All cash buying hits a record in 2012: Parts of Florida see investors buying up 70 percent of all home sales. California all cash buying hit a record in 2012 at over 32 percent of sales.

The amount of investor buying hit a record in 2012. Last year for California over 32 percent of all homes sold for all cash based on property records where no mortgage was recorded with the sale. Some of these homes went to owner occupied sales but the vast majority based on “absentee buyers†signifies that the majority went to investors. The sustainability of investor demand is contingent on the perception of future prices gains. The trend from 2007 has been unmistakable and this is a countrywide phenomenon. Talking to various investors, some are pulling out of certain markets given that yields are weak. Some are still buying into momentum with the intention of selling the place shortly given that rental yields are lower. Keep in mind these are all cash buyers, not mortgaged buyers so lower interest rates only incentivize their actions if there are lesser investment options in the market. I would imagine the rising stock market would pull some investment money back into Wall Street. The all cash buying trend is significant but after five years, will this continue into the next few years?

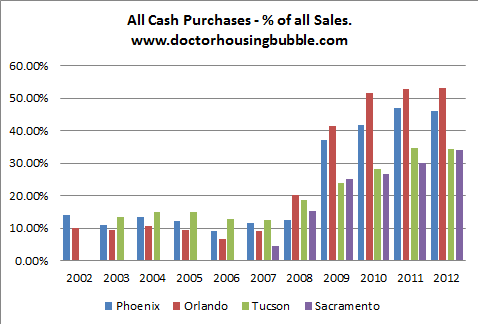

All cash buyers across the US

Below highlights a dramatic shift in the makeup of home buyers across many markets. The perception in the press is that all this home buying is somehow occurring with regular buyers diving back in. That is part of the story but not the critical component of what is occurring. Keep in mind that you also have a large portion of purchases going to FHA insured buyers that can hardly muster a down payment. In California, mixing in the all cash buyers with FHA insured buyers makes up well over half the market. Never in the history of California has this been the case. So let us take a look at what happened after 2007:

In 2002 and 2003 all cash buying in places like Phoenix and Orlando hovered around 10 percent. In 2012 over 50 percent of all purchases went to all cash buyers while in Phoenix it was closer to 45 percent. Sacramento hit a record with 34 percent of purchases going to all cash buyers. This figure almost aligns with the 32 percent for California overall.

What is more telling with the chart above, is how limited your regular home buyer has become. For example, from 2002 to 2007 this segment made up about 90 percent of all purchases. But given the lack of real income growth, many bought homes with maximum leverage mortgages. After 5,000,000 completed foreclosures and a few million more in the next couple of years, the game has shifted. After 2007 a big part of the market was driven by investor demand and has only grown since then. In some markets, investor demand is the dominant force.

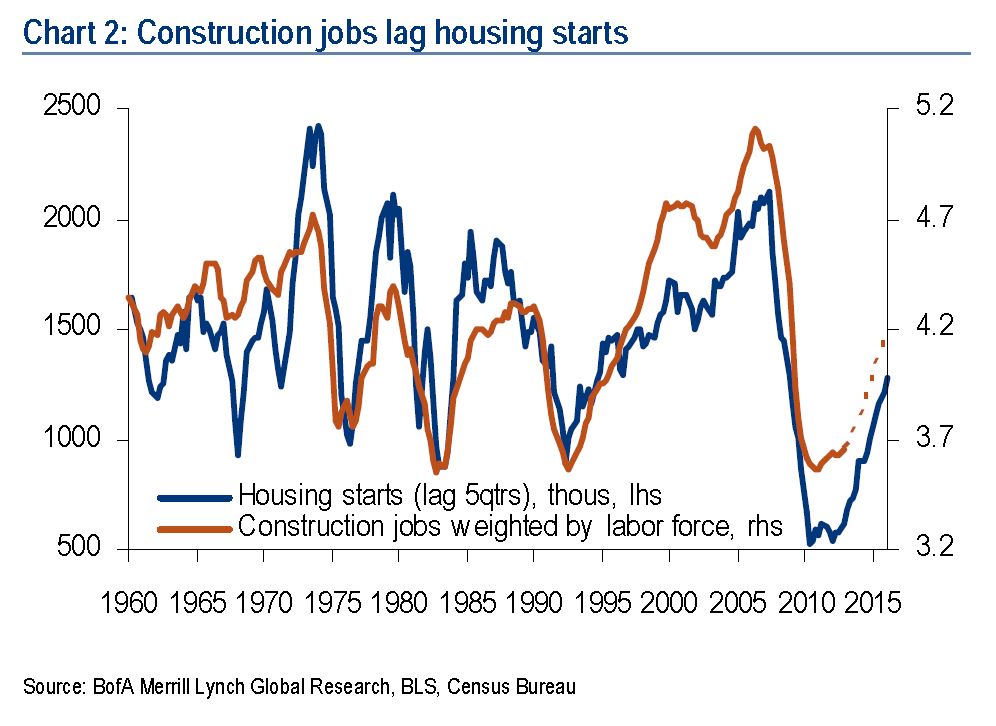

It also seems that with the large number of foreclosures, a slow transition from the over leveraged buyers to investors has happened. That is, like trading cards, these foreclosed homes have slowly ended up in the hands of investors from owner-occupied buyers. How so? Housing starts completely collapsed in 2007 so most sales were for existing properties. Only now are we seeing housing starts pick up:

Today, to qualify for a mortgage you need to document income. However, if 30 to 50 percent of the market is buying with all cash there is no need for verification. Next, you have another 25 to 30 percent of purchases going to low down payment FHA insured buyers that can only afford a very minimal down payment. The FHA to make up for this gap has increased mortgage insurance premiums dramatically.

