Orange County condo prices hit record level: Can’t afford a home? Time to move into a sophisticated apartment with a mortgage.

The last hurrah in the previous housing bubble included a massive desperation of people to buy any sort of real estate. Forget about crap shacks, let us go with crap condos! That is the point we’ve now reached as well. A recent report shows that condo prices in Orange County have now reached a record level. This makes sense given the blistering horny buyers that can’t get enough of the tiny amount of inventory out in the market. The same shtick is being pumped out there from last time including “condos are a great way to build equity so then you can buy a home.â€Â How convenient! Of course people got massively burned by condos in the last bust because condos in many cases are apartments with 30 year mortgages. And in Orange County, you have absurd levels of HOAs that actually can go up. Buy that condo now or be priced out forever.

Condo mania

Condos are simply a way to get into the real estate market and given current home prices, many people are jumping in because this is all they can afford. Why rent an apartment when you can own one? It isn’t any surprise that during the last bubble, the peak in condo prices was nearly identical to the peak in housing values – this is just a cheap alternative.

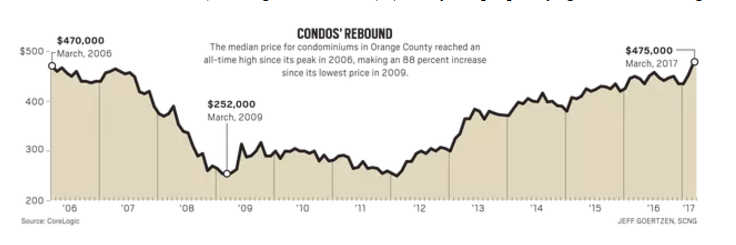

But take a look at this timeline:

Source:Â OC Register

The last peak was reached in 2006. At that time condos in Orange County were running at $470,000. Prices then corrected and hit a bottom in 2009. So let us just say that condos track inflation overall. What should the cost of a condo be today?

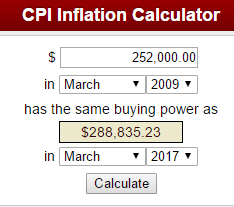

Source:Â BLS

So if you bought at the trough in 2009 for $252,000 that condo if it tracked inflation would cost $288,835. Instead, that condo today is now going to cost you $475,000. That is an 88% jump in prices since 2009. Did household incomes go up by 88%? Interest rates in 2009 were low as well. But right now everyone is humping any piece of real estate and condos are the less than attractive person at the club looking for someone at 1:59am. “What the heck†you might say since many are drunk off of the current mania.

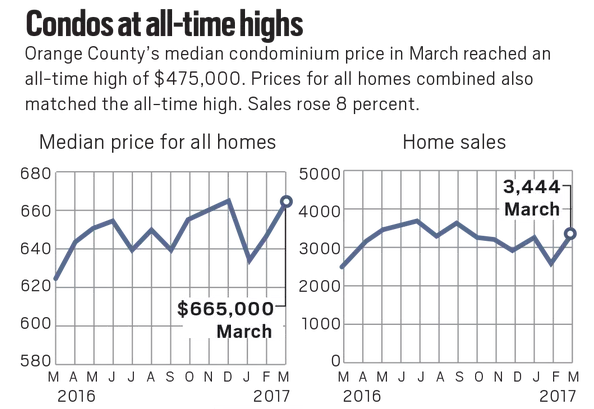

The market is hot with the little inventory that is out there:

That is what is pushing the market. But really condos are nothing more than apartments with mortgages. Take a look at this condo in Irvine for example:

93 Greenfield # 100,

Irvine, CA 92614

2 beds, 2 baths listed at 1,159 square feet

This place last sold in 1983 for $101,000. The current list price is $549,000. Plugging this into the inflation calculator yields a current price of $251,778 which is very close to the trough price seen in 2009.

But here is where the fun comes in. Take a look at the HOA:

All this nonsense rhetoric that once you pay a home off, you have no expenses is a lie. In this case, you have HOA, property taxes, and insurance that you will pay forever. Sort of like rent. Funny how that works out. In this property, HOA + Property Taxes + Insurance will likely run you close to $1,000 per month. I’m just saying that this is far from being free. You could rent a similar place for $2,100 to $2,300 per month.

But of course, you will never get this kind of math being sent your way because of the delusional mania we are currently in. People have forgotten that stocks and real estate do correct. Orange County has once again shown why it is the number one most expensive county in Southern California.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Subscribe to feed

Subscribe to feed

219 Responses to “Orange County condo prices hit record level: Can’t afford a home? Time to move into a sophisticated apartment with a mortgage.”

This is also not taking into account that if the building does not have earthquake insurance and a big one hits which causes the building to be condemned, you’re out a lot since you own a small sliver of the land. Even buying earthquake insurance for just your unit provides little protection if the whole building isn’t covered.

“That is an 88% jump in prices since 2009. Did household incomes go up by 88%? ” That says it all…..Housing to tank hard….i think i am being conservative with my 50-70% drop during the next crash 🙂

Factors like domestic wage don’t hold as much weight as it used to. We’re in a global market with the worlds most populous country heavily invest in our real estate market and you’re still talking about wage here in the states? Who cares if the average American can’t afford a house, there are millions of Chinese buyers that see our market as a bargain compared to their market. And in a sense, they’re right. Our prices have been well below the global average for quite some time and that’s about to change soon. Housing is not tanking hard at all, worst case scenario housing will dip a few percentage points, stagnate for a little bit then keep climbing although even THAT outcome I can’t see happening anytime soon considering how strong China money is pouring in.

Yes, President Trump who earns the majority of his income from foreign real estate investment will help the middle class. I’m not seeing it. Foreign real estate will continue unabated until we elect a new President.

NewAge,

The Japanese lost their shirt buying RE in CA…same story…they invested heavily in CA real estate and nobody talks about them anymore….same will happen with the Chinese.

Housing market is cyclical, wait until the global bubble burst and you will ask what happened to the Chinese investors…..maybe in 20 years from now people from India will invest in CA RE…..rinse and repeat….boom and bust….

Funny how history repeats itself….just switch japanese with chinese and you find yourself nowadays….of course the RE cheerleaders will be creative and find something in order to keep their theme going THIS TIME IS DIFFERENT

http://articles.latimes.com/1992-02-21/news/mn-2588_1_japanese-real-estate

“there are millions of Chinese buyers that see our market as a bargain compared to their market.”

Alternative facts.

A few Chinese “investors” who launder their money are the reason why boomers want 50% more than what their crapshack is worth? LOL. Not a chance…i will visit an open house when the market crashes. Before then…..try and sell your crapshack to these “millions of Chinese”.

@Nice Try

I have to study the history of the market and how it intertwined with foreign investments, namely the Japanese investors of the late 80’s particularly because that event is used as an example of the potential outcome of the Chinese investments of today. I was not born during that time so it’s time to dust off some books and learn a thing or two.

However, I still feel that the Chinese and Japanese are two different beasts with two completely different factors that come into play with how sustainable their respective economies are. Seeing how Japan’s economy still hasn’t recovered from that downturn, I’d say it was over before it started with them. The Chinese have a much stronger economy and have much more of a global presence than the Japanese have ever had so that alone leads me to believe that there’s no stopping them anytime soon.

The only way I can see the Chinese come tumbling down is if the US dethrones their manufacturing dominance via widespread automated technology. What’s better than cheap labor? How about no labor? This is very possible but in the distant future. Until then, the show will go on.

“The Chinese have a much stronger economy and have much more of a global presence than the Japanese have ever had so that alone leads me to believe that there’s no stopping them anytime soon.”

The Chinese miracle has been nothing but another big bubble where they’ve been taking on record debt. Their own GDP numbers are questioned by Western investors and economists. Their ghost cities are well known among economic circles. Too many houses being built to provide jobs for a clientele that cannot afford it. And then, the government encourages its own people to buy into a bubble stock market.

So much for MAGA. Here comes moah Chinese money:

Kushner family in Beijing: ‘Invest $500,000 and immigrate’ to US

http://money.cnn.com/2017/05/06/news/jared-kushner-nicole-family-event/index.html

#fakepresident and family at it again.

