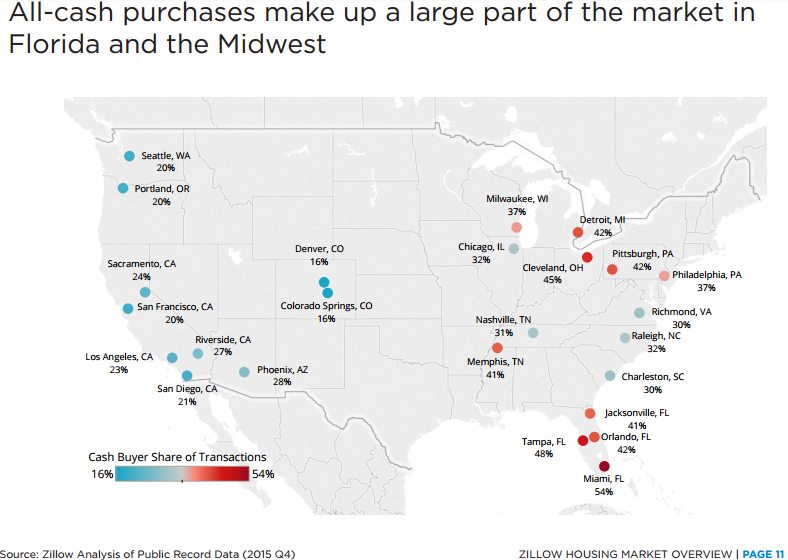

Nearly half of the homes purchased in major cities in Florida are all cash buyers. Cleveland is also seeing nearly half of all home purchases being made with all cash.

When it comes to all cash buying people usually think of select housing markets in expensive cities. While this is true in places like San Francisco or San Marino, there are currently some lower priced markets where all cash buying is massive. Many cities in Florida have close to half of all home purchases being made by all cash buyers. Cleveland is also seeing a similar trend as well. Investors are aggressively targeting lower priced housing markets to load up on properties. Investors in large numbers pulled away from expensive cities in California over a year ago. Value is being seen in other areas where all cash buying is dominating.

All Cash Buyers

While it comes as no surprise that all cash buying is still big in today’s low interest rate market, it does surprise me to see the level of all cash buying happening in places like Florida. What this indicates is that many regular families are still having a tough time buying a home. Even a $200,000 property is expensive if you need to buy it with all cash.

The chart below highlights the volume of all cash buying in various markets:

Source:Â Zillow

What I’m most surprised with is Florida:

All Cash Buyer Percentage

-Miami                 54%

-Tampa                48%

-Orlando             42%

-Jacksonville      41%

That is simply mind boggling in this current market. House humping California has the following numbers:

-Los Angeles                     20%

-San Diego                         21%

-San Francisco                  20%

In other words, it looks like there is way more investment activity in Florida at the moment. While California all cash buyers may dominate certain cities, overall most purchases are being made with mortgages.

You see places like Cleveland and Detroit also having high all cash buying rates of 45% and 42% respectively. In these markets it is clear that investors are trying to find deals. The rental Armageddon machine continues to plow through this country.

While all cash buying may have slowed down in California, it is still going strong in many parts of the United States. As you would expect regarding rents, cities with NIMBYism policies tend to have the fastest growth in rental rates:

Of course this assumes a growing and booming economy. We’ve been out of recession since the summer of 2009. The business cycle is simply part of life and we shall see what happens when this runaway train starts slowing down.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

89 Responses to “Nearly half of the homes purchased in major cities in Florida are all cash buyers. Cleveland is also seeing nearly half of all home purchases being made with all cash.”

Does Zillow have historical comparison for how many were cash buyers in LA in the past years? Would be interesting to see if it’s actually changed.

Side question — is there a public records site which provides any details of the financing of a transaction? Curious where Zillow is pulling its data.

Even bill burr is talking about the la bubble, starting around 1:50

https://m.youtube.com/watch?v=XM9BhsXTZYE

LOL- I love the part where Burr says, “even if they DO find people who can pay for and move into these multi-million dollar condos on the Sunset Strip: they’re gonna be so f#@&kin’ bored cause they knocked down the Whisky, the Roxy and the House of Blues, so there won’t be anywhere to go out anyway…”

Hello DR. I’ve discovered your blog a few weeks back thanks to a fellow reader on Wolf Street. very nice and informative and mostly covers the places I’ve lived in the US. It seems I left the country just in time!

Regarding that crazed Florida market: is there any breakdown for investors buying all cash? How many are foreigners? How many are “mom and pops” investors and how many big funds?

In the 2011-Q2 2016 time frame, Miami-Dade saw just 56 condo towers built with a measly 5,720 units built.

But there are 75 towers with 11,736 units presently under construction, with delivery scheduled between Q4 2016 and 2018. Another 55 towers with 7,026 units have been approved, but building hasn’t started yet.