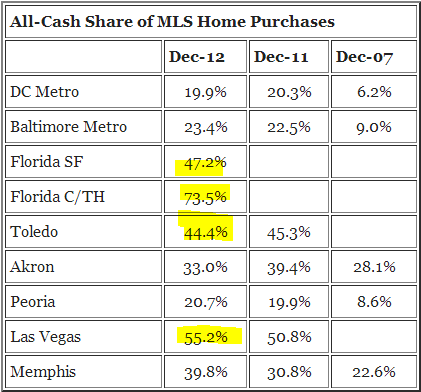

Take a look at certain areas in Florida:

Source:Â Calculated Risk

In parts of Florida over 70 percent of purchases are going to all cash buyers. In Las Vegas it was 55 percent. This is an incredible amount of volume but also speaks to the unintended consequences of artificially low interest rates. Most investment property owners that are in it for the long-haul understand that overtime, your ROI is not as high as you would expect when you first purchase a property. Many over time come to realize that anywhere between 40 to 50 percent of your gross rents will go to other items besides the PI in your payment. But for the all cash buyers, this amounts to 40 to 50 percent of the gross rents which will severely alter the return on investment.

For example, say you buy a place for $200,000 that rents for $1,500. After one year, gross rents would be $18,000. A simple calculation would find:

$18,000 / $200,000 Â Â Â Â Â Â Â Â Â =Â Â Â Â Â Â Â Â Â Â Â Â 9% return

This is not bad but the S&P 500 returned over 13 percent last year merely by holding onto a index traded ETF. Now run the numbers after we account for NOI:

$9,000 / $200,000Â Â Â Â Â Â Â Â Â Â Â Â =Â Â Â Â Â Â Â Â Â Â Â Â 4.5% return

That is a big difference. Keep in mind that a big part of this money is coming from large investment funds so they are capped out on how much tax benefits they can claim on their rental properties. For anyone that has owned rental properties you know that you will have expenses from property management, vacancies, repairs, taxes, occasional bad tenants, legal fees, and other items like replacing a roof or blown out water heater so over time this does cut into your profits. And this is not a passive activity. So many of these all cash buyers appear to be new to the game and time will tell how those yields will look in a longer term perspective.

Some of the much bigger income (i.e., hedge funds) are looking to put these rental payments into some form of security. This is where those added costs will show up over time:

“(Fool) Private-equity firms have been buying up distressed single-family homes for several months now, using pots of money to grab large lots of foreclosed properties which they can fix up and rent, sometimes to the very people who used to own them. Obviously, this venture is turning a profit: Not only are more companies getting involved in the landlord business, but Wall Street is working on a way to turn the income from these rental homes into a new investment vehicle: the rental-backed security.â€

Given how high the volume is from investors, you have to wonder what will happen once yields begin to drop down to Earth. Will investors fight over each other for a 4.5 percent return? For markets where investor buying is over 30 percent, will the organic buyer make up for the gap once investor money slows down?  That is something that we are going to find out over the next few years. If you are wondering why you are losing out on bidding on certain homes, there is a good chance that you are contending with all cash purchases.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Subscribe to feed

Subscribe to feed

78 Responses to “All cash buying hits a record in 2012: Parts of Florida see investors buying up 70 percent of all home sales. California all cash buying hit a record in 2012 at over 32 percent of sales.”

Correct me if I am wrong.

At a trustee sale, if there are no bidders the bank or holder of the note gets the property for money owed. Thats considered a cash sale. The note holder already paid for the house, now they have title to it.

The post is referring to MLS sales. In Florida, ALL trustee (courthouse) sales must be cash. The MLS reports the specifics of the financing used for every sale…Cash, FHA, VA, Conventional, etc. In Palm Beach County, in 2011 and 2012, 65% of all MLS sales were reported to be cash sales…it is tough for a buyer to compete in that enviornment.

As we saw recently, according to the Feds, the GDP decreased at an annual rate of 0.1 percent in the fourth quarter of 2012. This was (again according to the Feds) because a cutback on defense spending. And so there you have it. We’re in check maybe checkmate. Increased tax’s or decreased Government spending or a combination of both have the same effect; less disposable income. This all has a cascading effect, less tax receipts mean higher deficits, which in turn leads to less Government spending, so less Jobs. The music will stop and when it does, watch out. Now what’s my home worth?