Forgot the most important part of the article:

The EB-5 visa has been used by the Trump and Kushner family businesses. Foreigners, particularly wealthy Chinese nationals, have used the EB-5 program as a ticket into the states. And that promise has helped attract foreign investments for U.S. real estate projects.

It’s laughable that a dimwit like Gibbler would reference a link from CNN the epitome of fake news and then blame Trump who has been in office a little more than 100 days for a program that has been around for decades.

The EB-5 Immigrant Investor Visa Program was created in 1990 by Congress with the Immigration Act of 1990 and provides a method for eligible Immigrant Investors to obtain United States visas as a path to permanent residence—informally known as the green card—by investing from $500,000 to $1,000,000 in projects that create full-time jobs in USCIS approved Targeted Employment Areas or high unemployment areas (HUAs).

During the OBAMA regime in 2011, USCIS began making a number of changes to the program in hopes of increasing the number of applicants. By the end of the 2011 fiscal year, more than 3,800 EB-5 applications had been filed, compared to fewer than 800 applications in 2007. By 2014, the number of EB-5 visas granted had more than doubled since 2009.

In 2013, the U. S. Securities and Exchange Commission (SEC) issued an investor alert to warn investors about an increase in fraudulent investment scams that exploit the EB-5 visa program. For a twelve month period in 2015 and 2016, the SEC has successfully brought “enforcement actions against nearly $1 billion worth of EB-5 projects”—a majority of them against “individuals or companies that misuse investors’ funds”. In August 24, 2015 the SEC filed civil fraud charges against Lobsang Dargey for his misuse of the EB-5 Visa program by misappropriating about $136 million dollars from Chinese investors through his Path America entity.

The Trump administration announced that they would be auditing the program. Trump’s current tightening of all immigration abuse includes making sure this program was used within the legal guidelines. The overhaul would significantly increase the investment level needed to qualify for the program. Instead of raising $500,000 to invest, the new threshold would start at $1.35 million. This will help focus the program on pure business ventures and move away from only buying citizenship.

https://conservativedailypost.com/obamas-eb-5-program-receiving-focus-trump-congress-legislators-hammer-500k-loophole/

Until you realize that not that large of a percentage of SFR buyers are foreign AND until you realize that China is in its own massive financial bubble and all it takes is for that to pop, all those trillions of dollars to disappear, and foreign demand to slow here in the U.S.

You are correct. And the Chinese don’t sell. They will keep the home for the great grandchildren. Never renovate. And rent out every room and closet.

This isn’t a joke. It’s true. I live there and I see it.

My income did go up by 450% since 2008. But in 2008 I was in high school and worked in the produce department of a grocery store.

regarding likely drops in prices… if Clinton is trustworthy and prices ease back to 2009 levels, that’ll be about a 40% reduction. I, for one, dont’t that the cpi. If we assume 5% inflation per nnum, then it should be more like. a 20% reduction. And I’ll note that these figures are not going I to account the effects of increasing mortgage apr’s. If we see a price tumble this year he dates aren’t more than a percent point or two higher, a 20-30% reduction would make sense. If tumble doesnt happen until ’18 or ’19 and/or if apr’s get back up o 6+% where they historically were, then 40-60% seems possible.

ugh. Typing on Android…”if Clinton is trustworthy” should be “if cpi is trustworthy”

OK Mike, quick test: what’s 5.0%the most recent year when the CPI was 5.0% or higher?

Answer: 27 years ago.

Housing crash? Hahahahahahaha. You’re funny. Those days are done. Whatever you’re smoking; you need to share cause you’re high. Housing prices are only 1/3rd of the way to peak prices. China is so expensive, Cali is a bargain by comparison. The climb is only at the beginning.

AM Wells.

Time will tell. I’ll give it a few more month, maybe a couple more years. This will be a biggie. And not just here in the US. Be ready for it. Its not a matter of if….but when it crashes.

Wells,

In my opinion this is eventually going lead to major correction due to stagnant income growth; majority of US cities are barely earning and hence inflation is purposefully suppressed. global interest rates are falling. US cannot raise interest rates swiftly.

properties are rising, but incomes are not, many products and consumer index are falling over quarters. people have to pay insurances/taxes every years. all these cannot comes from fixed incomes, so it will eventually going to correct itself and come to equilibrium.

I would say 5-10% year for the next 10 years at least.

Those who think this party is going to end are wishful thinking.

It looks that the world central banks unleashed again the “animal spirits”. I’ve seen this show before and it ended tragically for millions of home “owners”. It is a sad state when people act based on emotions and then they complain about the “profiteers”/investors. Well, in real life investors act based on cold logic and and the speculators act based on emotions.

Like I said before, one of the condos I bought in 2011 was sold at the previous peak for $360,000 (in 2007). I bought it from the bank (foreclosed) for exactly $100,000. It was located in a very desirable area, with only one golf course separating the condo from the ocean. You could smell and see the ocean from the patio.

The large big banks who own the FED did not have to sell to fire sale prices because they were well connected and TBTF. However, the smaller regional banks, did not care about profits at those times. They just cared about survival. $100,000 cash infusion here and there kept them afloat. I had more opportunities like that during those years (2009-2013); more than I had money to invest (although I bought many). A regional bank VP was knocking on my door to offer more deals. However, I am not extremely rich and I run out of cash. Hopefully this time I will have more.

Save money and have connections at smaller, regional banks. The TBTF banks don’t like the smaller banks competition and will do anything they can to kill them. On the next leg down, they will fight again to stay alive.

Do the CEO’s of these small regional banks have golden parachutes? That’d be the only reason for me to believe that they would expose their institutions to such risk for the second time within 15 years.

They have to take on the risk of writing loans, otherwise they’re not going to be a viable business (since the loans are what creates profits for the bank).

I got one of those houses in 2009, but then lost my job in 2010….

I rent in La Canada for $1700 2BD 2BTH with a great view. Next door tenant is paying $2,500. I moved in 3 years ago, they moved in 2 years ago. Point being I cannot get anything close to that rent/buy even if I tried. House prices in La Crescenta, Tujunga, Glendale are beyond what they were in 2006.

Even in 2006 at its peak, the houses were livable conditions. Right now same locations selling for 750k beyong for “crap shacks.” Tujunga TUJUNGA junk is being snatched like gold for 650k.

These realtors sure no what they are doing. Desirable area they list a home for 600k and drive the price to 750k. My wife and I stopped looking. We make 200k+ a year and cannot find a home to buy. Either its junk or we get outbid. Done searching. Let these “smart” investors keep buying!

So what’s your plan? Wait for the collapse? Rent forever? Move?

I’m at > 300k and renting long term seems preferable to buying before an inevitable crash and being locked in.

Please enlighten me on how $200k income is not enough to buy a house. I was making $100k three years ago and bought very decent 3bd 2ba home in diamond bar for $535k and only had to spend 10k to fix it up. I qualified for an FHA loan so only downed about $25k. Sold it 2 years later (2016) for $590 due to relocation to Texas.

200k income is enough to buy a home in many locations. Does not mean I’m willing to go live there. Smart play is to continue to rent where I am until the correction. Saving for the time being. Also, three years is a whole different animal. Can’t compare.

I grew up in La Canada. Have also lived in Diamond Bar. No comparison. Given the choice of renting in La Canada and buying some 40-year-old tract home in Diamond Bar, I’ll take the rental.

Many would argue that the $252K low was an over correction and they’re probably right.

I’m not saying that the main premise of the article isn’t spot on, but I think the true value of the condo in March 2009 was probably higher than 252K. How much higher? I’m not sure.

You have a valid point there Brian. These statistics of median home prices are usually based on homes that have been sold in the last month, not some current valuation of all homes or condos in OC. Needless to say, 2009 was a fire sale…especially for condos that NEEDED to be sold in that timeframe. Regarding inflation numbers, OC RE appreciation has topped bogus CPI inflation numbers for a long time…this shouldn’t be a surprise to anybody. But it sure makes for a good headline.

