take a look at this listing:

https://www.redfin.com/CA/Lake-Elsinore/4111-Cottonwood-Cir-92530/home/6671531

Almost double the house for $350K (of today’s money) in Lake Elsinore. I’m sure your house was shinier and had a better view and maybe even had a pool but you cannot say that this era of home-buying is anywhere close to where it was in 2006. We’re talking about $288/SF (inflation adjusted) vs. $113/SF of today. We’re not even on the same logarithmic scale here. I understand areas like SD, OC, LA, SF are reminiscent of 2006 and I agree but even those areas have cold hard cash flowing in not the over-leveraged credit that 2006 brought us. I’m not saying right now is the BEST time to buy, but at the same it’s still REALLY GOOD. Could there be a correction? Sure maybe 20% at most during some apocalyptic event but I expect stagnation for a few more years at best.

@New Age – That listing is a short sale… not a good sign if what we have experienced since last summer continues. Inventory in that area is up over 100% YoY and days on market is up almost 300% YoY. You are correct though that adjusted for inflation, prices aren’t quite what they were in that area but in many other IE cities they have passed their previous peaks.

I don’t spend a lot of time looking at listings, but I don’t remember seeing a lot of short sales over the last few years. When we bought in 2006, it was pretty much near the market peak. When things started to go south in 2007, we tried to get out by selling the house but by that time prices had already started to go down. Our realtor at the time mentioned that we could possibly do a “short sale”, something that was relatively unheard of until the 2000 era housing bubble started to pop. He said the last time he had done one was in the early 90’s during the recession that followed the housing bubble of the late 80’s.

Like I said, things feel eerily similar to the end of the last bubble. It’s pretty much just a waiting game to see how things play out this time.

@DebtFreeIE

You mentioned that many IE cities have passed the peak. I will challenge that and go as far as saying that not a single IE city is even 2/3 there (inflation adjusted). I’m looking at numbers and they simply don’t agree. Negating the fact that the house I provided in my example is a short sale, the average $/SF is still $185 which would’ve priced your 2006 house somewhere around $320K which is FAR BELOW the price you purchased your home at the time. Also, you mentioned that inventory has doubled and days on market has quadrupled, I’m going to challenge that claim as well. Do you have a source?

If it feels like 2006 to you, you might want to turn the AC down because those chills are definitely not due to the housing market. We in a completely different solar system to 2006, we shouldn’t even be saying “2006” it’s completely irrelevant to the housing market of today. People fail to see how speculative that market was and how astronomical prices have grown in such a little period of time. That is simply not the case here.

I have been reading this blog for some time and could not help make this comment. Been priced out since 2015, currently paying more for an apartment, than what a house would cost to rent. But I will be damned if I pay someone else’s mortgage, or be someone’s investment property bag holder. Good luck to all!!

Just say you love your apartment and are waiting for better housing deals that’s a better reason. You think there is no mortgage on that apartment you rent? If there isn’t, you think you aren’t subsiding someone’s retirement? lol True, don’t be a bag holder but your logic is off.

I feel very sorry for you. Maybe switch apartments? My apartment costs 1300. If I were to buy it with 20% down I would still pay over 2000 per month. Renting is very cheap compared to buying. Plus your landlord takes care of everything. Imagine you buy and have to fix the roof on top of everything else you are paying when you purchase a property. If I were to buy a house, my mortgage would be like 3000 if you want basics like a front door and windows.. Why should I make myself housepoor. If I want to live in a house I could just move back to my parents.

So you are renting an apartment and you don’t think you are paying somebody elses mortgage or finances their vacations, luxury cars, etc. This is a big reason people finally throw in the towel and end up buying. Being at the whims of a landlord in places like socal sucks big time. Just be sure not to be a long term renter, this is a recipe for financial disaster in socal.

I was trying to make the point that in comparison to buying the rents are very low. There isn’t really a financial reason to buying if your landlord lets you live There for half the cost. Buying is basically renting from the banks. I rather save my money and give it to a privat landlord. If that lets my landlord drive a lambo and I save a significant of money each month than I don’t know what’s not to like?

