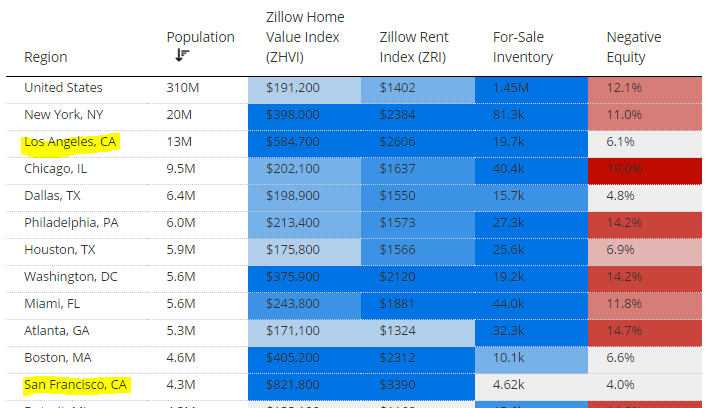

A look at real estate figures for the top US metro areas and a case study of San Francisco and Dallas: The Los Angeles metro area with more than double the population of the D.C. metro area has the same amount of housing inventory.

When investors look at markets they factor in a multitude of variables. Large investors were looking at capitalization rates and also local economies when buying rental property. For the first time in US history did we have a nationwide effort by large investors to buy up single family homes. This of course has caused a big dip in overall available inventory but has also pushed many home builders to focus on what the market was demanding which turned out to be more rental housing. The Los Angeles metro area (which includes the OC) has some of the weakest value for rental investors. This for a region where the majority of households rent. For example, the entire LA metro area has 19.7k homes for sale with a population of 13 million. Compare this to the D.C. metro with 19.2k homes for sale but with a population of 5.6 million. This is why you see some zany behavior when it comes to buying. But how do things look for the largest metro areas in the rest of the US?

Top metro area housing metrics:Â Case Study for investors

I’ve had contact and worked with many real estate investors that have bought homes to rent out. To a lesser degree I’ve also chatted with rehabbers and flippers. One thing both groups have in common is they both want to make money.

A common rule of thumb investors will use in valuing property is taking the purchase price of the home and multiplying 1% or 0.9% and trying to use that figure with expected monthly rental rates. For example, here is a hypothetical case for a property valued at $200,000:

$200,000 property x 1% = $2,000

$200,000 property x 0.9% = $1,800

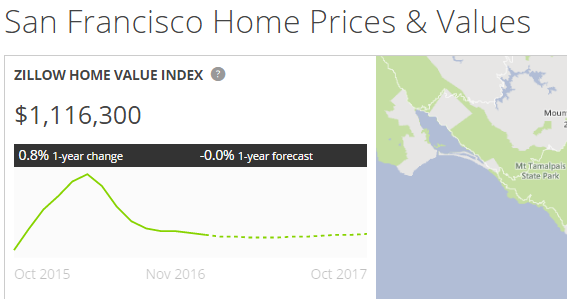

Assuming you could get rents between $1,800 and $2,000 a month, this would likely turnout to be a decent rental. Of course there are many other considerations including local economy, growth, taxes, insurance, and maintenance but many investors use this similar to a P/E for valuing stocks. This approach certainly has a better approach than using absurd mega down payment scenarios. Let us demonstrate with a case. For example, take a $1 million crap shack in San Francisco. Say you bought last year with a $200,000 down payment:

The market definitely looks like it is peaking. So equity gains for this year are neutral. But you could have stuffed that $200,000 down payment in an index fund tracking the S&P 500 starting in January and you would be up $40,000:

Of course house humpers and gut busting Taco Tuesday baby boomers fail to mention alternative scenarios or use convenient starting points – they also fail to mention that 7,000,000 people lost their homes to foreclosure since the crisis hit, including 1,000,000 alone in California (goes against the simple real estate mantras). A large part of gains in places like California are largely built on perpetual appreciation. Of course much of this appreciation has come from house horny buyers. Investors largely pulled out of the California market in late 2014 and 2015. What we have left is the manic buyer. Take a look at the data for other parts of the US:

If you run the rule of thumb numbers for many of these areas like Chicago, Dallas, Houston, Atlanta, and Philadelphia you get pretty close to the 1% figure – although even here you can see things are getting frothy. But look at freaking Los Angeles:

$584,700 Zillow Home Price Index with a Zillow Rent Index of $2,606 (this is a 0.45% ratio here!)