I too was thinking that CPI isn’t probably the best way to calculate what market prices are or should be. Historically, prior to the derivative scheme that turned home buying into a gambling hall, RE typically increased an average of about 4% per year which is higher than the CPI rate.

That said, the point of the article is still spot on. Condos are the last to appreciate and first to fall, and high HOA’s, taxes, insurance, maintenance do make you basically a renter, just as they do with a house though too. Less HOA usually, but higher taxes. You don’t pay your taxes you lose the house or condo. So really we are all just tenants and uncle Sam is the landlord. Personally I think for us to preserve property rights that needs to be abolished. Thomas Jefferson warned of this 200+ years ago!

If you’re going to use the inflation calculator (which you always should since we’re comparing value between two different time periods) you might as well use it for figures that may go against your narrative. You mentioned that condos reached an all time high recently and numerically you are right but present day value, you are wrong. Present day value of the previous all time high of $470,000 (using the same CPI calculator) is about $577,000 which means that prices still have to climb a whopping 21% to reach that level of mania. Factor in the Chinese investor element strongly present in today’s market than it was back in 2006 and you have plenty of room to climb. You have to be consistent when factoring in inflation Doc! Not just when it fits your script!

Anywho, when the average price hits the $600K mark within the next 3 years, then we will have reached that familiar hysteria. Until then, there is still more room to bubble up. Low inventory and interest rates provide just the right environment for this kind of growth and couple that with the ever so increasing dual income earning households that’s all the rage with millennials and you have yourself the perfect fools, I mean buyers to gobble all of the overpriced condos. And just a note, this year is looking to be one of the strongest years for sellers which means the show is about to begin. I’ll get the popcorn ready.

@ New Age

Well, if you want to adjust for CPI, you have to adjust the wages, too. Based on that, the average incomes went negative in the last 10 years. Even better, if you use the REAL CPI, like they used to in the past, the current GDP is contraction – meaning recession. That is the reason most people feel like in recession.

Why would using a previous price high that was achieved through unorthodox and unsustainable (bubble) methods be any reliable as a barometer for today’s market? Both the previous and current markets were far more influenced by immense credit expansion than by inflation generated through income growth. Thus, the credit cycle would be a better indicator of a bubble high.

On the other hand 2012 was a huge undershoot where evenyone and their mother should have been buying homes hand over fist… when prices were way way under rental parity.

What’s funny is that Jim Taylor started his tank now rant in 2012, exactly when prices started going up up up for 5 years.

Bottom line, flat prices for 11 years is about a 40% drop in prices when counting for inflation.

Inflation is not your friend as exhibited in rents.

@NTS

2012 was no means an undershoot as prices were still higher than what local incomes could support. The low at that time was only reached through extraordinary intervention from the Fed and government.

“Bottom line, flat prices for 11 years is about a 40% drop in prices when counting for inflation.”

let’s say you bought a property 11 years ago for 300k. If the property market price tracks inflation of say 2% it equals 372k after 11 years, right? Can you tell me how you calculate 40%?

I assume you agree with this: Incomes usually rise with inflation and inflation for the last 10 years or so has been 2% in the avg.

@Question:

They are referring to inflation of HOUSING in particular, not inflation of the CPI or whatever measure. In SoCal within 10 miles of the beach in good locations, with low crime and good schools, housing seems to appreciate more than the standard inflation rate from what I’ve seen (though when you look at historical sales prices for a particular place you have to keep in mind whether it was in a bubble or a dip).

$300k over the course of 11 years @ 3.2% appreciation would turn into $420k.

$300k over the course of 11 years at flat would stay at $300k

$300k plus 40% is $420k

I think that’s what they mean. See if you can look around at properties and if redfin/zillow show a current or recent sale, a sale 15 years back, 20 years back, 30 years back. It could give you more of an insight as to how much historical appreciation has been in good areas. I personally feel from what I’ve seen it’s been higher than 2%, and you can see that a small increase to 3% changes things dramatically over 11 years.

So where do you find an accurate CPI inflation calculator?

I currently use that of the Bureau of Labor Statistics, though I realize it’s imperfect: https://www.bls.gov/data/inflation_calculator.htm

I used the same calculator as the one you linked which is the same calculator the Doc used in his article. I used it as an example to compare apples to apples with apples. I assume it’s an accurate enough calculator.

@son of a landlord:

https://www.bls.gov/cpi/cpi_dr.htm

Check out that link from BLS. You can look thru the reports for every month of every year … when you click on the links, you’ll get a PDF. Look at the HOUSING SPECIFIC inflation numbers (right side shows % increase from prior year).

I can’t find a summary, or average calculation, but you can go in and see what it was for all of that time. It seems to me like housing went up at rates higher than 2% a lot of the time…but I haven’t gone through a lot so maybe you can find otherwise?

I live in San Francisco, the Chinese have always been a factor in the housing market here whether it’s 2007 or 2017. House prices here are at 1.2 million, almost double the last bubble, they can do one of three things.

a) Crash

b) Remain level as seen from paragon-re latest research

c) Shoot up to 1.7 mil a la Vancouver fame.

My bet is (b) because of all the easy/cheap/laundered money sloshing around in the world.

HOA’s are evil. The lofty fees collected far outweigh the price of paying gardeners to cut and maintain the property. Those at the top of these associations/schemes must be skimming the hell out of those fees and putting it in their pockets.

My HOA dues are $762 a month. The larger units pay well over $1,000. Who knows how much the penthouse pays?

Most of the money is for labor: 24/7 doormen, 3 on-site repairmen, and 1 on-site manager.

Also includes earthquake insurance, electricity, water, gas, cable TV and wifi internet.

$762 a month for HOA’s? Holy guacamole! That’s insane. That’s more than half of my rent but I do not live that close to the beach as you do. My landlord pays for water. I pay for electricity and wifi….cut the cord a long time ago…cable tv is a rip off and you can stream it all via internet and dvr it on the cloud. In HD quality! And, no doormen here and no manager. Private landlord and a secure front door 🙂 Owner of the units bought during the right time and can rent it out for much cheaper than professionally managed units charge and she still makes a profit.

A well-run, financially prudent SFH HOA has its place (prevents your neighbor from putting a chain link fence around his front yard for that lovely Compton look), but it’s a crapshoot whether you get a good one or a meddling, thieving, vindictive one.

A condo in the inland empire will have (for example) an HOA fee of $200-250/month. The same condo on the coast, with the same amenities, will have an HOA fee of $500-1,000. Okay, so maybe gardeners and contractors charge 30% more on the coast – I’ve seen that. But where is the rest going?

HOAs aren’t evil. Just ask them for an accounting report, sheesh.

i live in “Huntington Bay Townhomes by the Sea” in Huntington Beach. Our HOA is only $545/QUARTER!!! =$181.67/month(+$10/month additional fee for 3rd car parking sticker)

HOA has all volunteer Board Directors (Self-Managed), 3 gardeners, 2 maintenance workers, 1 pool cleaner, 1 p/t Office Manager, HOA Attorney on retainer for fixed cost

All the streets completely replaced 2 years ago and no assessment!

FYI: HOA dues are currently not tax deductible unless it’s a rental property or 2nd home. So buyer beware!

I’m aware their finances are public. I was asking because I’m curious, because I don’t have time to pore over HOA books, and $500 for the same amenities as a $250 complex inland makes no sense to me. No doormen, no guarded gate, just a pool, groundskeeping, and the typical long-term big ticket maintenance. I’m sure the coastal condo accounting is creative at the very least.

That said, any organization that condones sneaking around looking into peoples’ garage windows for violations is evil.

You might want to join an HOA board if you really want to know what is going on instead of bitching about it. Part of those dues is setting aside fees for long term reserves and the other is monthly expenses which you usually can’t escape: insurance, grounds maintenance, water, electricity, security for some, etc..

The other issue you don’t have to screw with is all the things with owning a home sometimes. You let others help assess the repairs while you enjoy your day.

How many of these crapshacks were apartments that got a new coat of paint, appliances and the gotta-have-it granite countertops? Back in bubble 1.0 I saw that happen, and some sold so poorly that they converted them back into apartments, LOL!