Lord blankmind, who cares if a renter pays someone’s mortgage, someone’s vacations or luxury cars? The only thing I care about is rental parity. If I have to lock up 20% plus pay thousands more per month why wouldn’t I take a deal and rent instead, save money and wait for a nice collapse? If buying would make financial sense we wouldn’t need RE shills and RE cheerleaders. We would have bought already. But because house prices are massively overpriced and disconnected from fundamentals we are having these fun discussions.

Dude, are people really that silly?!!

What’s worse?!?

Paying your landlords mortgage and living in the same house / condo that would cost you $$$$ more to purchase ……OR

Buying and making your realtor, lender and SELLER rich? Some peeps haven’t heard of being house poor yet?!!

Obviously there is a cost of living. Don’t think you come out ahead just because you signed some papers that benefit everybody else.

As low as rents are compared to the cost of buying now in SoCal, I don’t think my rent would even be covering interest, taxes, and maintenance of somebody who bought the property at current prices via traditional 20% down/financing the rest deal. So no, I don’t feel like I am paying for somebody’s vacation and luxury car. I rent a 5 bedroom house over 3,000 s.f in one the best school districts in San Diego for $3,500 per month. The Zestimate on it is over a million. I would consider buying it at $750K or below. The only reason the rent is making sense to my landlord is because he bought before 2000, when prices were attached to reality.

Prices for Westside condos have been pretty chaotic in the last couple of months. Some examples:

Sold for $62K under ask: https://www.redfin.com/CA/Los-Angeles/1722-Malcolm-Ave-90024/unit-401/home/6803912

Sold for $10K under ask: https://www.redfin.com/CA/Los-Angeles/1539-Greenfield-Ave-90025/unit-301/home/6802463

Yet this place sold for $137K over ask: https://www.redfin.com/CA/Los-Angeles/1742-S-Bentley-Ave-90025/unit-302/home/6801614

Granted the place is really nice inside, but it’s just at the 1000 foot distance from the 405 and the street is narrow and full of ugly, old apartments. The unit has a “shared” rooftop patio that is just inviting trouble if a neighbor turns the place into an AirBnB.

This last condo is a sad example of an overpriced unit walking down the price to find a buyer. It’s close to the last selling price now. Witness the “Game of Thrones” condo.: https://www.zillow.com/homedetails/10640-Wilkins-Ave-APT-204-Los-Angeles-CA-90024/20506682_zpid/

They’ve been trying to sell it since April of last year and have gone through at least two realtors. It’s a nice street, but the place is just… off. Who has a sauna in their bathroom?

This one you referenced is funny:

https://www.redfin.com/CA/Los-Angeles/1742-S-Bentley-Ave-90025/unit-302/home/6801614

Who pays 500 a month for HOA’s? This place was built 79. Instead of 1mio it is probably worth around 290k if the HOA’s were around 43 bucks.

For my Santa Monica condo, I pay over $1,000 a month in HOA fees. And I’m in one of the small units — 1 bed/1 bath. Some of the bigger units pay over $1,500 a month.

But those HOA fees include 24/7 doormen, cable TV, WiFi internet, electricity, water, and earthquake insurance. Also a community pool and sauna that I never use.

The doormen are convenient. I can travel for long periods (once was gone for 6 months) and not worry about burglars.

That condo was sold for $294K in 1999.

I should have bought it then.

Crazy, I tell ya!

1k HOA, congratulations! Looks like you hit the jackpot! But hey, you are in a secure location. Like a panic room. Not like us normal people who get robbed twice a week. Not.

I agree Bob, less than 300k seems like a fair price (if HOA’s would be less than 50 bucks). There are really nice houses in my area for 800-1mio. I could see myself making offer during the next crash within the 400-500’s range.

Uh, most people actually. You must not live in California.

$500 HOA is not unusual for West LA/Westwood. Take a look at this 55 year old condo:

https://www.redfin.com/CA/Los-Angeles/10701-Wilshire-Blvd-90024/unit-404/home/6825578

4th floor on an 11-12 floor building… if a unit in your stack above you has a water break, it will become your problem, too.

@JR – the kitchen would give a hippie acid flashbacks!

Just because other dummies overpay for HOA’s doesn’t make it better. It’s totally retarded to throw your money away like that.

Legally and practically, nobody is making money off HOA fees.