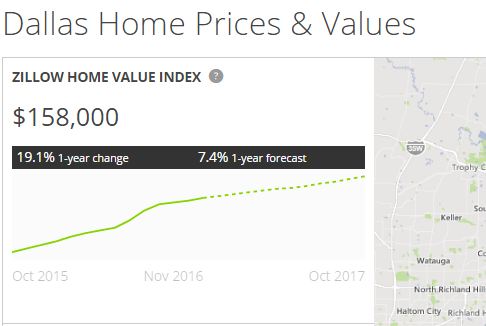

And keep in mind low interest rates apply for the entire country. So an investor looking to leverage their value is going to look elsewhere. That is why some of the hottest markets are in places like Texas:

So while San Francisco has been neutral for the year, the Dallas market is up 19.1% for the year. So do the math here instead of the “well I can paint my wall and water my lawn†emotional ploy here. If you were an investor today, would you buy one $1 million San Francisco crap shack that would rent for $3,500 or $4,000 or five Dallas homes at $200,000 each that would rent for $1,800 to $2,000 each?

Here are a few scenarios over the last year:

San Francisco – your $200,000 down payment would have a neutral return and your gains would largely be from the principal pay down. $1 million crap shack still worth $1 million.

S&P 500 – by doing nothing aside from eating Tacos and watching I Love Lucy, you made $40,000 without needing to unclog any toilets at midnight. $200,000 now $240,000

Dallas – your $1 million in real estate is now up 19% plus principal pay down. Your real estate is now worth $1.19 million for a gain of $190,000.

This is the math investors do. For California, what you have is constrained inventory but also, households that are cash strapped on rents. Foreign investors are still buying in niche areas but even in San Francisco, it has obviously slowed down. In California, the market is predicated on perpetual appreciation. When that slows so does the manic behavior.

For the most part, investors look to make money. Just because you didn’t buy the overpriced crap shack doesn’t mean you are not looking at other avenues, including other real estate in other area or other investments. In the last year the house humping cheerleaders seem to have ramped up their rhetoric. Maybe living in a termite infested depression era built HGTV inspired nightmare with a gigantic 30 year mortgage isn’t the dream especially when those gains begin to stall out.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

80 Responses to “A look at real estate figures for the top US metro areas and a case study of San Francisco and Dallas: The Los Angeles metro area with more than double the population of the D.C. metro area has the same amount of housing inventory.”

The reason inventory is so low? Because once you are in, selling can be a money mistake. Several reasons:

First, the IRS only allows you to move 500,000 tax free I if married, 250,000 if single ) between the house you sold and your new home. If you are up more than 500,000, you are taxed on the amount over 500,000. Then, you pay the realtor plus other costs, which can total around 7%. After paying all that money, you lose your prop 13. Therefore, trading up can cost you six figure money in taxes, expenses, plus the prop 13 loss just to buy an equivalent house. After losing six figure money just to sell, you need to re-borrow that money, plus borrow more. Many people I know in their mid 40s have more than 500K in equity, so they just don’t sell.

Secondly, you have to find your next home, then convince the seller to accept an offer contingent on your sale. That is hard to do. Otherwise, you have to sell yours, get the cash, then pray you can find a home for sale better than the one you sold. You might get stuck living as a renter while getting into bidding wars trying to get back in.

Often, your best move is to forget the whole thing. Just remodel the house and stay where you are. That saves a lot of money. Or, just rent it out and put 10% down on the next house. Use the rent payment to help pay for the larger mortgage. This is what I have done. I now have several homes in tow that turned into a gold mine. Unfortunately, because of the tax laws, I will never sell them. Several of my friends I went to HS with are in the same situation. They kept their last home or homes as rentals because the tax and fees are so ridiculous to sell. This is a why the inventory is so low. Everyone keeps their old homes as rentals because that can be cheaper than paying the tax man and the realtor, plus over 20 years, the homes will likely make you wealthy. Notice I said likely. It is not for sure they will make you wealthy. But, most likely they will.

Right on the money jt. This is exactly how to play the game in socal. One of my acquaintances turned his Torrance box into a rental and did a cashout refi to use for a downpayment for his newer, much nicer place. You keep the rental income which seems to go up every year and the Prop 13 basis and you essentially have a free hefty down payment for your new place. Welcome to socal RE, the competition here is brutal!

Makes perfect sense to use your house as a piggy bank if your property taxes are locked in with Prop 13. Unfortunately here in Texas the sky’s the limit even if you don’t sell or refinance. You are just an ATM for the local taxing districts and the appraisal district that does their bidding.