Condos are a scam. You can get evicted if someone wants to turn your building into apartments. What if all your neighbors vote to sell when you are still underwater from buying your condo in 2017?

Also we are reaching full employment:

http://www.ocregister.com/2017/04/27/job-growth-to-rise-in-inland-empire-as-it-slows-in-orange-and-los-angeles-counties/

I repeat: do NOT buy into a building with significant investor ownership. These are the people who will vote to “de-convert” to rental if they can scrape so much as $10K profit from the deal. Make sure the complex is at least 2/3 owner occupied. Owner-occupants are usually extremely resistant to any attempt to convert the complex to rental because they will not profit from the deal even if they sell at a considerable improvement over the price they paid, because they will only have to scramble for another place to buy at prices usually inflated beyond their sale price.

Back in 2004 I heard banks were not willing to provide mortgages or reasonable mortgate terms if there was more than 25% rentals in the complex. I find that silly because it justifies the first ones to rent their unit to continue to keep it rented if there is a quota.

These days, 50% investor-ownership seems to be the cutoff for mortgage financing. I was able to score a low price because the building I bought into was 75% investor owned, and I paid cash.

But this circumstance came to haunt me when these owners voted to convert the unit to rental and sell to a single investor, forcing me to sell, as well. So now I am insisting on a building that is no more than 30% investor owned. Ideally, there should be NO investor ownership.

Perhaps another mortgage rule that could put a nail in the coffin for quick flippers would be any condo that is considered a second or investment would have to maintain ownership for a minimum number of years to avoid steep taxes for leaving too early or secure gains. I doubt it would fly but it would certainly put a dent in the condo mania and put reality back into real ownership. This would certainly make it an easier environment for getting a mortgage if the primary resident.

Tanking soon!

Soon is relative. In this case soon = 2030 …. maybe.

I’ll take the bet it won’t tank, not even close.

I’m sure OC is the same way, here in San Diego over half the condos are investor owned. Once some of these RE companies that own a majority of these condos decide its time to sell, I would hope there’s some type of correction.

11 years and condo prices are the same

That’s equivalent to a 40% drop when counting for inflation

You have to wait for 9 more years. JT said that you have to live in for 20 years to see a nominal increase (even if adjusted for inflation and selling costs you lost money).

A realtor friend of ours regularly goes to industry meetups, lectures, and dinner sales talks. He was sharing his horror with us at the type of conversation he hears around the room. Because while technically and legally, lending is supposed to be more regulated in these post-2008 times, there is all kinds of creative lending going on. “5% down on a $75k annual salary? Sure! You can definitely own a $550k condo in Irvine!” What is more, he feels like he is the only one in the room that is wary of these kinds of promises. Everyone has drunk the Kool-Aid and eagerly awaiting salvation.

The psychology of house mania is really something else. After being surrounded by so much insanity, I start to feel like this is normal and I’m the truly crazy one to wait and hope for a leveling off.

Never ever listen to a realtor about lending.

I’m calling BS on this. Almost every loan goes through a federal agency and they’re all being sticking to requirements and verifying with documentation.

Wrong, 100% with sub 600 scores, the new subprimes, its called FHA

Jeff,

dude, lenders have no issue underwriting a loan with low credit score and bogus numbers. Lender dont give two craps if you default or not…by the time you foreclose the loan is loooong sold to fannie and freddie. Come on now…open your eyes.

This is correct; income documentation is required on all agency (fannie/freddie) loans as well as FHA/VA and Jumbo loans.

“stated income” technically exists via bank statements for income (think business owners); but, those loans require a sizeable down payment and good credit. They are also very difficult to get through as they need to fit a very small set of guidelines.

@wake up

This is completely untrue. Just because the loan is sold on the secondary market to a large investor and makes it’s way to fannie/freddie does not release the liability of the originating lender. If there is a defect in the loan and a poor underwrite is done; that loan will be pushed back onto the lender, full amount and any yield paid will be recaptured (and underwriter most likely reprimanded). That loan will need to be sold in the “scratch n dent” market at a substantial loss.

Lenders absolutely perform their due diligence when underwriting to confirm to their investors and the agency guidelines. They don’t just let any loan slip through b/c they will sell it and it’s fannie/freddie’s responsibility; that is not how the industry works.

Moreover, just b/c FHA allows credit scores down to 580 does not mean all lenders will allow it. They have their own “overlays” and guidelines agreed upon by their investors which must be adhered to in order to protect against high risk borrowers.

FHA has something called “compare ratios” and they run stats of loans insured from every lender. If 1 lender has an abnormally high % of loans defaulting they will be penalized for not practicing responsible lending and could lose their FHA/HUD endorsement. That is a death kneel to a lender in this market as FHA owns a large portion of buyers.

I could get more technical, but, I think you see the point.

Last year, I inquired about how much mortgage I could qualify for with a mortgage broker and got approved for a >50% DTI @ 3.5% down.

Here is the exact numbers for you by someone who knows FHA very well:

46.99% DTI max front ratio

56.99% DTI max back ratio

Front = PITIA = principal, interest, taxes, insurance, hoa (basically all debt assocaited with the property)

Back = All debts combined: property + student loan, car payments, credit cards, child support, etc……..)

Where can I find these lenders? I have a relatively high household income, 800+ FICO score, and the only debt I have is just under $10K of student loans left. The only thing that has kept me out of the housing market is the lack of a down payment. I don’t have 20% or even 10% saved up for the houses I’m looking at (not outside of my 401K at least), and if I did 3.5% down through a FHA loan the mortgage insurance is big chunk of change. I’m afraid to apply to any lender just because I don’t have the ideal down payment to avoid PMI.

My rent is eating up a big portion of my income which is the biggest factor contributing to my inability to save (that and daycare for two kids right now) however I could easily handle paying $1500 more than my rent right now for a Mortgage & PITI if I owned a home. It’s just those pesky down payment requirements to avoid PMI.

PB,

You can do 5% down conventional up to $636k loan amount in LA and Orange county (other counties are different). Yes; that will have PMI but most likely 50% less than the PMI with FHA (if your fico is indeed 800). Although, there probably won’t be too much of a difference in payment b/c conventional PMI will be lower, however, FHA rates are always lower than conventional.

So, 4.25% conventional vs. 3.75% FHA is roughly the same payment since the conventional PMI is 1/2 of the FHA PMI.

FHA will ALWAYS have PMI. You can put 90% down and it will still have PMI. That is how they fund the FHA system.

Minimum down required: Conventional 5% FHA 3.5%

Hope that helps.

Full steam ahead, real estate prices are unsinkable. Condos are the last to go up before we hit the iceberg and then it is first mate Francesco Schettino who will stumble into the life boat. This time I will not be a fool and go down with the ship, I am already getting into my life boat along with all the gold in the safe.

Buy any house in sight. This time is different:

http://www.zerohedge.com/news/2017-05-03/gm-auto-inventory-hits-10-year-high-highest-november-2007

(This message brought to you by JT)

Not to worry. The Fed believes that current economic weakness is temporary (as if a return to mediocre growth is anything to brag about). Full speed ahead with the S.S. Rate Hike.

I would never buy an OC condo unless it is located walking distance to the beach, bars, and restaurants.

The middle class in CA is almost gone. Even those with over $100,000/yr income, unless they have lots of assets paid in full, are just “well paid proletariat”:

http://charleshughsmith.blogspot.com/2017/05/redefining-middle-class-it-isnt-what.html

Very interesting article. Exposes a lot of uncomfortable truths as to how we define “middle-class”. Definitely makes one think. I for one believe that the middle-class is doomed in places like CA where our leaders cater to illegals and welfare recipients while championing anti-business policies and railroads to nowhere, all the while taxing the hell out of everything and everyone.

I think the bigger culprit for the decline of the middle class is technological obsolescence and corporatism. We produce and manufacture more with fewer workers. Corporations offshore jobs to save on labor costs or import cheap talent at a fraction of the prevalent wage. ZIRP and QE provided corporations with cheap capital to do stock buybacks and m&a while creating little or no new infrastructure (i.e. jobs) for long term value.