The HOA homeowners associations have to account for every dollar spent. and HOA board members are generally unpaid.

If you have high HOA fees, you typically have luxurious benefits to living there (deluxe pools, fitness centers, doormen, security, etc). These all cost money. If you don’t need luxury don’t live there.

Medium HOAs typically cover gardening, lawn mowing, roof replacement, outside painting, etc. Stuff either a homeowner would have to do or hire someone at a higher price to do.

Personally, I’d look into where the HOA money is going. If you see high legal fees, run away, or find out why.

Given that, I am on an HOA board and we charge $50/year in HOA fees. Most of that goes to a householder BBQ once per year. The rest covers things like maintaining the signage for the neighborhood.

In the past I have lived in places with $1,000+ HOA’s. The fee included 24/7 security and doormen among other amenities. If this is something you desire, then you must pay for it.

The kitchen in the game of thrones house is…interesting? I’d bet it scares off quite a few people.

Game of Thrones kitchen? That’s nothing!

Check out this Game of Thrones HOUSE: https://www.redfin.com/CA/Woodland-Hills/4984-Topanga-Canyon-Blvd-91364/home/4205295

The game of thrones house looks kinda cool! Def. interesting. 1.3mio seems overpriced for 1300 sqft and the location. I could see myself making a 500k all cash offer.

Son of a Landlord, that is a very cool house. Someone spent a lot of money on the interior finishing, hardwood, stone arches, stone fireplace, built-ins, solid wood beams, …. Very awesome.

The $973 per sq foot makes it a little pricey for the neighborhood. With a castle wall, and a moat, on 1000 acres, I would snap it up. Maybe Our Millennial could be one of my serfs? 🙂

It sold at the last bubble peak for $924K which means it is up 41% from the last peak. Either this bubble is more outrageous than the last bubble or a lot of improvements have been done. No idea if it looked like a cool castle back then.

It was built in 1952 and sold in 1999 for $207K. $207K was typical 1950’s/60’s tract house pricing back then so I doubt it had finishes back then.

Ive Seen It All Before, and im to dumb to admit it.

America’s Hottest Housing Markets See Biggest Sale Declines

https://www.zerohedge.com/news/2019-04-23/americas-hottest-housing-markets-see-biggest-sale-declines

Housing is not yet crashing.

This one sold for $80K over asking in NoHo NoHo in my opinion is Van Nuys with a boob job.

https://www.zillow.com/homedetails/5825-Morella-Ave-Valley-Village-CA-91607/20012989_zpid/

“NoHo in my opinion is Van Nuys with a boob job.” ………..So true.

Sounds like this is the year millennials go out and buy in droves. Not!

http://www.bloomberg.com/amp/news/articles/2019-02-25/millennials-face-1-trillion-debt-as-student-loans-pile-up

Heartache for the perma bears this morning.

GDP Growth up 3.2%.

So much for you fantasies of a housing crash and a recession.

Thank you PDT!

Mr. L, I have to agree with you. Stock market hitting all time highs, GDP over 3%, unemployment at record lows, all means no correction/recession in the immediate future. In fact I know many people who are sitting on piles of cash looking to buy rental property for a passive income stream. Furthermore in response to rents, I raise prices every year on my S. Cali rentals and am currently receiving my highest rents ever with zero vacancies.

@Grasping at Straws,

I agree….everyone is looking for a way buy properties for cash flow…super hard to do as a small investor as all the major companies are scooping up income properties. I can’t quite figure out how they are making money, but I guess their time frame for returns is in the 7-10 year range.

You gave yourself the answer. The economy is supposed to be strong, yet the housing market is going down: higher supply and lower sales. How do you reconcile this? Are you still saying it’s seasonal 😀

Take a look to 2007 and you will see striking similarities.

I hate to burst your bubble Millennial, but the increased inventory is all in the high end. Median home prices up to 700K in LA are still going under contract quickly with little to no inventory. The junk that sits on the market for 90+ days is the same junk that will sit under any market conditions. I will agree that appreciation has slowed across the board and the days of buyers asking for the moon and getting it on mediocre properties are over. There seems to be a abundance of $1 million+ properties available in LA compared to the medium & lower end. Is this a sign of things to come across the whole spectrum of the RE market? Maybe, but we will have to wait and see. With current mortgage rates hovering around 4% it’s still near historic lows. For now the music keeps playing and the dance goes on.