“I went to HS with are in the same situation. They kept their last home or homes as rentals because the tax and fees are so ridiculous to sell”

Ever hear of 1031 tax-deferred exchange transactions ?

Prop 13 has only limited benefits. SoCal property taxes can still increase via so-called “parcel taxes.”

“Property taxes” impose property taxes based on assessed market values.

“Parcel taxes” imposes property taxes based on the property’s square footage.

Parcel taxes (property taxes by another name) remain legal despite Prop 13. Every few years, Santa Monica voters pass a new parcel tax, usually “for the children.”

Read about Parcel Taxes — The Other Property Tax — http://www.caltax.org/ParcelTaxPolicyBrief.pdf

The rub of course is that being a landlord is not a desirable option for most people because it sucks in a lot of ways.

In other words, due to a defective culture of competitive speculation, the area becomes more difficult and risky for basic items of consumption like a house to live in, so people become stuck and unable to make a move, sounds awesome!

At some point i think all these new landlords are going to figure that out and all hit the exits at the same time. The house my X sold this year (at a loss from 2005) was sold to an “investor” who’s going to rent it out.

As was the house next door to hers….there were actually 4 houses for rent on her street alone last time i was there.

Selling is only a money mistake if you are hoping to move up and stay in the area! If you are retired, retiring and need the equity, or are willing to move out of state, selling can be liberating! Personally, unless I lived in north San Diego County or Santa Barbara, and was close to the beach, I’d be looking to cash out and get the %e!! out! I bought a beautiful home on 2.5 acres in the inland northwest, am 2 miles from a large lake, i.e., 25 mile long lake, have a boat, and have a nice little beach/park to enjoy. Certainly it’s not a beach place in winter, but there is plenty of nice weather for months in the summer and the water is much cleaner than anything in and around L.A. or probably San Diego! I have enough left over from escaping So. Cal. to escape to warm tropical locales in winter, and have a comfortable retirement!

I agree with your comment. I live in Santa Barbara and bought now own a home; spent a a lot on a remodel finished 2016. Remodeled to below slab ( new waste water lines) for the same math logic u outlined.

You have real estate investment management outfits in CA trying to peddle remote investment in Texas. The lunacy of buying at an inflated top is very interesting. I imagine they will receive a nice wake-up call on their property taxes, which are grossly understated by the industry purveyors of “fake news”. Real property taxes in Texas metro areas are closer to 3 percent.

Hard to hit that 1 percent threshold on a turn-key investment of $200,000 in Houston with the market awash in class-A apartments offering 2 or 3 months of free rent.

http://aaronlayman.com/2016/12/average-rents-cinco-ranch-decline/

Expect to see more and more of these investment gurus turn to peddling their get-rich-too stories in a real estate seminar near you.

“Real property taxes in Texas metro areas are closer to 3 percent.”

This is something people just don’t realize, they only see a 300K McMansion. The cooling, heating and maintenance due to brutal weather is also usually not accounted for. And there is no Prop 13 in Texas. If property values go up a lot, the tax man will come a knockin.

The weather isn’t brutal. Stop exaggerating.

The quality of the weather is a highly subjective judgement, Hotel California.

I personally consider any summer temp over 82 F to be “brutal”, which is why I live in Chicago. If I ever leave, it will be for Montreal, or some other cool-climate place, not a place like Houston, notorious for its heat and humidity- Chicago summers are bad enough. Or, for that matter, SoCal, even though I’d love a little studio in Los Angeles to get away to in January once I’m retired. But I’d want be out of there by the time summer arrives.

Have you ever spent a summer in Houston?

Brutal is an understatement!

No, I’ve never spent a summer in Houston and wouldn’t consider living there, because I’ve heard how the summers are there. They make St Louis summers seem cool. I’m a pale-skinned, blue eyed woman with no heat tolerance, who can’t spend more than a half hour in the sun. I go to the beaches here in Chicago only in the morning, or when the sun starts to list around 6 PM, never in the afternoons or early evening. I do my swimming at indoor pools.

I’ll move to a warm climate when it’s time for me to pass on. Having suffered heat prostration in the past, I can tell you it’s one of the kinder ways to die. You don’t feel any pain until you come to. First, you feel rather dizzy and light headed, and your clothes feel very heavy. Then you feel drowsy. You have no idea what is overtaking you and you are not in pain. Then you wake up, and you are lying on the pavement wondering what happened, and you are suddenly freezing cold and shivering all over even though it is 90 F outside. But you don’t feel much of anything when you are starting to be overcome.