At the end of the day technology will replace all human activity by AI, Robotics, and automation, genome science The only question I don’t know has been determined if all the 1% were left on the earth how many AI and robots would be needed to sustain them? Also with automation simplifying everything from building anything at will you would certainly shrink the entire human population to a small fraction compared to where it is today.

@Hoemrun

That remaining one percent will serve as living batteries for the greater machine intelligence.

homerun: if AI and robotic progresses to the point that the working class is fully displaced, then it will have progressed to the point that all of humankind is obsolete. if we remain, it will be as pets.

Mexicans have not grown much in Orange County the past 7 years while I support cutting down on illegal immigrant. Many conservatives are wrong, its the Asians that are involved in driving up housing. While regulation and taxes can drive business out of Ca there are a lot of liberal tech people who will stay in Ca since they like it. Also, Texas has a problem now with immigration in the big cities. Chinese are drive up real estate values in North Dallas.

For 1,200 sq. ft. in Irvine, I think you’d pay more than 2,300. A quick check of Zillow is showing a range of about 2,350 to 2,950. This bubble is different from the last one because the rents are getting crazy too. The predictable outcome is homelessness, and I’m shocked by the growth of the homeless encampments every time I go by the Santa Ana river. I also find little makeshift shelters, often without even a tarp, when I’m out for a walk on a trail next to my house.

Good point. Sitting out the last bubble in a rental was easy since rents were so much lower than buying a comparable property. Rents have risen drastically and the cost of home ownership has decreased due to the lower prices and lower rates. Bouncing around from rental to rental and getting roommates to save money is likely acceptable for young, single people. People with families face a much tougher choice. Many of just thrown in the towel and bought even if the numbers weren’t in their favor.

The rents are starting to turn in Seattle, New York, San Francisco, etc., so I’d imagine LA and SD will follow suit (although they’re were still up a little in April.)

Here in Portland, it would cost a grand more per month to buy the house we’re renting.

Whoops, forgot the link: http://wolfstreet.com/2017/05/01/the-great-unwind-grips-the-12-hottest-us-rental-markets/

I’m currently paying 1450 for a 1 bedroom in Glendale. Been here 10 years. When I moved in it was 1130. Now Glendale has turned into Los Feliz / West Hollywood. And my landlord is selling the building … soon. What will my new rent be? I’m guessing between 1800 and 2,000.

We’re one of those families stuck renting a place that’s too small for us, but we can’t rationalize paying $1000 to $1200 more per month minimum for a bigger place. We’d rather have that cash in our retirement accounts. Buying is out of the question because prices are so ridiculously insane. So we’ve just sucked it up for now and hope that things get better sooner rather than later.

@Joe

Thank you for reminding us that having a liquid retirement plan is more important than putting yourself in cumbersome debt for the privilege of becoming “home owners”. The bank swill gladly grant you that title as long as you keep up with your monthly payments.

Makes sense to peg rents high now to keep someone from dumping their property and then be potentially punished with years of rates hikes and no tanking in home properties. I think the powers at be are trying to change the psychology in what we do and potentially stem off a crash in home prices.

The bubble rent prices just means that the cheap and easy credit went first and foremost to investors during the current cyle. Too many buyers piling in trying to grab a piece of the finite rentier pie. They overpay for land and/or properties and therefore have to jack up their rates to cover their costs. This “luxury” rental market mania is feeding upon itself as several markets are already suffering oversupply problems.

This bubble is different from the last one because the rents are getting crazy too. The predictable outcome is homelessness, and I’m shocked by the growth of the homeless encampments

1. No. The predictable outcome is draconian rent control laws. Tenants outvote landlords by a wide margin.

2. High rents have nothing to do with homelessness. Santa Monica and New York City both have draconian rent control laws, and much homelessness. The chronically homeless are mostly junkies, alcoholics, alcohol, and/or mentally ill.

I guess two things could happen that might change the situation:

Either a city council head gets paid under the table to enforce these tenant laws

or

Hire the right leaders to do the right thing with no bribe in my opinion.

I wouldn’t call newly, reactionary, local laws regulating that rent hikes be in-line with inflation a DRACONIAN measure. Communities are reacting to a real problem. Yes, some may go too far, and land lords are free to sell their less profitable assets or get out of business it they can’t make it work within the laws – but land barons also go too far in their greedy rent hikes.

You might not like being limited in how much you can squeeze out of the land surfs – but that’s what a society is about. The people. All of them – not the limitless pursuit of an individual’s wealth. THAT is what the board game Monopoly is about. If you think like that then you probably embrace dictatorships. Right? One person has “won” it all and now wields ultimate power. Government’s job is to at least consider the “commonwealth” a tiny bit.

SLynns,

Your are right in your emotional explanation. However, the real life is different. Rent control is proven to hurt most of potential renters at the expense of a small number who were in place and continue to stay in place indefinitely. It hurts the mobile work force who create the economic prosperity.

The real inflation for land, skilled labor and construction materials is way higher than the bogus CPI the government publishes to keep the social security and other entitlements in check. Therefore, without profit all builders will stop building. You should never confuse construction companies with Habitat for Humanity. They are not non-profit organizations. Without profit (lets say 8-10%) nothing moves. In construction, besides the market factors you have heavy government interference at all stages and a construction company could easily lose money; therefore nobody will take the risk and the headaches and the chance to lose money to create rent protected dwellings. No construction for long periods of time creates massive shortages to the point that you can pay over half a million for a studio. Who will rent that studio to you for less than $4000???…

What you say sounds good on the emotional level but the cold hard facts are different. That is why the conservatives do not agree with the liberals – they use different parts of their brain.

Flyover is correct, but we shouldn’t need his explanation to know that rent control accomplishes the opposite of its intentions and absolutely destroys the rental housing market. There is no better way to assure that rentals will become scarce and expensive- look no further than NYC and San Francisco.

NYC’s rent control and rent stabilization laws date back to WW2, during what time there was no construction and all production was geared to the war effort, while San Francisco’s laws are more recent. All cities had rent control during the war years, for wage and price controls, as well as rationing of essential goods, were strictly enforced during that time. However, when the war ended, every city but New York lifted its controls. They were kept in place in New York because of political pressure, and it took only a couple of decades for housing to become so scarce and expensive that people trolled the obituaries in search of upcoming vacancies, while existing buildings became extremely unprofitable and were either converted to co-operatives, or, if the building or neighborhood was not desirable enough, the ownership ceased all maintenance, ran the building into the ground until it had to be vacated, and abandoned it to the tax collector. By the late 60s, vast tracts in neighborhoods like the Bronx, which was a fine middle income neighborhood before the war, were depopulated, the streets lined with boarded-up buildings in various stages of collapse, while rents on newer buildings not subject to controls, skyrocketed, and tenants in rent-controlled units tended to be affluent, well- connected people… which did not stop their landlords from making their lives miserable by refusing to do essential repairs, and subjecting them to nitpicking rules and eviction actions so they could rent the units out at steeply higher rents.

In no city in which these controls were implemented, have they improved the lot of renters or made housing cheaper or more plentiful. Instead, they have made life more difficult for property owners and made owning rental property a losing proposition, and have made life hellish for renters terrified that any minor rule violation could result in their eviction.

Probably true, but Oc has increase. I have said a 100 times to the OC Register support reducing legal immigration since OC would lose population if Mexicans, Chinese, Vietnamese and so forth don’t come there as much. Tom Cotton wants to reduce legal immigration which would put less pressure on rents.

Price controls always lead to the same outcome: scarcity.

I would think that a key component of a “Housing Bubble” as opposed to overpriced housing would be the disparity of rent to ownership cost seen in the 2000-2006 bubble. The high rents may well cause an economic downturn due to lack of money to spend on anything else that will cause a widespread drop in rental rates as vacancies multiply. That in turn should cause a drop in housing prices unless there is a bubble that has taken hold and irrational behavior keeps pushing prices up to the precipice.

In a bubble, it is appreciation rather than income potential that is the driving force. Hedged financing (can meet principal and interest) to speculative financing (only meets interest) to Ponzi financing (need appreciation as neither can be met) to Minsky moment.