@THETHOUGHTPOLICE: “GDP decreased..because a cutback on defense spending…Now what’s my home worth?”

If you are in SoCal, no change. The Feds shut down Long Beach Naval Station, El Toro Marine Corps Air Station (Irvine), George AFB (Victorville), Norton AFB (San Bernadino), Marine Corps Air Station Tustin in the 1990s. In addition a huge chunk of the defense industry jobs were also sent from SoCal to Missouri, Texas, Virginia, Georgia, Alabama, etc. during the same time period.

Any slowdown in GDP due to defense department spending cuts will likely hit Virginia, Texas, Missouri, Georgia, Alabama, etc.

Defense cuts will have have a major impact in San Diego county as well as south western riverside county. San Diego is home to multiple military bases and tens of thousands of employees.

Actually, San Diego has lots of defense related industries. As far as the economy, my point was the fragile nature. It won’t take much to send it into a tailspin. My belief is it will soon, but who knows, as no one knows where the top is and no one knows where the utimate bottom is…

Hello Earnest

with the loss of aerospace and defense jobs, there has been an influx of jobs and technology also. The so-called Silicon Beach is right here on the Westside. My guess is many buyers in 2012 and 2013 will come from this sector. For example, venture capital into the LA is second behind Silicone Valley. When I was renting an apartment in Santa Monica, the neighbor above me and neighbor next to me were both engineers at Google.

http://www.forbes.com/sites/ciocentral/2012/08/28/why-los-angeles-is-emerging-as-the-next-silicon-valley/

http://www.bizbest.com/insider-guide-to-silicon-beach/

http://www.represent.la/

I saw a report last week (wish I could remember where) that Virginia would be first in job loses, followed by California.

You are assuming housing is a free market dictated by incomes when all these articles suggest that it is a manipulated market based on debt that can be socialized. Incomes have largely been replaced by debt, which enriches wall street while the risk is passed on to the taxpayers. This has been going on for a while. All the military bases were closed in the bay area in the 90s but housing prices went through the roof as debt loads were increased and dumped on the taxpayers. Now the banksters have moved in a big way into the landlord business and their incentives will shift from selling us debt we cannot afford to keeping us renting as long as possible. Families are totally screwed by this system until government of the lobbyists, by the lobbyists, and for the lobbyists shall perish from the earth.

Hello Doc

Curious what makeup of these all-cashers are simply buying forecloresures or other un-listed properties? in other words would it not be interesting to see how many of those buyers who intend to be owner/occupiers are all cash. Makes perfect sense if the majority of all cash buyers intend to rent it out or flip it, however, as an active seeking buyer myself (owner-occupier) am I going to be competing with all cash offers? If so, doesn’t it tell a different story about the state of the economy?

If I had to choose:

1. Liar loans

2. All-cash speculators

Me pick “all cash”.

Do some cash purchases, later get a loan for the property? Then secure more properties with cash first? Doesn’t seem fair if that is the case

Responding the question about buying cash first, then get loans, then use borrowed money to buy more properties all cash.

It is happening even with the so call “Big Cash” Chinese buyers in Socal. The Chinese realtors are teaching clients to buy all cash, then getting a HELOC (due to minimal income and background verification and fast approval process) for as much as they can, to buy another property all cash, then another….. I know, because a friend of mine who recently bought a $380K house in Rancho C.M. (and renting it out immediately for $2150/month) is already on the lookout for next property. Problem for her isn’t getting the HELOC but finding more properties (inventory problem) and bidding (because of all other cash buyers).

So don’t think these Chinese buyers are coming with unlimited supplies of cash. They are mainly using the first pile of cash, then leveraging using American banks (our hard earned $) to buy more.

That sounds similar to how the last house of cards was built…..

@CJ

Apparently, your friend that bought the house for $380,000 and is renting it for $2,150 a month is not very good at math. That is only a 6.7% GROSS return on investment not including other expenses and set asides for vacancy. Plus renting out property is a JOB, not a hobby.

Hello Bren more on this ‘all cash buyer’ term. I found out from a realtor friend that many buyers today are going in with an ‘all cash’ initial offer but at the end of the day the buyers are in fact getting a mortgage. Many listing brokers today would rather deal with the initial buyer who (falsely) claims he is all cash then terminating escrow and putting the property back on the market. As you may know, often times when a property falls out of escrow the property gets a ‘black eye’ and subsequent buyers will be suspicious of the property (ie: why did it fall out of escrow???). But for many of the real “all cash buyers” who intend to own-occupy are retirement age boomers who are funding their kids first home purchase. For myself, one of the key questions seems to be: what percent of owner-occupier are truly all cash… 10%? 20%? even if 10% seems like it would tell of an improving ekonomy.?

Overseas Chinese buy US real estates to (1) preserve value of $ in US$, and (2) make some income, and (3) get some beneficial use (sending kids to US for free schooling, vacationing, etc.).