Sure, but there is no state income tax. Cost of living is way, way below Cali except for utilities as you mention.

i have a house in the heights area, since i have my homestead my mortgage payment is only $639.00 per month.i learned home sales are up in houston 23% as people are rushing to buy since interest rates will go even more soon.i got my rate in 2011 at 3.39 and my mortgage balance is only $76,500,the size of my home in the heights is 1,845 sqft and lot size 4,000.i have been checking out the cheaper hoods in houston and the burbs and im shocked at the prices of homes my size or smaller,since the heights is one of the most expensive hoods in houston, it just shows im sitting on a boatload of equity,just like jt im keeping the house since the equity i have is way more than $250k and houston will continue to grow and im in my 30’s.

I watched House Hunters the other night and learned something new.

The realtor showed a couple a house that was $14,000 over their budget. He had the gall to tell them: “Remember, you’re not buying a house [or mortgage], you’re buying a monthly payment”.

I wanted to put my foot through the TV. Not as pyrotechnically effective with a flat screen as one with a tube, but the sentiment was the same.

And guess which house they chose.

I love hearing stories like this…just more signs of impending financial doom

crash & burn baby…crash and burn

“A window. I love the vintage charm. I can imagine myself looking out the window”. The potential homeowners are just as bad as the realtors and so willing to be sold.

I’m not so sure it’s a sign of the end (although to be fair I do think we’ve peaked). As far as RE agents are concerned, it’s never NOT a good time to buy or sell. They’re on autopilot regardless of the state of the market. Some are lying, the rest are delusional.

Aaron Layman,

You are right on in your comment. We in the bay area are barraged by experts proclaiming the Texas aka “Dallas” market is ripe for rental income. I always wondered myself if it was so great, why would they not just keep it to themselves and buy their own rentals. caveat emptor

What exactly is this blog? It seems like all I see commenting are a bunch of cheerleaders or mega bears.

Look, if you looking for a place to live, then you promise you can afford, and you do what you have to do to do it. I’m not talking about any kind of investment, I’m not talking about making any kind of money, I’m talking about buying a mortgage and paying on it for 30 years. Then, at the end of the 30 years, you have a much better chance of retirement than someone who didn’t do that.

Quit playing all these money games. Just pay your own little house off, only worried about that, you’ll be fine.

That’s essentially still the case in most of the country. The problem is that real estate in LA is so expensive that you can get burned if you don’t buy in at the right time (few rarely make it 30 years in one place, or 10 years, for that matter.)

Yep, this. The culture of speculation and greed which exists out here has so perverted the concept that timing execution has become paramount. Mid-20th century ideas such as staying in the same house for 30 years is outdated.

Amen, Realist. But it’s become divorced from that. It was shelter. Then an “investment”. Then an ATM. Then the biggest mortgage and commitment to 30 years of income one has yet to earn, then just a monthly payment, like using a Best Buy credit card. Perpetual and crushing debt to maintain a facade rather than actual value and security.

So distorted from what it actually is: shelter and a payment locked in at a certain amount for the life of the loan rather than constantly rising rent or the whim of a landlord.

I don’t blame anyone for rejecting the whole premise, Realist. There is nothing wrong with renting. It has it’s own benefits and too many have it in their heads that it’s always better to own, when it can be a destructive force, especially when it’s done for anything other than housing oneself and family and throttling oneself financially to do it

This blog is effectively for people simply obsessed with real estate. Real estate (outside of organic buyers and professional) is basically a delusional playground for a lot of people; It is a largest transaction they will ever hope to conduct in their lives and it is also does not require much brain power. Real estate generates more dreams and delusions than anything else. It is a psychological gold rush.

In this blog, a lot of people said they moved out of Cali, but not a single person said where.

Once in a while a good comment pops up with unusual micro-economic insight, but for the most parts I feel most posters are just dreamers.

Surge – more than once I’ve said where I moved to: MT. I can specifically recall OR, ID, WA, and CO mentioned by others.

Seems like you’ve made a generic complaint of other posters, then your post just reads as a generic complaint itself.

Where people move depends on lots of factors, therefore it may be irrelevant to your circumstances. I stated many times that I moved and the factors involved and the places I like. It depends on weather, job, retirement, weather preference, family and friends, therefore where they moved, it shouldn’t mater to you.

You can search the previous article for more details.

I replied to a fellow poster’s question a while back, that I now live in Rio Rancho, New Mexico after 33 years in Los Angeles. The “Land Of Enchantment is a great place to retire, if you like four seasons, and take into consideration what my accountant said “it’s not Texas, it’s not California, IT’S NEW MEXICO.” Plenty of nice homes here for the price of or less, than a “California Crap Shack”. Not a place for beach people or surfers though.