Grasping,

No reason to burst any bubbles just take a look at the data. LA, OC and SanDiego have negative prints YoY. Remember our economy is strong at the moment. It’s 2006 all over again. You can tell yourself all day that this time is different or you can prepare yourself, follow the data and set yourself up to make some big money when the crash happens. Your choice.

It’s cute when people try driving through the rearview mirror.

As if there have never been economic recessions/depressions whereby various asset classes depreciate substantially. It’s not driving through the rear view mirror. It’s using past experience and current information to try to make the most judicious financial decisions you can. I guess we’ll see who is right soon enough. I’m not asserting that one side is right or wrong, but it might be remiss to categorically dismiss the possibility that the house of cards could come tumbling down at any moment. The higher something goes, the harder it falls!

When comparing renting vs buying, you should subtract off the principle repayment amount from buying, but add back in the lost interest (about 2.4% for 4 week T Bills) from the down payment. Doing that around here (South Orange County Coastal), renting is a better deal, unless you have $1m lying around and can pay all cash.

That said, a 70% crash from the peak that Millennial is talking about will never happen, even granting that prices, at least around here, have already dropped at least 10%. The reason is that the Fed has already chickened out with their QT, and there’s little doubt in my mind that they will drop rates to zero if we get a significant drop. Their primary loyalty is to the banks.

I already own some rentals, but want to move into a nicer primary residence. So will be looking to buy later this year if a good deal comes up after a further price drop. Would rent out current residence if that happens.

One worrying development, or good if you’re looking to buy, is the rise in gas prices. If oil continues to go up due to Trump’s policies towards Venezuela and Iran, that could cause a severe downturn, even given the US’s increased oil output. Oil prices shot up to close to $140/barrel before the 2008 crash.

I went to three Open Houses in Woodland Hills today. At all three, I was the only buyer present.

I used to talk to other open house visitors and tell them how inventory is going up in OC and other areas and now demand is muted. How expected market time has changed dramatically YoY and how we hit an inflection point last year. Now, it’s just me and the realtor. The market has become very boring. My realtors, I email with, about ten different ones are trying hard to get me to meet or swing by at their open houses. Sales are way done YoY so I am guessing some realtors are looking to find a job besides sitting at empty houses on the weekends.

Bob: “Trump promised MAGA (Ala the 1950’s and 1960’s where government projects like SS, Medicare, infrastructure building, (and a 90% tax rate on the wealthy were expanded)). However, he is a typical Republican and has cut these programs.”

Flyover: Could you please provide any proof that Trump cut SS and Medicare? I didn’t hear of any cuts. What type of “fake news” sources are you listening to? Don’t tell me that is CNN, NY Times or Washington Post. The infrastructure building continues based on available funds as it should.

Bob: “If the FED is truly not political, they will raise rates again soon.”

F: Since inception, the FED was political and continues to be political. If they ignore the political power entirely, their private business license can be suspended and they worked too much to acquire so much power. You can’t fight the whole Congress and WH. They have their own interests but they can not ignore entirely the other politicians interests. They work hand in hand.

My thought is that they will raise interest again late Summer 2020. By the time you feel the effect, the elections will be over. They try to avoid the appearance that they interfere in elections. Till then, they will continue with QT (money supply contraction) unless they get a major crash. If they start again raising rates next Summer (2020), the bottom of RE will be around 2022. It takes about 2-3 years for prices to bottom.

Rachel Maddow has “proof” that Trump colluded with Putin to lower SS and Medicare payments.

The Fed announced at their last March meeting that QT will end this September, and they are reducing the max Treasury roll-off from $30 billion per month to $15 billion per month, starting in May.

Flyover, please Google “Trump cuts Social Security” and there are about 1000 news sites that are moderate and support my claims. Trump is certainly not a New Deal President. Quite the opposite. So much for MAGA….

I hope the FED isn’t completely political. Otherwise why would they have raised rates at all? It is ruining Trump’s party.

Trump does not have the legal authority to cut social security, only congress can.