So 6% is like found money to them.

Back home in China or Taiwan or Hong Kong, properties are so expensive and yet rent so low, most properties are sitting vacant (rent < costs of having tenants).

Oversupply of rentals on the market means a decrease in rents going forward. These guys are going to bail when rents bail. Housing bubble 2.0 comes to an end. I predict lots of blood-letting in 2014 and 2015 for the landlords.

That’s an interesting statement. Will the hot money bail as fast as they came? Can they bail out as fast as they came in? It’s not certain they made ANY money on the whole Fed RE bailout in the long run.

Fed opened the gates and hot money may have flooded in to support it. Banks are more than willing to sell. I don’t know if the hedge funds have the attention span and management infrastructure in place to handle the micro management. I guess the Fed figured that they can always kick the can down the road and find solutions when needed. Given current ZIRP and low inventory from foreclosure moratorium, it will be interesting how they will handle this.

Of course, there is always option to re-package loans and sell them to non-domestic trade partners.

When I see “buying into momentum” I imagine somebody who will sell to the next person who will buy into momentum at a higher price. That blows a bubble that will pop after the early buyers have run through the entire pool of suckers. Collapse depends on rental money being inadequate, but it’s not that that will suddenly happen; it will have been there all along.

Adding securitization, I don’t know what to think. This could be a game of quidditch, it has so many different moves.

I’ve always used the lousy market in Florida as an example that Boomers in the north cannot sell and move. Maybe, just maybe, this is a sign that the markets in the northeast are picking up. After all, an empty nester couple who own outright or didn’t hit the HELOC train in the last decade probably have a large amount of equity to cash in, and can easily pay cash down in Florida for a nice little thing in the 200-300,000 range, which would buy you a palace down there compared to their crappy older cape cod on Jersey or Westchester that bubbled up to 500,000 and more, and still hasn’t dropped much. I’m not saying that they are a majority of the market, because most up north have no equity and savings to speak of, but, they have to be part of the market. Wise move, you have to admit. No state income tax, warm climate reducing wardrobe costs, no need for a snow worthy car, and excellent senior health care. Love those early bird specials, too.

Anyway, at this point in the market crash, having big money investors come in and buy is good news, in the end. Who else would? Mildew can destroy a home down there very quickly, and it’s good just to have some “investor” buy in and turn the air conditioner on to dry things out. Florida has probably seen a bubble bigger than the one in the 20s pop, and that one took decades to bounce back from. It’s traditionally a speculators market, because, hell, there’s no employment down there to justify the amount of building and pricing. They just hope that northerners will show up to die there in large numbers, escaping winter for the last few years of life. The numbers tossed around above make me laugh, though. $1500, for a 200,000 home. What kind of job down there will justify such a housing cost? I’m guessing the average income outside of Miami is maybe 30,000, if that. And, as mentioned, how about all of the costs of maintaining that home? Anybody expecting 8% on their money without living very close by and doing most of the work themselves, screening and paying attention to tenants religiously, will be very disappointed in their returns, I’m pretty sure. But, why even bother? I’ve seen over 8% return in my IRA over the last five years, just sitting at my computer and investing fairly conservatively. Stock market looks good for ’13, too. I mean, where else are people going to put their money? Old houses a thousand miles away? Who needs the problems?

One very large issue with owning real estate in Florida is the cost of home insurance. It is going up and the state is getting out the subsidized hurricane insurance business. What do you think will happen to the cost after the next way overdue category 5, Andrew, comes plowing into a place like Tampa? Additionally, as the boomers age and cannot take of themselves, who in Florida is going to take care of them and what happens to the house with no relatives around?

dreamers…taxes for non residents incredible water costs.mandatory pool maintenance …exorbitant taxes from a legislature owned by insurance companies, incredible mandatory auto insurance …dangerous to be hospitalized in florida, crime corruption …mandatory lawn maintenance …huge police presence …loking to write tickets on anything….welcome to the shooting gallery of south florida ..you have to be

armed here remember the cops are only anhour away i retired here 20 years ago BIG MISTAKE

Remember when people used to simply “buy a house”, buy things? Now they (lower voice) “purchase a property”. Everything is a “purchase”…”I’m going to purchase toilet paper”. What’s the next buzzword to fancy it up? “I’d like to secure a property”, “I secured a hamburger and fries today”. Hahaha…

Lol love it!! How about this one. “Let’s socialize internally on that. ” it means to meet w your co workers and talk. Lol who makes this crap up??? Someone named Bif or Muffy no doubt.

Hey Drinks – Thanks for making me laugh today!

Rule of thumb is when over 16% of the houses are rentals in a neighborhood, that area will deteriorate…get run down. Renters do not maintain their property like an owner does since he has no stake in the property and is a shirt timer. This hurts the surrounding house owners who will see their values drop even more.

These investors may turn a profit but the neighborhood is a lose-lose situation for long term house owners.

Ok, hold on Mrs. Ming — let’s get clear about something.