I think a lot of people do not want to mention where they are now living, in fear of Californication. No worries about that here, not enough well paying jobs in New Mexico.

It’s clear from the Zillow graph that price appreciation is flat-lining (or even going down) in the Bay Area. Sheer madness to buy now, especially in crappy neighborhoods in SF and Oakland that are absurdly overvalued. I can’t remember where I read about the “Cycle of Speculation”, though its probably easy to find online: Elite investor insiders initiate the cycle and make the biggest gains, then come the somewhat-educated Second-Tier that catch on to the appreciation in prices and hope to make a profit, finally there are the “suckers”- the unsophisticated mom and pop investors who sink their savings into the mania just at it’s peak (be it Stocks, Real Estate, Tulips, whatever)- they’re the ones who lose their shirts when it all goes South. Meanwhile, by this stage the originators of the boom (Tech VC’s, Corporate RE buying-up foreclosed homes etc.) already withdrew from the frenzy they created, taking their profits with them. When you wrote: “Investors largely pulled out of the California market in late 2014 and 2015. What we have left is the manic buyer” I think your latest post has already shown that the writing is on wall and we are nearing the final stages of the speculative cycle… I feel terrible for those who stand to lose the most.

I bought in 2006 for 760K in SD and right now it’s current pricing is at 700K, give or take some..

But if you add in the taxes and maintenance.. then I am losing a boatload of money…

I have a friend who is renting a big house in San Diego/SD for $3500. If he wants to buy the same house, it’s gonna cost him atleast a million dollar… so he is not that inclined..

From what I learn .. housing is all about timing….

You are so f’ing right. My saying has always been that, in California, the 3 most important things when buying RE are (not location, location, location) timing timing and timing.

Although the last 30 years are not going to like the next 30 years. Falling incomes, interest rates that really can’t get any lower and 10,000 boomers retiring every day is going to make changes that no one can predict with any certainty. I’ve been saying for a while now (and I’ve just started reading articles saying the same thing) “who are the boomers going to sell their assets to”? The guy who’s making less then he did 10 years ago?

I think the average age of the people in my GF’s neighborhood (just based on seeing them out side) is about 70……do the math on that.

I think the average age of the people in my GF’s neighborhood (just based on seeing them out side) is about 70

The younger people are probably at work.

Doc, I’m going to assume that you know the 1% guideline is a very rough estimate. My rents are at about 0.7%-0.8% and I’m doing pretty well.

As long as values go up, that offsets the purchase price vs rent ratio. I bought/built roughly 4 years ago and recently did a cash-out refi. The net to me now is zero cash outlay (i.e. initial purchase $300k so initial cash from me $75k. Valued now at $400k so the new mortgage is $300k and I take the cash at closing.) Even with the new mortgage, there is still significant positive cash flow.

Just one of the beauties of being in a flyover state…

And yes, I’m very well aware that prices won’t go up forever.

You are right, Jeff. It is better to have 0.7-0.8% rent REAL than 1% on paper. I look at it as a bond. Therefore, how much the ROI is important, but equally so is the QUALITY of the bond (the rating). If you rent to white collar civilized professionals with 0.7-0.8% is better than getting 1% on paper in a slum. Long term, the 0.7-0.8% will produce far more net profit than the 1% in the slum with bad quality renters. That is because the bad renters don’t pay all the time or they stop paying. On top of that, they trash the place which bring the net profit really low, lower than in the first case scenario. Many times, in the slums you have to use a lawyer for evictions and that drops the profit even more.

I always position my rentals/investments towards the Costco market segment/demographics. In this case, my paper calculations match the reality. In the case of so-so neighborhoods, the real return is way lower than the initial paper calculations. That is the reason, the good quality renters get better deals than average.

Also 1 house is A LOT easier to manage than 5 houses.

This real estate market is downright offensive right now in Nor Cal. We walked three properties in the last few days that were ‘internet beautiful’ as my wife and I refer to them. Look great on google earth and the pics of course, and all of them were third world shitholes in person. What’s worse is that all three of the realtors excitedly told me they were ‘flippers’ and asked if I was a ‘flipper’ too. I always throw up in my mouth a bit when house jockeys ask me if I’m a ‘flipper.’ I have to explain to them that I am an actual real estate investor that buys on real fundamentals and they look at me in disbelief as they try to wrap their heads around this foreign concept.