As I once lived there, my take is people pouring cash into the market must be really desperate to spend their money damn right now because all those towers and those condos are going to cause one of the now familiar South Florida condo bursts. Which is when you make money: you buy during the burst, in cash, and sell during the boom that’s bound to follow at a nice profit. It’s just a matter of being patient.

I suspect these cash buyers are concentrating on preconstruction condo sales which, with the glut described above, have been weak for over a year now but… I still don’t understand why anyone would want to buy so near the top of the bubble when all data hint a correction is around the corner.

Please note: “correction”, not “crash”. When valuations are so nose-bleeding high even a 15-20% drop seems big.

These cash buyers are shooting themselves in the foot by pushing valuations, which are bound to drop when those 10,000+ units enter the market, even higher instead of waiting patiently.

But, again, I’ve been out of the South Florida housing market for years now and have no intention of coming back any time soon…

Why live in the capital of sink holes. Not really a smart idea to be building massive buildings on potentially weak soil.

Don’t ask me: I got out years ago!

Plus the weather is rotten…

I met an agent a few years back who was telling me in the height of the Florida Condo mania boom in 2005 and 2006 he was selling new Miami empty condo shells for a cool one million dollars at a frantic rate, no kitchens, bathrooms flooring etc just a bare bones interior called a builders finish.

When the bubble popped he went to the onsite auctions being held in the same buildings and was watching the same units sell for $150,000….that must really hurt…..

look at this 30 day 125k profit flip.

https://www.redfin.com/CA/Ladera-Ranch/18-Bayley-St-92694/home/5915975

60 day…xp

https://www.redfin.com/CA/Costa-Mesa/133-Morristown-Ln-92626/home/4552962

they are all over the place.

Seller took a 25% haircut.

I too would like to see what makes up these numbers. I have a few guesses. Possibly foreigners are worried that the next Administration in Washington DC won’t be as accommodating to people running here when they feel like it and buying property. There could also be those pulling funds out of the stock market because of concerns about valuations there and thinking real estate, if it generates only 5% a year after fees and expenses is a better bet. There also could be those that have the money are buying real estate as an inflation hedge. Those waiting for a market correction might be waiting for a while. Thirty years ago I was really ticked when the average Westside home was selling for $185,000. I was thinking of sitting on the sidelines waiting for the correction.

“Thirty years ago I was really ticked when the average Westside home was selling for $185,000. ”

How much was the mortgage interest? 18% or 21%? Wasn’t that during the Volker years? What was the rate of wage increase per year back then?….crickets

So, moving forward, could you please enlighten us which of the 2 drivers is going to push the prices higher?????!!!!! Interest dropping 18% or wage increase at the same time with globalization???? I’m waiting for you to enlighten all the fellow bloggers.

Disclaimer: Past performance is no guarantee in the future

These days he spends time buggaring younger generations from the sidelines!

Highly dubious that real estate is a safe haven from the stock market as the two are closely intertwined. 30 years ago, residential real estate was supported by income growth of organic buyers. Today, it is a speculative commodity highly manipulated by Wall Street hedge funds. So if you believe that RE can’t undergo a roller coaster ride like any other speculative mania, then by all means buy as many houses at current price levels.

No such thing as a 100% sure thing anymore! And with real estate, unless you are a landlord with multiple rentals and can survive some hard times as well, you only make money when you sell! It’s only when you have cash in hand that you can say you either made money or lost money!

Prince of Heck, I think you’re bang on. The real estate market isn’t anything like it was 30 years ago. We were still looking at an income ratio to sales price of just over 4 in L.A. 25-30 years ago. That number has more than doubled.

I think that depends on where you live. If you happen to have a job for Facebook or some other IT company likely your income will hence mean higher home values. Another thing I heard that at some big IT firms in the bay area if you happen to live within a certain range from work the company gives you additional pay just to cover living costs. This sadly just gives landlords more reason to keep rents up until the whole thing implodes. This smells more like a Section 8 Plus fund for the IT industry.

Florida, the land of real estate speculation and bubbles on an epic scale.

1920s

http://www.thebubblebubble.com/florida-property-bubble/

The Dr.s take from 9 years ago Comparing 2007 Florida and 1920s

http://www.doctorhousingbubble.com/florida-housing-1920s-redux-history-repeating-in-florida-and-lessons-from-the-roaring-20s/

2009

http://usatoday30.usatoday.com/money/economy/housing/2009-08-02-lonelycondo_N.htm

Good reference.

I will definitely read it.

Foreign buyers with “hot money” are buying tangible assets like housing in the U.S. because of weaker economic growth throughout the world, devalued foreign currencies and financial market turbulence.

http://www.cnbc.com/2016/07/06/foreign-buyers-flood-us-real-estate-but-buy-cheaper-homes.html

http://www.chicagotribune.com/business/ct-illinois-foreign-real-estate-investment-0706-biz-20160706-story.html

Unlike the U.S., many countries have laws and regulations that limit or restrict foreign property ownership:

http://www.macleans.ca/economy/economicanalysis/how-the-rest-of-the-world-limits-foreign-home-buyers/

http://www.vancitybuzz.com/2015/11/vancouver-real-estate-foreign-investment-restrictions/

Housing To Tank Hard Soon!