Other than regular landscape care (usually renters responsibility) the maintenance of the home is the OWNERS responsibility. It is the rental OWNERS who let the properties go downhill.

@Good One

You are missing the point. In the case of rental property, neither party, the renter or the landloard, have the same incentive to keep the property in good condition as an owner would do. The 16% is a statistical norm. Go against it at your risk.

@ Jeff Beckman – there was no Reply Link in your comment box so, it looks like I’m replying to myself!

No, I didn’t miss the point. I understand her drift but I think clarity is important. I continually hear people refer to the subpar condition of a property because the renters don’t take care of it. That’s an incorrect statement.

The more accurate terminology would be that INVESTOR OWNERS don’t tend to maintain their properties well.

Thank you!!!! For pointing out REALITY.

It is the OWNER’s responsibility to maintain the house!

Of course renters don’t have an incentive to pour money into an asset that’s not theirs!

DUH!!! That’s a no-brainer. It’s also very stupid to make an innuendo that makes it sound like renters are lacking morality or something because they’re unwilling to pour money into an asset not their own!!!

Not the renter’s fault if they’ve got a deadbeat absentee landlord!!!

Not the fault of “renters in general” if some landlords fail to maintain a relationship with their tenants to ensure any agreements are being upheld about grounds keeping, etc.

@ Jeff Beckman

The point is not to dispute the 16% statistic, but to dispute laying the blame on the renters:

“Renters do not maintain their property like an owner does”

If the comment was “renter-occupied properties don’t get maintained like owner-occupied properties”, that would be different, and there would be nothing offensive to object to.

The comment, however, made it sound like ALL owners like to maintain their properties, just that their slovenly immoral renters do not.

I would be happy to maintain your home. But you would have to rent to me for 150 a month not 1500. No typo And you fork over the material bill. Not a bad deal really if you think things are going to change.

…but Wall Street is working on a way to turn the income from these rental homes into a new investment vehicle: the rental-backed security.â€

Meanwhile, the federal watchdogs at SEC are in deep slumber

Watchdogs? What watchdogs? Maybe the poster is referring to the wh0res who slide through the revolving door to the private sector…

http://www.huffingtonpost.com/2013/02/11/sec-revolving-door-wall-street_n_2648355.html

I know, I read about that it’s frightening isn’t it?

I keep saying, people who made mad money during the housing bubble are DESPERATE to get that bubble back. And if allowed, they will do it, and more mayhem will ensue.

I wonder how many times they can do it within a certain time frame before everyone says enough is enough?

The institutional investor capital is likely a manipulation to drive the market with an artificial outcome common to FED led banking sector actions like these

Know the game if you’re playing on this field- it’s not a private investir’s home field

Janum, having owned rentals for 20+ years, the only time rents went down was when people actually left the area in large numbers. If people are not leaving, they still need a place to live, once they get foreclosed on. I have a buddy that bought a REO from BofA in the Bay area and the former owners became his tenants. For the cash buyers to pull back, we need other places for them to put their money other than a bank at 1% or less. With the stock market at these levels, who wants to come in with a bunch of cash? It is smarter to look for bargain areas to buy RE in as rentals and will likely stay that way for a few years.

Jim, you are looking at the Demand side. There has been a net outflow of people leaving over the last few years. My comment was about the Supply side. Lots of homes that were/are sitting empty will become rentals soon. The much higher supply and lower demand will lead to lower rents. We’re already seeing happen in eastern Ventura county. Rents have dropped 10%+ in the last few months.

People don’t even have to leave the area – sometimes they just move into a parent’s basement, share an apartment with a friend, etc.

I think I will stay in stocks because I believe most people are thinking as you are talking. Although i would watch for a bond market collapse before i would watch for a home price collapse in most states.

showing a 9% return makes people pay attention, but where are the annual costs such as real estate taxes?? That certainly knocks 2% off the 9%. Also, if maintenance is deferred, rents will either go lower, or as the Midas man says..we can get you now, or later–have to figure at least 1% for maintenance, then, I doubt anyone doing this stuff will manage the property themselves, so there is 2-3% minimum for management. The biggest surprise of all is when these properties go DOWN instead of up.

The only reason to think prices are going up is if you see homes being built next to where you live in abundance. I see people leaving where I am. not because it is over grown but because there are no jobs to compensate for the rent being asked for.UNless you manage a Mcdonalds you don’t make any money . I don’t care if you do have a useless college degree. That college degree has been financed by the public taxes which is why your cost of living has increased. And teachers are not interested in teaching . They are interested in surviving just the same as doctors and lawyers who in large part have useless jobs. We are in a hyper inflationary environment which is being manipulated by liars and ignorant politicos. For every smart liar there is thousands of people willing to listen to him her.Remember that psychology class. Almost useless unless you went on to graduate school and if you did you don’t own anything in this kind of environment but your knowledge.