I had to educate one realtor on what a SIP house was after she insisted that the pile of crap I was looking at was not a modular home. This realtor didn’t even know what a ‘stick-built’ home was. Really, we are talking about total mental midgets slinging real estate right now and even dumber people buying this crap. This market reminds me of 05ish when I was selling real estate. It isn’t quite as bad as 06 but it is ramping up to be. The house jockeys (realtors) are out of control as usual. Sorry Jim, your projections have been way off and premature, but someday during Donald Trump’s first term you will be right.

“I have to explain to them that I am an actual real estate investor that buys on real fundamentals” Ha ha- Nice!!

I thought about selling my little crappy house in Santa Monica, but held onto it, rented it out and pulled some equity out to build a house on a much better lot.

So glad I did, but I’m not gonna lie…it was a tough couple of years through ’05-’08. It could of gone south in a heartbeat and I could of lost both houses. Now I’m paying my new house mortgage and the 2nd on the old house completely with the rental income. and I deduct the hell out of every maintenance thing with both houses…I think jt is spot on…why sell once you get it? Now I have 2 houses in one of the best cities in LA County with low overhead, strong rental income and low property tax basis.

So why come here? I mean, really? Why come here? If you guys have it all figured out, what’s the point?

Excellent! I love how GreenGroovyMom said she almost lost both houses, really inspiring story on owning property.

There goes Motel California again whining about anecdotes and personal life stories relevant to real estate. Are you that big of an ego that you cannot stand to hear someone’s investment experience? People come here because they love real estate–they want to own it or they already own a lot of it. And newsflash, some people learn from other people. I gleaned everything I know about making money in real estate for example because I listened to the multi-millionaires that I sold apartment complexes for when I was a commercial broker. That’s right, I listened. Learning from the experience of others is a valuable tool in life. You should try it.

Mr Miyagi, your response has some very transparent clues about the point I’m making.

You continue to take and make things personal whether via childish misrepresentation of my screenname, applying cheap labels such as “whining” or accusations of “ego”.

Anyone who feels confident about the skepticism opined here being wrong wouldn’t feel the need to stoop to that level, so save the patronizing life lessons learned sermons for yourself.

The point is that if there was enough confidence behind the usefulness of such anecdotal formulas for others, there’d be no need to visit a housing market skepticism blog. I wouldn’t buy for a minute that any of you are here for charitable purposes. Anyone can easily make up anything anonymously on a comment forum, it’s not even remotely comparable to learning from people you know personally.

Motel,

The difference between you and me is that I think most people are here because they love real estate. As I’ve stated they either want to own or do own. Big deal. The purpose is to discourse over the subject which whether you like it or not, includes life experience.

If you are so skeptical that you think everything people say on this forum is an elaborate lie to maintain some sort of online honor, then you have psychological problems that nobody on this blog can help you with.

I do agree with you though that seeking advice from people you actually know in the flesh is a great idea. I don’t disagree with you, in fact that is where I stated that I initially learned how to be a successful investor–real actual human clients I had that owned a lot of multi-family investments.

Clearly the question has struck quite a nerve which shows it’s probably getting very close to the truth.

Mr Miyagi, your responses to it continue take a personal attack angle. That’s the real difference between our posting behavior. It’s a classic lack of confidence tactic. You’ve established a pattern of this here and on another similar blog.

Now you’re doubling down by creating a smokescreen of exaggerated untrue suggestions about skepticism and mental state.

This blog is entirely premised on questioning the religion of real estate, therefore the suggestion that it’s a natural forum for the congregation of lovers is ridiculous.

“and I deduct the hell out of every maintenance thing with both houses”

so then now both houses will not be a primary residence so you can’t get the tax free $250K on their sale……unless you are committing fraud.

As i understand it the $250K/$500K for married tax free exemption is for a primary residences only and since you are deducting for both houses they aren’t…….

oh and don’t you have to pay taxes on the rental income as well? I certainly hope you got all this covered.

Damn straight Im committing fraud. I deduct the handyman expenses on both houses but use the address for the rental. Its not a ton,but having a rental is a good ‘shelter’. Listen I am small potatoes for the Fed to red flag. And FYI, I don’t know ANYONE with a rental who 1. declares the true amount of rental income as its not tracked. The renters can’t declare it. 2. Doesn’t depreciate and write off EVERYTHING they can…

Its one of the few perks left on filing yo’ damn taxes! The Fed Govt can suck it…they take way too much of my money anyway.

GreenGroovyMom: I don’t know ANYONE with a rental who 1. declares the true amount of rental income

My father was from the Old County, and as a new American, was proud to pay his taxes to the IRS. He always reported his true and total rental income.