Bob, my dad is on SS. It was adjusted upwards every year with the bogus CPI number they published. I don’t have to google when I get his statement every year. Or, do you think that Trump increased the SS for conservatives and cut them for liberals?

Numerically, his SS was increased every year, not decreased. If you talk about adjusting SS based on REAL inflation, then I agree that it was decreased. However, all the entitlement under ALL presidents (D or R) are adjusted based on the published CPI not REAL inflation. So the cuts in SS are bogus, “fake news” as are all the “journalists” affected by TDS working for MSM. Trump is not the one calculating the CPI. There are the same bureaucrats who worked there during Obama years and they use the same methods.

Bob: “I hope the FED isn’t completely political. Otherwise why would they have raised rates at all?”

F: You don’t have to hope. The FED is not “completely political”. They are by the largest banks and for the largest banks best interests. The interest of the largest banks comes first. However, they can not ignore completely the politicians because their license to rob us depends on them. Why do you think they kept the interest at zero till Hillary lost and then they started to raise it faster than ever before? They try to stay off of the election fray because it doesn’t pay to have a bunch of angry politicians against you. Comey was not as smart as those from the FED and he paid for it.

” It was adjusted upwards every year with the bogus CPI number they published. ”

And now it is going down under Trump. Yet another Trump lie to keep us from the 50’s and 60’s when America was great. IMHO, when house prices and stock equities have gone up 300% and the FED and Trump says inflation is at 2%, someone is lying.

“You don’t have to hope. The FED is not “completely politicalâ€. ” I think you just contradicted yourself.

I agree that the Fed is run by the banks. However, if the banks get a secret agreement to bail them out when the economy crashes, they are run by the politicians. We have seen this all before. I think when Bernie gets elected in 2020, this corruption will be removed.

Bob: “And now it is going down under Trump. Yet another Trump lie to keep us from the 50’s and 60’s when America was great. IMHO, when house prices and stock equities have gone up 300% and the FED and Trump says inflation is at 2%, someone is lying.

F: Somebody lied to you. SS was increased in each of the last 2 years under Trump. It did not stay the same (forget about cuts) – it went up. Trump does not calculate the CPI. The bureaucrats (the same ones under Obama) calculates the CPI the same way. Your issue is with the government bureaucrats not with Trump. They used the same method like before.

Now, my opinion on CPI is that they lie. I agree that inflation is higher than the published number. Under Bernie, they will calculate it the same way.

“You don’t have to hope. The FED is not “completely politicalâ€. †I think you just contradicted yourself.

Bob: “I think when Bernie gets elected in 2020, this corruption will be removed.”

F: Keep on dreaming. You haven’t seen anything yet. Socialists are the most corrupt politicians on the face of the earth.

Yup, yah gotta be pretty dumb if you’ve Seen It All Before and think Senile Bernie is gonna win. Pretty F’kin DUMB.

Do you renters know the feeling when those RE cheerleaders tell you how high your rent is supposed to be? Than you tell them you pay less than half and they call you a liar? The feeling is priceless. Big thanks to my Landlord and big thanks to these RE shills who think that everyone in California pays 3k for a 2 bedroom. Let’s keep up this conversation. I’d like to hear it at least once a month! 🙂 🙂

Well rents ARE rising, so they do have a point there. But rents are not rising nearly as much the cost of buying for an equal property. Not even close. I live in San Diego in a pretty good neighborhood, and pay $2,750/mo for a 4/2.5 with a very nice view. House is probably worth $750k so I’d have to put down $150k and my payment would be about $4k/mo. Why on Earth would I do that? Instead I’ll save the $1,250 per month and add that to the money I have saved for a down payment, for when the price is $225k to $300k and rates are 7% to 8% where they should be.

Of course by then I’ll have a lot more saved up and will probably move up to an even better neighborhood. The real estate market is just that – a market. And one should never buy at the top of any market swing.

Great post Josh! Couldn’t have said/explained it better!

Buying makes just no financial sense.

I won’t stop saying it: my rent is a joke in comparison to the cost of buying.

Josh I am in the same boat minus 1/2 bathroom and a good view. Agreed 100%. It’s astonishing how high prices can go and people still won’t sell.