Lol you KNOW those large brokerages are going to over sell the “rental securities” (I do believe that is an oxymoron) then strip the profits up front in fees (banks win either way) and in the end homes will be forclosed, investors will lose. I am sure the bankers are hedging their bets on these rental securities as I type! You have a better chance blowing a wad of dough here in Vegas at the casinos. More honest too.

Article that says it true: “Home Investment A Fad” by Robert Shiller

http://www.businessinsider.com/robert-shiller-home-investment-a-fad-2013-2

Why would JP Morgan Chase, Morgan Stanley,Goldman Sachs and bunch of other mega hedge funds jump onto the slum lording bandwagon business? What is the future of private property ownership in America anyway?!! Think again?

@JB – as has been stated above…the investment banks you mention would be doing so to broker securities created around pools of rental properties. They won’t own the real estate, they’ll just collect fees selling the bonds backed by that real estate. It’s much better….no risk, just fee collection.

As for the future….well, stay tuned. But, you may like going on Youtube and sourcing any video interviews of Robert Schiller to get a decent idea (a walking knowledge-base about real estate in America)

Right,right…but something is still fishy here,no?

http://www.newrepublic.com/article/112395/wall-street-hedge-funds-buy-rental-properties#

@JB – you made me chuckle. As a former Wall Streeter I can tell you — there’s fishy happening everyday in that little universe! Read: The Big Short by Michael Lewis for a very accurate picture into that world.

Your link — I had 2 primary thoughts when reading it:

1) It sounds like these institutions are now competing with each other for these properties. Well geez, pretty soon the situation will be moving into ‘the greater fool’ territory. Never pretty.

2) The owner-occupier foundation of the single family home market will not be strong with so much corporate ownership. As the article and others have stated, with high unemployment, stagnant wages, many boomers wanting to trade down from the crazy McMansions they bought, others just re-evaluating what ownership means (or doesn’t) to them (me), lots in 20-30’s age with mountains of school debt to pay off first —- where is the big pool of owner-occupiers with strong jobs, some savings and an interest in staying at least a decade going to come from? They create the market stability. Instead, the institutional buyers will bring plenty of volatility….it will be unsettling.

I have a question about appreciation. Before all the junk went down, on average real estate appreciation was something like 3%. What was the fundamental pressure that dictated that growth? Was is wage inflation? Was is GDP growth? Or, more than likely, some combination of these and more? Population growth vs. new home building growth, etc..?

Say a house was fundamentally worth 200k in 2005, but it sold for 400k because of the bad loans, etc. And say those fundamentals were working in the background ( even though the signal to noise ratio was too small to detect such properly in the short term) over a 10 year period to 2015. If the signal was fundamentally 2%, or 3%, would not that justify the house being 243K, or 268K at 2015? 269K, or 311K by 2020?

Or, because of wage stagnation, pending deflation, etc., would the background signal be flat as well, and thus there is no way to justify RE appreciation?

Well, fundamentally, demographics have driven house prices over the last thirty years, as the boomers entered the market and age, laddering up to MacMansions. Now that they are dying off, well, sorry……..

This group (JP Morgan Chase, Morgan Stanley,Goldman Sachs) is responsible for creating an environment for cheap money-credit and easily mortgage financing that suckered people into a feeding frenzy that inflated the housing bubble. It was greed, greed, greed.

Now the same group is milking the system on the way down as the bubble deflates (the subject of the current article).

There is a role for government and a role for the private sector (in economic activity) in a careful balancing act. When the role of government is controlled by private sector companies, as it is now, the role of government is over and balancing act is broken. Our current situation is one of greed raging unchecked.

JP Morgan and Bank of America are my best performing stocks of 2012. BAC is up 74% from when i bought it. JP Morgan is up 48%. But if this were 18th century France, I’d be the one operating the guillotine on ’em.

well the good thing about all cash buyers is if they need cash they have to sell a what ever price they can get,no bank to answer to,no giving back the keys and walking away.

2005 – “Oh! Don’t buy a house because of the bubble”

2013 – “Oh! Don’t buy a house because of the low interest rate fiscal cliff bubble”

20?? – “Oh! I died, life is finite, and I never did buy that house. Sure wish I would have done that because in the end it doesn’t really matter.”

or, 2030 – “Wow, lived ten years longer because I didn’t have that stupid overpriced house sucking energy out of me every time I turn around to take care of it and thousands out of my pocket that I could have spent on heath care and happy, fun, relaxing activities.”

@Papa Now – your statement is vastly simplistic and, honestly, clearly written by someone who hasn’t owned. If you’re looking for it to provide you with some deep sense of fullfillment, I think you’re going to be disappointed.

There can definitely be a feeling of satisfaction and comfort to have a place of your own and make it the way you like. But, it will also be very time consuming to maintain and as a friend of mine says, “a black hole for money”.

So, like most things in life…there is both pro and con. And if you’re going to read the internet you’re going to hear both sides. And that’s a good thing.

There’s more to life than owning real estate. Your argument reminds me of people who insinuate that someone’s life is worth less because they didn’t have children.