It was like that in the old days. (I’m talking 50 – 60 years ago.) Immigrants would come to America, and strive to “become Americans,” which meant proudly obeying the laws.

Back when I owned rental property, I too always reported the true rental income, and never deducted anything fraudulently. It never occurred to me (or to my father) to do otherwise.

@Son of a Landlord…thank your father for paying his taxes. Although, he probably wasn’t too happy about where they were going after he was here a few decades to see the misuse of taxpayer money. I’m happy NOT to let the Feds know about my rent increases, thankyouverymuch.

I’m anticipating interest rates will go up. A lot. Is their any online info that calculates how many adjustable rate mortgages are out their?

Here’s a condo in Westwood/Century City for under $120k — https://www.redfin.com/CA/Los-Angeles/10590-Wilshire-Blvd-90024/unit-7/home/6804402

It’s only 202 sq ft. NO KITCHEN. (There is a fridge and you can buy your own hotplate or microwave.)

Curious sales history:

1978 — sold for $30,000

1998 — sold for $5,000

2005 — sold for $660,000

2015 — sold for $78,000

2016 — listed at $119,990

I’d love something like this as a winter getaway, but not for that price. I was thinking more like $75K.

Are you sh&%tting me?!? A condo w/ fees!! That looks like it was an old man’s skid row SRO back in the 60’s. Charles Bukowski probably wrote his best work here. All you can fit in there is a freakin’ pull-out sofabed. No kitchen? Is the shower shared down the hall??

HAHA good description DonPelon.

That unit can only be sold to members of that HOA, and is intended to house domestic help.

That $660,000 must be a typo…probably was $66,000 ?

Great. I could own a hotel room?

“2005 — sold for $660,000”

LOL pure insanity…….good for the person that won that lottery though.

Probably fraud where the “buyer” got money back from the seller and bailed the state/country. Common thing at the time.

A lot of foreign money both domestically (mainly CA) and internationally are still buying in low inventory Texas markets. This is why you are seeing gains of 19% in Dallas. I just sold our last rental property in Austin TX and in the slowest time of the year I sold it for full asking price in 35 days to an investor who got money from family in China as part of down payment. You have something like 54% of population as renters in Austin, and 50% of the local is economy is hospitality jobs. The rents are good in Austin but its still tough to make the 1% rule and you will have multiple people sharing a home. The house next to the one I sold had 5 ppl living it and this is a middle of the road blue collar neighborhood. Everyone you talk to in Austin owns a rental property this is one of the sirens going off telling me to sell and raise cash.

Los Angeles is indiscriminately expensive to buy a home. You look at the middle of the hood where you car will get broken into for a kit kat bar… $500,000. A house way out of town, $500,000. A small condo in Hollywood $500,000.

You look at Denver, they have very expensive houses BUT there are also poor areas where you can buy a house for cheap to make up for all the times your car gets broken into.

The more I look at housing here the more I come to appreciate how affordable renting is. I live in a very hot area, no roommates, only pay for electric and internet and have a pool I don’t have to maintain.

The weather is obviously amazing and the job market is great for Finance/ Accounting. But I really don’t think they have done anything to protect the Middle Class and it will one day be gone. Measure JJJ recently passed which is another blow to the middle and most of the lower class citizens here.

Housing to Tank Hard in 2024.

I think JT might object with your Tank date.

I have a number of beach close homes and I am loving life right now. However, every so often, they do drop a lot in value. And,once this current run is over, there will be another drop in the cards. However, I am certain there will be a drop well before 2024.

A new study by Trulia indicates that it requires 91% of the median income in L.A. to afford a median priced home. Obviously S.F. is much worse at over 100%, and other California cities are in similar shape. Basically, the dream of owning a home is dead for most, which leaves renting as their only option. While it appears to be a sweet spot for landlords, the real question is how long can real estate and rental prices stay insane? And, as the Fed increased rates today and indicated there could be 3 rate hikes in 2017, what impact will that have on this mess … will rates force home prices prices to come down, or just further shrink affordability?

“Rents Are Falling in New York City. Is This a Crash?”

http://www.slate.com/blogs/moneybox/2016/12/13/rents_are_falling_in_new_york_city_is_this_a_crash.html

They’re falling in trendy areas of Los Angeles, too. The media is finally catching on, late to the game, as usual.