Start condo rant:

Condos are nothing but a headache. Majority of the HOA’s are mismanaged and run by schmucks that have no business running a faucet let alone a HOA. When you dig into the financials you will find most HOA’s dangerously underfunded and one roof repair away from financial disaster. Many HOA’s today are not FHA or VA approved because of the higher percentage of renters vs owner-occupiers, making them harder to sell. Speaking of lack of owner-occupiers, If you want to live amongst a bunch of renters who don’t give a sh*t about the community you might as well continue renting, it’s cheaper then owning a condo. Condos appreciate slower and depreciate faster then SFH homes. Condos are always the first to tank and they tank the hardest. Even if you find the perfect condo, mark my words there will come a day when you will regret buying it because the HOA will eventually make your life miserable. When you buy a condo you give up all your rights as a homeowner. A HOA can auction your property off much faster then a bank or the county. Don’t even get me started on special assessments, because they will come sooner or later. I have owned many condos over the years and still own a few, but I don’t buy them anymore. I learned my lesson. Run don’t walk from condo associations. Since the last crash many many condos have been bought for investment property and rented out, this more then anything else has had a adverse effect on the quality of these communities.

Everything you you say is true.

But right now I’m paying about $1,000 a month (HOAs fees, insurance, plus VERY low property taxes) on my Ocean Avenue, Santa Monica condo. I can see the beach from my balcony.

The building sucks. Thin walls. Shared “community washer/dryers,” and lousy HOA. Yet it’s cheaper than renting an apartment in Santa Monica, especially in this location.

And the building is extremely SAFE. With 24/7 doormen, I needn’t worry about burglars. I’ve left for months at a time, and didn’t have to worry about leaving my unit empty.

Zillow says the rental value of my condo is over $2,800 a month, and I’m only paying $1,000.

Well, yes of course because you own it outright and don’t pay for a mortgage anymore. If you would compare renting versus buying my bet is, its much cheaper to rent from a landlord then renting the money from the bank.

How many times are you going to brag about your $1,000 HOA fee?

that’s what it sounds like to me and I can’t figure out WTF you are doing here. How could anyone as successful as you make yourself out to be have found a site like this? If I had half the wealth you claim to have this would be the last fucking place i’d be posting at.

Sorry to detour this post back to LA, but when 30,000 residential units are being built in DTLA, you gotta take notice.

Is there a massive over-build happening or is there a massive demographic flux happening that none of us can fathom.

If there is a massive demographic shift into LA is happening then there is no tank

http://www.aircre.com/downtown-development-explosion-video/?utm_source=01_Requests+%26+Staff&utm_campaign=625d107ac0-AIR+CRE%3A+The+Weekly_05-03-2017_Staff+%26+Requests&utm_medium=email&utm_term=0_88c7d0b230-625d107ac0-114486777

Tech companies and startups are moving into DTLA, bringing with them lots of potential home buyers and renters who want to live close to work. Over the past five years or so it has become “cool” to work and/or live in DTLA. You also have new shopping along with trendy restaurants and bars opening in DTLA. Personally I think DTLA is a cesspool and gross, but to each his/her own.

http://variety.com/2017/biz/features/tech-companies-portal-a-downtown-la-1202028616/

http://www.sandiegoreader.com/news/2017/jan/15/travel-los-angeles-downtown-trashy-to-trendy/

Believe it or not, here’s a link from some Malaysian website talking about how “hip” downtown LA now is:

http://www.themalaymailonline.com/features/article/from-shabby-to-chic-downtown-la-gets-a-facelift

Maybe this might have something to do with it?

http://www.eb5insights.com/

http://www.investlaeb5.com/

https://therealdeal.com/la/2017/01/12/eb-5-investors-are-california-dreamin/

If you make 50K in LA you’re now considered “low income” and are eligible for housing assistance. Congrats.

https://la.curbed.com/2017/5/3/15539770/los-angeles-affordable-housing-income-requirements

Look up above where I posted an article about the disappearance of middle class and the new proletariat at $100,000/yr. People are just blinded by how much they make and forget about the purchasing power. Based on income in Zimbabwe everyone is a billionaire; but how much can they buy with it? If you add all layers of taxation for that “higher” income, the transportation cost, the low purchasing power, you can easily see that person on 100k/yr without assets in SoCal is a serf in a neo feudalism.

When those in power talk about how they’re going to help the middle class and tax the rich, I wonder what their criteria is. I seem to be in a doughnut hole where I always wind up paying more for less. If they remove the deduction for property taxes my whole carefully constructed life will be thrown off balance. Everything Trump wants to do seems to target me. Oh, Canada . . .

Flyover is pretty much right. I make give or take $100k a year as a self employed individual in the SF Bay Area. Looking at the local house prices where I live in San Mateo county I would probably have to triple that income just to save enough for a down payment and to pay the monthly mortgage and overall living cost expenses in a mediocre 1960s crap shack with no yard, nothing fancy.

My new philosophy living here is that it is like living with a different currency. A dollar here is not a US dollar, it is a California dollar. A US dollar is worth about .25-50 cents of CA dollars depending where you are living in the state. The rents, housing values and taxes and just overall cost of living in the Bay Area makes a dollar worth about .20-.25 cents here. Over in Sacramento a dollar is more like .50 cents and in So Cal a dollar is between .25-40 cents depending on the area.

And now in Orange County…..

“A family of four with an annual income of $84,450 or less now qualifies as low income in Orange County. A single person living alone qualifies as low income if he or she earns $58,450 or less a year”

http://www.ocregister.com/2017/05/03/84000-a-year-now-qualifies-as-low-income-in-high-cost-orange-county/

That is absolutely insane. When I first started my career, making 100K was a milestone that you finally made it. Now that amount almost qualifies you for low income housing in OC.

Hello inflation! Locking in a fixed housing cost isn’t a bad idea.

Lord,

don’t confuse a housing bubble with inflation. Oil, products from china, clothing, cars, electronics….mostly everything is getting cheaper. We had only about 2% inflation the past years. Wages go up by that rate. If you perform well, your wages increase is often 5% (at my work anyways). Just because there is a temporary housing bubble does not mean we have inflation. The Fed has not increased rates due to missing inflation targets…(thats what they say anyways). To me it does not matter if housing is artificially inflated for a short period of time. My rent has not gone up in years. By your logic, do we have deflation when the housing bubble burst? Of course not, its just the cyclical boom and bust.

@Millenial

How dare you tear down one of the few remaining rationalizations for buying into such debilitatingly overpriced markets.

@Millenial Crapshack buyer:

Flatscreen TVs and useless garbage from China is all going down in price, however, this is all stuff you don’t need. Shelter, food, energy, transportation are all necessities. These have and will continue to be driven by inflation. And just because your rent hasn’t increased, doesn’t mean rents in general haven’t been rising. The purchasing power of a dollar for things you really need get less and less every year. Betting against this will be very costly…

I was just looking up the median wage after reading something in another thread… it is currently at about 78000 in OC. So the average household is pulling in about 92% of what it would take to peek over the poverty line. It’s ok, though. Even if we were sailing toward iceberg, this ship is unsinkable…

Oh Lordi,

“Flatscreen TVs and useless garbage from China is all going down in price, however, this is all stuff you don’t need. ” Not sure in what industry you work in….at the company i work (multi billion in revenue per year) we assemble most of the stuff in the US but the majority of our components are made in China. The “useless garbage” description is no longer true. I wish it were but that was the story a decade ago. China is able to manufacture quality and durable components. (not across the board but for certain products you cannot find a difference except the cheaper price of course).

“Shelter, food, energy, transportation are all necessities. These have and will continue to be driven by inflation.”

Again, inflation has been very low the past years. Oil prices are down and people use more renewable energy. Crude oil per barrel was about $150 in 08……its now down to less than $50. Keep talking about the high inflation or start looking at some facts/data.

“Again, inflation has been very low the past years. Oil prices are down and people use more renewable energy. Crude oil per barrel was about $150 in 08……its now down to less than $50. Keep talking about the high inflation or start looking at some facts/data.”