The “life is finite” argument cuts both ways. “Life is finite” also means you don’t want to waste 30 years of it slaving away to pay off a mortgage on a property that will be worth 1/4 as much as you purchased it for at the end of the 30 year period. And there are no shortage of people who purchased houses at the wrong time–that are now finding themselves trapped inside 30 year mortgages and living day-to-day with the perpetual fear of losing it. These are people who constantly regret their purchasing decision, because it has effectively made them a slave to their own property.

For example, my college roommate, an accountant– committed suicide last year — he would have been now about 15 years out of college. Years ago, he stretched to buy a house in Arizona on a 30 year fixed year mortgage. Unfortunately, during the crash, the price of this house plummeted to less than half of what he purchased it for. Rather than sticking around 26 more years and slaving away to make the mortgage payments, he decided to walk away from it and just take the credit hit.

He then found a new job as an accountant in a different state. But he grew to loathe his job as an accountant and wanted to switch careers. But he couldn’t take out the requisite educational loans to go back to school, due to his bad credit. He felt trapped, with no way out… The decision to purchase a house has significant real world consequences..

I recognize that a case can be made for people “over-waiting.” But when you have a market like this one…with data that is inconsistent with historical trends, evidence of market manipulation, flippers, all these cash buyers floating about, overbidding wars, and the FHA loans, coupled with the fact that for most people, owning a house will be a more expensive transaction than any other purchase they will make in their entire lifetime (in the hundreds of thousands of dollars), any mistakes or smart plays in this field are magnified.

You might be able to stomach getting short-changed $5.00 at McDonalds drive-thru last Saturday, but when you instantly lose $80,000 in equity on your house because the interest rates rose…that’s a different kind of a feeling altogether.

Patrick – you are a very sharp cookie and an articulate one, to boot.

Thanks for sharing your very poignant, REAL WORLD story. It reminded me of one:

A woman I know, about 57, a business consultant who makes good coin when she has the work. About 2006 she decided to move to another (more expensive) part of town. She had done nicely on the house she sold and her business flow was very good. It was a egotistical era, as we all recall, so she decided to add lots of remodeling bells and whistles. I’m thinking over a one year period she ploughed 100K into this more expensive house.

Well, 2 – 3 years later the economy craters, her biz contracts dry up and her house declines in value probably 200K. She was like a deer in the headlights and went into therapy. Actually I barely saw her for about a year, she just retreated. I empathize but, the truth is, she did it to herself.

I think she’ll be okay, she’s a good saver, still has the house. But note the age I mentioned. Unless you have millions, no one wants that kind of hit while moving toward retirement. Scary.

**OH, WAIT, let me also describe something I haven’t seen anyone mention. For any first time buyer itching to buy……IF you’re thinking ‘well, if I lose my job and can’t pay the mortgage, I’ll just sell”. Yes, that’s an option. However, has anyone given you the real skinny on selling? Then let me…..it’s an absolute BITCH!

It is vastly time-consuming, humbling and you…are…at….the…mercy…of…the…. buyer….AND….THE…AGENTS! If you don’t think you got screwed after a transaction, it’s only because you don’t know HOW you did. I wish that horrid exercise on no one.

According to your story, your accountant friend killed himself because he couldn’t stand accounting. I really doubt that this was the reason. I know that it is tough being an accountant and it is not for everybody, but I never heard of anybody killing their body over it. In regards to the point you are trying to make, real estate is not for everybody. In fact, close to half the people rent. There are many good arguments to make for renting for the next decade or more.

You used to be a huge housing skeptic, but now that you’ve bought you constantly come on here and seek to justify your decision. I understand why you bought, but you’re starting to sound a lot like others who’ve come on here and seemed to be trying wayyy too hard to make themselves feel better about their own personal financial decisions.

sorry, my full name got cut off last message.

Do you have any land out back for gardening, Papa? If so, you’ll be glad you bought, 10 years from now, when the real price of food had doubled, and you have the option to put a few vegetable crops in the ground to offset food prices.

In Germany, the price of a 4KW solar electricity kit is about 8K. In the U.S. the same kit is 20K. But give us some time, and we too will see cheap solar as an option against the rising price of electric energy. At that point also, you will be glad you owned a home.

Again, as gas/oil prices stay high (remember fracking is only profitable at $75/barrel), and electric vehicles get cheaper, you’ll be glad you own a home and don’t have to fight a landlord about installing a quick charge vehicle hub, if you eventually want to go EV as a hedge against that.

The long term trend is clear: fossil energy is getting expensive, while renewable energy is getting cheaper. Owning a home puts one in a good position to take advantage of this trend.

all excellent points, but depends greatly on

(a) where one lives in relation to their work/supply chains,

(b) the energy efficiency of one’s home,

(c) the source/availability/quality of the water,

(c) the quality of the soil or the desire/knowledge to remediate it.

now how many buyers factor these into the equation when choosing a home?

So buying a house is a must now? At any price?

Even companies don’t buy the houses they use, those are mostly rented and the capital freed for better investments.