The homes built in the roaring 20’s are quality. Lath(oak strips) and thick plaster on the inside. The outside, 1″ thick redwood planks, tar paper, chicken wire and thick stucco(cement) that will stop a 9mm. Thick hardwood floors inside with a lot of wood molding, ceiling and floor. This is something that has never been seen since then. The new homes can’t withstand an earthquake like the retrofitted roaring 20’s homes. You know that the big one is overdue and all those other homes will fall down.

The new homes can’t withstand an earthquake like the retrofitted roaring 20’s homes. You know that the big one is overdue and all those other homes will fall down.

Depends on how new the home is. Homes built from the 1940s to 1970s likely won’t fair well. Especially if they’re brick, split level, or taller than one-storey.

But homes built after 1980 are allegedly better built. Even better if built after 1990. And safer still if built after 2000.

Two realtors have told me that if a home was built after 2000, it’s relatively easy and cheap to buy earthquake insurance for it.

Of course, realtors lie. Does anyone here know if the above is true?

$900 for structure replacement value of 320k.

That is correct. Houses built after 2000 are better built.

The key word is “retrofitted” roaring 20’s home. The older homes with raised conventional floors, as opposed to slab on grade, can be knocked off their pilings if not seismically restrained.

city permitted and inspected cripple wall braced, bolted down into the cement foundation. Guaranteed that anything under the floor would not move. Then the lath and plaster and the outside planks, chicken wire and cement holds it together. I spoke to people who do tear downs on these homes and it is a big job due to the heavy duty construction. They told me that it withstands earthquakes. They say that the modern construction is easy to tear down. They hate those 1920’s homes.

My mother owns a homes in Santa Monica, between Montana Ave and San Vicente – built in 1923 and one of the oldest houses on the block. It is the raised foundation type with lathe and plaster and real 2 x 4 beams. Often times, when contractors have come to work on the house, they have also been impressed with how solid the floors and walls are.

It has survived all major quakes so far, with only occasional wall cracks. I presume all these types of homes will survive more quakes if they are located in the Valley or Inland Empire, but if a 7.0 happens in Santa Monica, a lot of those homes may slide off the foundation. My mother’s house has had the typical earthquake bolting as a precaution. Like someone else posted, its not the walls and floors that are a problem, it is when there is a strong lateral movement of the ground that can make a house slide of its foundation.

Wood frame structures generally survive earthquakes well. You want a structure that is flexible and light enough to withstand a lot of shear and still hold together. Rigid structures like concrete without enough rebar, or things that can easily separate like brick are the worst. Another danger is if the structure slides off it’s foundation — modern CA construction requires bolting to the frame to the foundation. A 20’s house may still be fine, but heavy and ‘solid’ don’t necessarily make something more earthquake proof.

Agree. There is nothing built before or since, quite as good, or as beautiful, as the houses and buildings of the 1920s. They have rock-solid construction, beautiful architecture replete with wonderful millwork and details, and great floor plans. They’re the best of both modern and traditional-they have the beauty, craftsmanship and detail of an earlier era, but have compact, efficient floor plans that make good use of space, and usually ample closet space, found only in places built in modern (post 1918) times. I have lived in 20s vintage apts of various sizes in St Louis and Chicago since attaining adulthood, and am so spoiled by the beauty and comfort of these fine old buildings, that the typical modern ranch house looks like a steep comeldown to me.

yes, I live in an English Tudor home in Burbank, built in 1926. I do not have the cement driveway, just two unobtrusive cement strips through the lawn. Oh those were the days of the Packard, Lincoln and Cadillac. Of course the house was modernized with Central air and heat, copper pipes, and double paned vinyl windows. The modern homes do not have the solid wood inside doors with the vintage glass knobs and etc. The modern home plaster board walls are so flimsy. Moving into a new home will take quite an adjustment for me.

Buy now, with interest rates going up your monthly payment will skyrocket, buy now before it is too late. Still have a few darlings here in Oxnard. We have “Taco Tuesday” on as many days as you like. Me and the good Capt Morgan are going out today on my Sea Ray. Come next year business will be booming. During the holidays, business is slow.

but people who voted for trump are telling us that they are gonna get a manison in beverly hills for $100k,if the interest rates go up,lol

DJ, you come on over to Oxnard(aka Newport Beach of Ventura County) and I will show you the Taco stand that my nice(twice removed) runs by the harbor. You can fill up on all the Tacos that you want. I may even invite the good Capt Morgan to join us. feliz Navidad

carlos,im sure i will have a great time at the beach.beautiful weather,beautiful views of the beach and water and the beautiful women smiling jumping up and down, showing off their beautiful figure,well it’s time to visit cali again.

Leave a Reply