Agreed. Much of the recent major inflation has been caused by financial engineering (ZIRP, QE, etc.) rather than by real consumer demand. Current oil prices are reflective of the meager GDP growth.

China’s insatiable drive to build their own ghost towns fueled the commodity bubble. Financing for such gargantuan operations was provided by the coordinated suppression of borrowing rates by the global central banks. The effects of its inevitable deflation (falling oil and metal prices) rippled across the globe, from Australia to Houston.

This Seattle house was listed at $775,000 and sold for $995,000: https://www.redfin.com/WA/Seattle/7711-Winona-Ave-N-98103/home/307000

$220,000 over asking!

SOL, that is common strategy employed in Seattle. I don’t know about other places.

They list on purpose very low to create lots of interest and precipitate an action to be taken fast. Then, they wait at least a week to get all possible offers in the door. Then they decide which one is the highest/best offer and the most liquid. That is how they start a bidding war without announcing an action.

Not only limited to Seattle. This strategy is employed in many cities/markets

so the buyer who paid 220k over asking is having to do that in cash right?

It was priced for a bidding war.

Redfin estimate shows $1M.

The fricken house sold for $2i5K in 1991. What better example of why you should invest in Real Estate? It beats a Stock Market index fund. Of course if you invested in 215K in Apple in 2003, you’d now have 33 Million.

Lets do some math.

If you invested $215,000 in Apple, you have $33,000,000. Your made your money 153 times over.

And, if you bought the home for $215,000, you only needed 3% down,or $6450 down. You made your money 154 times over.

So either investment was the same.

Methinks JT’s never heard of margin buying anywhere else but in RE. Then again, it would make his rags to riches RE stories much less compelling and persuasive.

Prince of Heck have you ever bought stock on margin?

First of all I definitely do not recommend it…

but second of all… it’s not even worth bringing up versus the leverage you get in real estate. You are talking 33:1 ratios versus not even 2:1… and margin calls are cruel with stocks… not for the faint of heart. The game can be over quick.

@NTS

As with any speculative investment (especially the highly leveraged ones), timing your purchase is the key. Margin calls are terrible for real estate or for stocks. It’s easier to say that you won’t sell or walk away when the RE market turns. But to put it into practice is another case.

There have been studies on buying a home with a 30 year mortgage or renting and investing in the stock market over 30 years. The stock market wins.

That math may work in flyover country, no way in coastal CA. When you add in factors such as extreme leverage, tax breaks and shelter being a necessity…I don’t think this equation is even close.

Obama money!!!

“Why rent an apartment when you can own one?”

And lets not forget that you get to pay double the purchase price for that privilege……that is, if you have a mortgage.

Back when i bought a house….at 9.75% i might add……I had the luxury of paying triple the purchase price…….how that is only 9.75% escapes me

I remember the interviews at work. We would bring people in and always ask them if they were renters or owners. If they were in their 20s to early 30s and renting, we let that go. But if they were late 30s or older and renting, we quietly wondered how financially savvy they were.

exactly!!! Renter=poor, Buyers=rich! If you are buyer you are rich and get hired to any job! Buy today, be rich and get your dream job! All you need to do is sign today! Dont be a loser, be a buyer!!!

I would definitely qualify as not financially savvy. Even though I worked my way through college – 35 hours per week – and maintained a 3.5, I had no idea what I was doing when I graduated. I had no idea that back then, in the early 90’s I should have purchased real estate. I had no idea that such a thing was within my reach. It’s something I never looked into mainly because none of my single friends bought real estate. And because my whole life is listened to my parents say they could never afford their house today. It wasn’t until 5 years ago that someone showed me on Redfin what houses used to cost. I’ve been kicking myself and tearing my hair out ever since.

Boxes, that’s the biggest fake post!

As long as you are alive and healthy, you are still winning. If you had bought real estate in the 90s, you would be winning by more. But,you are still winning.

“As long as you are alive and healthy, you are still winning. If you had bought real estate in the 90s, you would be winning by more. But,you are still winning.”

I’m betting that those who bought real estate and stocks during the 1940’s are bigger winners than those who bought during the 1990’s. Heck, those who bought RE and stocks during the 1800’s are the biggest winners of all.

@Fairy Tales, I don’t know if the post is real or fake. But, I do know others who have the story. After college graduation, I mingled with a huge group of recent college grads living the beach life. Out of all these people, only 4 of us jumped in on the beach shacks. The rest ignored real estate and focused in on partying. We also partied, but spend our weekends at the home depot. By the late 90s, beach shacks were flying, so many others became serious and most of those bough inland locations. Very few are still renters. Some gave up and moved to other parts of the US. Seems line the generation just out of college are more fixated on urban living as opposed to beach living. The number of young people living at the beach has collapsed. Corona Del Mar and swaths of Newport Beach are turning into old folks communities. The real action is now urban locations. If the same pattern plays again, you would think those out of college who get in on urban locations will be looking good in 25 years. In 25 years, I will be just turning 70ish, which is too old, so I will not be playing the urban game. But, the urban game is condo that are not in Orange County. Instead, the urban game is condo located in places like LA’s westside and midcity, Boston, downtown Seattle, … you get the picture. So, a replay of my strategy for the 20 somethings might be multiple comdos in urban settings. In 25 years, I will be too old to care, but I will be watching … assuming some a-hole does not start WW3. Personally, in 25 years, I will be amazed if WW3 does not take place. In fact, part of the reason I retired so early is the odds of WW3 is too high to ignore.

“We would bring people in and always ask them if they were renters or owners.”

Yes, employers want to know if an employee rents or owns a home. (Of course, owning means the bank owns it and you pay the bank a fortune in most cases).

JT raises a good point here but as usual its exactly the opposite than what he makes of it.

An employee knows that a renter is more flexible. If we don’t pay the employee well or treat the them well, they can just take another job and move without losing equity/money.

If an employee bought an overpriced crap shack, the employer got the employee by the balls. The employee is a debt slave and has to work hard to make the payments and not lose the house/money.

However, if the employer knows the employee bought during the right time and not during a bubble the employee is flexible because he can move and rent the home to a price that covers the expenses.

It all comes down to buying during a downturn/bust. The worst thing in life you can do is buy during a bubble. The banks sucks the life out of you and your employer takes advantage of it. You are being punished twice for the same mistake.

+1

A good worker is inherently ambitious and will move on because his talents will outgrow the position — regardless of age or of ownership status.

“The worst thing in life you can do is buy during a bubble”. You really can’t think of something worse than that? Even if we confine the topic to real estate? I can think of multiple things that would be worse…

The California Fair Housing And Employment act does not allow you to ask a potential applicant if they are renting or own their residence.

If your company did this today, they could be in violation and you should cease such questions immediately.

Actually, renting or owning can be asked … some legal experts would say it should not be asked since it is not job related, but it can be asked.

My post is considered fake? Why? It’s true. It’s my life. Sorry that my lack of a life plan sounds implausible.

It’s pretty insane in OC. There’s a seller trying pawn off a 6000 sq ft lot for $600k… and get this, there was ACTUALLY A BUYER WILLING TO PAY FOR IT, only to have the sale fall through. It’s back on the market now for $550k. Imaging paying 30 years for a plot of land.

Interesting article about domestic migration within California. Basically discusses how current income levels affect domestic migration patterns within CA and how lower income people are being pushed out of San Diego into Riverside county do to lack of affordable housing. Anyone who commutes on the 91 or 15 can attest to the traffic nightmare this has created.

http://www.voiceofsandiego.org/topics/economy/low-income-san-diegans-are-getting-pushed-to-riverside/

@NewAge

“However, I still feel that the Chinese and Japanese are two different beasts with two completely different factors”

Called it! Of course this time is different!!

“The Chinese have a much stronger economy”

Dude, that’s hilarious! Are you seriously doubting that China is in the biggest bubble in history???