I can’t see any sense of tying $300k capital into walls for all of my life. Especially when I would have to pay another $300k interest to bank in order to get it and all that from heavily taxed salary.

It’s not a mortgage, it’s a slavery deal, for 30 years.

Something to think about.

http://blogs.the-american-interest.com/wrm/2013/02/11/california-cheating-young-with-toxic-bonds/

oh Papa, you have a very short memory… why don’t you look back further at income to house price ratios.

Many of us want to buy a home but can’t afford to pay 500K for a fixer upper starter with a couple of kids in daycare even with both people working, because the economy is not so great where you can rely on having a job 6 months from now.

You go ahead and buy though.

Betty, you are absolutley correct, and the scenario you put out is true.

But what I’m saying is a different tale, with a different set of circumstances. For example buying a $250k home instead and commuting. Join a vanpool with workplace subsidies on the cost. No not everyone is in that group but then again I don’t understand how Rancho Cucamonga is supporting a $400k+ home price in many neighborhoods either. Some money is somewhere…

PAPA – Life is more than a house. The fact (as you say) that life is finite should tell you that. You’re not gonna take it with you, and buying a house isn’t a magic ticket to happiness while you’re here. You’re right, IN THE END IT DOESN’T REALLY MATTER if you bought a house or didn’t buy one, does it?

I just took a look at listings in San Francisco, which has always been one of the priciest locations in the U.S. and WOW was I ever surprised.

Something very strange is happening in San Fran. I am really, really surprised at how LOW the prices are, and for very nice, large one-bed and even two bed places. Now, I have no idea about the neighborhoods they’re in, but when I looked at listings there in 2005 at the bubble peak, the cheapest listing was a tiny studio in a rather run-down and un-rehabbed Victorian for $300K plus.

Those of you posting here who are familiar with San Francisco: how are zip codes 94103, 94124, 94019. 94109. and 94132? Are these super-reasonable condo listings for real and do they sell for these prices, or do they get bid way up? I’m very curious.

Thought I should share how the owners of condos (rented to students) violated housing laws by turning two bedroom condos into unsafe 4 bedroom condos. I imagine this happens all the time, being one of the ways to charge exhorbitant rents.

http://www.sanluisobispo.com/2013/02/12/2391281/pine-creek-condos-inspection-unsafe.html

And, the Pine Creek condos shut down by the city (see my post at 12:55 am) rent for $2400 to $2800. They are supposed to be 2 bedroom, but have been converted to more bedrooms (which commands higher rent). All the units were in violation. Woe to the owners who bought in 2006 for $400K.

Sorry to relish in slamming the landlords of the Pine Creek condos that were shut down (see my post at 12:55 am), but I have found several sold in 2006 in the upper $400Ks, such as this one for $495:

http://www.zillow.com/homes/1185-foothill,-san-luis-obispo_rb/#/homedetails/1185-E-Foothill-Blvd-APT-14-San-Luis-Obispo-CA-93405/15426472_zpid/

Someone made bank on the sales and the owners are going to be losing big time, considering the retrofits, loss of exhorbitant rent, and the fact that they’ll be lucky if they can sell for $325K.

I want to clarify one thing about my opinion. As some have stated, yes I was a huge housing skeptic, and with reason. But the simple reason my opinion has changed (although I HATE the reason it has) is because the Gov changed. Simple. They enacted policies of social and fascist proportions that no capitalist saw coming, although some historians did.

What I’m actually doing is looking past my bias confirmation, and looking at a corrupt and manipulated market that I have no evidence will stop. I don’t see fury in the streets, I don’t see the revolution that some predicted, even though I somewhat bought into that the last few years.

What I see is continued socialism, and until that is fought by the people, I see no reason for this market to do anything other than chug along this new status quo. And the reason I don’t see a “collapse” is because SoCal is a desirable place to live. The job market and regulations may be horrible, but it keeps going doesn’t it?

And the reason I’m not worried about losing a house is because of all the laws, loopholes, and BK options there are. Yes, that part of me changed. After seeing what Washington has done, my “moral hazard” is out the door. Game on!

I think you should do what’s best for you. I can’t argue with the points you’ve made, nor can I predict the future with such games being played in the financial worlds. I still think something’s gotta give soon, but I am in a different personal situation. I own a townhome, with an affordable mortgage, that is suitable enough for me. I would like something different, but I can wait to see if prices drop. If I’m in the townhouse forever, I’ll be happy. If prices drop and I can get what I’d prefer, I’ll be happy.

I think if you can afford it, like what you’re getting, don’t forsee a need to move, and will be ok if prices drop significantly, I say go for it.

Ladies and Gentlemen, introducing the next RE time bomb, REITS:

http://finance.fortune.cnn.com/2013/02/19/mortgage-reits/

Can investors complain if they are getting a reliable 5% net return? How much would be enough? Has betting on Apple been a winner recently? How about bonds? Who wants any of that action? The problem now is that all money is basically dead money, either because it isn’t invested — or because it is.

Leave a Reply