I’ve never owned a condo but what puzzles me is the opposition to HOA fees. Legally, an HOA cannot make a profit on these fees. They are for maintenance such as roofs, sidewalks, exterior painting, etc. There may be fees that you’d prefer not to pay and do yourself like lawn mowing, gardening, community pool maintenance, etc…. All of these items have to be done for a single family home also but a condo owner should benefit on the economy of scale. However, there shouldn’t be any legal skimming going on. Is outright HOA fraud happening and is being prosecuted?

Yes, fraud happens from time to time, as it does in any other type of organization. A large high rise condo near me here in Chicago had its $500K reserve fund, earmarked for new windows, stolen by the board president, who absconded with the money. This would not have happened in an association with strong financial controls and bylaws governing the custody of funds and lines of authority in handling them, or that had transparency and vigilant owners. I repeat, the association should have a 3rd party financial management team, and in the case of large associations, should hire a professional property management team to manage all its affairs. Any association larger than 100 units is far too large and complex to be managed by amateur owners who have to make a living at other jobs, have no training and little experience in the management of large buildings, and can spare no more than a few hours a week, if even, at a job for which they receive no compensation.

This is why I believe that the optimal size for a condo association is 50-100 units, with a minimum of 24 units so that you have enough scale to be able to afford maintenance and repairs and still keep HOA fees low; but no more than 100, because extremely large associations, like giant high rise hives with 500-600 units, tend to become extremely corporate in their management while their owners become apathetic and take no part in their building’s affairs.

In theory, the HOA fees should work in the owners’ advantage. However, in real life it doesn’t work so well.

Yes, fraud and kickbacks are widely practiced. Very hard to proof and prosecute. You can see sometimes 2 similar complexes in the same area and one has double the fees. For example, how can you prove the the subs did not take to restaurants or resorts the guys in charge for higher payments?!???…. This is just a small example; the sky is the limit to the corruption of human heart and what it can devise…

I find it more just straight-up incompetence which derails most HOA’s. The people running them usually have no experience in such things, can’t balance a checkbook and end up overpaying for services, signing bad contracts, hiring the wrong contractors, and generally pissing away money on unnecessary things while being oblivious to the needs of the community as a whole. It doesn’t take long for a HOA to turn bad when the money is mismanaged. Add to that the ever-growing number of units occupied by renters who could care less about the community and soon it all goes to hell.

There are many types of fraud, one kind is to stay on top by paying the IRS and governments correctly and misleading your members with altered books. This is going to keep the fraudster out of jail and land them in a civil lawsuit where the worst that will happen is bankruptcy

Add to this the fact the fraudster was doing it for years, it makes the other board members look like schmucks for not catching it earlier so they cover it up. Rinse and repeat.

All this 5hit comes to a halt when the public perception that whatever you buy today will sell for more tomorrow ends. No different than what happened in the dot com bubble, or in housing bubble 1.0. Its already rolling like a wave over this planet, it just hasnt gotten everyone wet yet, but it will…

J_Kai, agree with your analogy. However, they did not just get wet. They are sunk in debt to their eyeballs. With the exception of some conservative boomers, most people can not longer manage the amount of debt they took. They are not just wet, they are drowned.

A good snapshot of potential buyers in general and those in SoCal in particular:

http://economicprism.com/the-coming-debt-reckoning/

Anyone can pile up debt, but not all will be able to service it. That will cause a cascade of bankruptcies and deflation. While the debt is piling up it does seem that this time is different and sky is the limit to RE prices. However, a time is coming soon when even if the FED will make money available, people will be afraid to borrow and a time is coming soon when the government (at each level) will suck dry each taxpayer just to service the interest on the mountain of debt accumulated.

Remember, money supply is increased by debt (borrowing) and money contraction is caused by paying back debt or bankruptcies. Nobody can borrow to infinity.

Soaring home prices are a sign of a highly competitive and successful local economy

.

JT, since RE prices went up all over the world, it looks that all economies are very successful. I would say, based on your rationale that Venezuela and Zimbabwe are the MOST successful….sarc. OFF

In reality is the Central Banks printing smaller and smaller units of measurement, aka. “currency”. That is a sure way to impoverish everyone who doesn’t have access to a printing press. There is a good reason why the middle class is almost gone.

Shut up and take my money (for your real estate investment lessons)!

@Flyover

Don’t you know that the Dutch became rich from selling tulips (and their derivatives) to each other.

Thank you again Flyover

A San Mateo home–900 sq. ft., 2 bed., 1 bath–just sold for $550,000 over its asking price. Since the house is worth almost nothing, that means that a small residential lot in San Mateo is now worth $2,550,000. There were 17 offers in a matters of days. Does this really suggest that CA real estate prices have stopped rising?

No big deal. Many lots in coastal SoCal are worth 2.5M dollars. Just to list a few cities full of small lots worth much more than 2.5M … Manhattan Beach, Santa Monica, Pacific Palisades, Corona Del Mar.

Thats awesome! That and the one below for 1.6M means a lot of money is going to heaven, never to be seen again as fools fight one another to pay through the nose for overpriced junk. Soooo glad I have a super cheap rental in the middle of a nowhere that I consider paradise. Rock on people!

https://www.redfin.com/CA/Los-Angeles/1600-Steele-Ave-90063/home/6954706

1.6M house in City Terrace!! One of the shittier parts of East LA!

You failed to mention that it has a unobstructed view of the 10 freeway. All that noise & pollution comes at a premium.

That house’s hilltop location provides a beautiful view of the freeway. And as it’s set above any freeway wall, the house receives the full benefit of the traffic noise.

If this house sells for anywhere near 1.6 million, it will be a sign of the apocalypse.

Indeed, I’ve seen quite a few listings “south of the boulevard” in the 818 at this same price point. Comparable sq ft, nicer digs, exponentially better area, larger lots, etc. Why anyone dropping this amount of coin on a house would choose this property is beyond my comprehension.

Real Estate Speed Dating. (the future of romance)

“It literally occurred to me that why can’t we take that kind of app or that style of meeting people and apply it to different things. It works for romance, so I think it could work for a mortgage.â€

http://www.bubbleinfo.com

housing prices still rising!! I pity the middle class american. They are priced out and pushed out of california. most of my neighbor here in alhambra and monterey park are rich chinese and russian people. They bought a lot of property and rent it out to illegal immigrants. This is one of the reason why there is a shortage of inventory here in los angeles.

Alex from San Jose disappears and Wang Bu from Trolldom appears. Bring back Alex.

I recently seen him over at wolfstreet.com commiserating about his 12k a year income. He’s quite prolific, if only he could monetize his comments.

Thanks for explaining that to us Wang Butt. You know we Americans are so stupid and don’t understand such things. Thank god we have you to explain them to us.

I believe we are overdue for a correction in asset prices…BUT

With California laws now mandating loan mods and a high percentage of cash and high downpayment buyers in the last 8 years how does a crash happen?

Only those that have to sell will liquidate, CA foreclosures law now makes kick the can down the road official public policy. Unless baby boomers start down sizing enmass simultaneously I don’t see how this market deflates with any speed or gathers any momentum like 2009.

Thoughts?

Even back in 2009, there was no crash in the desirable area, more like a correction between 10% to 20%. there are too much cash on sideline. if the price comes down 10% to 15%, it just ignites another wave of buying.

As has been mentioned many times around here, conventional mortgages were the majority of the defaults last time around, despite the shady loans getting all the headlines.

It’s really just a matter of an economic collapse, regardless of the catalyst, but it’s impossible to know if it will be better or worse than last time.

Glad to see that a few paid attention to the devil in the details instead of blindly parroting media headlines. More misleading headlines: all cash offers or higher down payments driving RE.

There is nothing in the near term to have the market correct. Well priced open houses have 50-100 people walk through on a weekend. 30 make an offer.

If anyone thinks this is a sign of the market ready to tank – you are kidding yourself.

The market will climb another 5-10 years then level out for another 10 while incomes catch up with the higher prices. There is NOTHING in the market today to push prices down. Supply and demand is a very simple concept. CA screwed up the supply and they make it easy for people who overpaid to get a rebate instead of the home going back on the market for someone who can really afford it. Our taxes pay for those who made stupid decisions.

I’m not a realtor I’m a realist.