Jim,

Have you thrown in the towel for 2016? There is still 60 days left for housing to tank before the year ends.

Based on what I see in the South Bay, there is no tanking anywhere to be seen. Houses that are priced correctly sell very quickly.

Towel has not been thrown yet. However, I do admit 60 days is not a long time. It might take till 2017. Yes I have been off by a few years and its frustrating, but that doesn’t mean I’m wrong yet. Wrong timing yes, but overall mega direction change coming I will be right on that.

House tanking is so passe’.

How to buy a home, from Barbara Corcoran (Shark Tank).

She has some good points here, however, I know the consensus on this site is housing will crash… in 2014… in 2015… in 2016… in 2017

http://www.businessinsider.com/shark-tank-barbara-corcoran-house-real-estate-buying-tips-2016-10

A real estate agent who thinks it’s always a good time to buy a house? No way! It takes some expert cognitive dissonance to forget about previous crashes when prices get overheated.

So, when do you buy and how many houses are you going to buy?

Good luck, because you need it.

Realtors I’ve been talking to in the Denver area say there is still an incredible amount of money out there … people out of state or out of country buying sight unseen! So while they might be moving on from S.F., or other California markets, they are now buying in other places! I keep thinking that the money will dry up, but it seems to keep coming and coming!

I think the money will dry up when:

1) The stock market corrects. People are diversifying large market gains into real estate. I am still considering this. Long term gains are taxed at 20%. Time to pull out now before the tax rate goes higher.

2) When the rental market cools even more. Less motivation to become a land baron and REITs have less motivation.

3) When the US heavily taxes foreign real estate purchases.

4) Or when foreign markets completely crash.

A new luxury condo building in San Francisco is sinking and tilting: http://www.sfgate.com/bayarea/article/Sinking-Millennium-Tower-puts-building-agency-on-9220921.php

Homeowners spent $1 million to $10 million per condo. Now the market value of their condos will tank. There goes any hopes of flipping.

Even buying late in 2015 turned out to be a good play.

LA home prices up 6.9% in the last 12 months, OC at 5% and IE at 5.9%.

http://www.ocregister.com/articles/prices-733848-home-year.html

You mean that 2015 was good for flippers and other day traders. Otherwise, buying into an overpriced market is a no go for the vast majority of organic buyers.

No, I meant that buying late in 2015 was also good for organic buyers. A late 2015 organic buyer in LA would be sitting on almost 30% equity at this point and likely very close to rental parity. Nobody should be buying a house with less than 20% down.

20% down payment+6.9% appreciation+2% principal pay down=28.9% equity

You forgot to subtract the expenses (i.e. minus property taxes, minus maintenance costs, etc). Although not relevant in calculating equity, you should factor in costs of selling.

There is nothing organic or natural about a 1-year 30% equity gain. 20% of a 500K house is 100K — which very few organic buyers possess for the privilege (luck) of falling into such “paper” equity. Equity gains in that short period also should matter mostly to flippers and investors, not to organic buyers.

@Janum,

The expenses are factored into the rental parity equation. Who said anything about selling?

@POH,

My example simply points to an organic buyer with 20% down (and there are plenty out there) now has close to 30% equity and is likely very close to rental parity. These people can sleep well at night and are not going anywhere. My whole point was buying late in 2015 turned out to be a good play, contrary to what all the naysayers were yelling on this blog. Don’t confuse this with anything else, it’s not rocket science.

So, buy now for be priced out forever?

He’s continuing to spread the word among RE doubters….

This is kind of false since OC is growing slower in rent than Austin Texas or even Houston Texas, why because of population growth. Land restrictions have a lot less effect on rent its population growth and Houston has the hgihest shortage of apartments to people since it grows about 85,000 a year. Also, most midwest states have seen their rent go down while Texas is growing a lot faster since people leave Ohio and Iowa and moved to Texas.

https://www.apartmentlist.com/rentonomics/june-2016-texas-apartment-list-rent-report/ Rent growing the fastest in some Texas cities since population is growing fast.

Ha, ha, pretty funny. In the 80’s it was the Volker years all right. I was excited to get a mortgage at 11.5% and had to take a Second TD to cover what should have been a down. They could do contorted things more easily to write up a Second that wasn’t disclosed to the bank like it has to be today. The house payment was around $1185 which was a bit considering the salary of around $35,000 a year which was also considered pretty good.

Higher interest rate can cause a price suppression that’s nice when you go to refinance. I don’t see that kind of inflation ( visible anyway with their cooked books) at the moment and Yellen wouldn’t dream of it.

Housing appreciation has been a pretty steady 3% going back to the late 1800’s according to Case – Schiller so if you take a long view this could be a good number. Of course you need a balanced portfolio with stocks too. If you can rent with a positive cash flow your numbers look even better – but that’s not guaranteed and there’s work involved.

I think wages are being suppressed by a host of things. A weak economy, the H1-B visas the undocumented immigrants, jobs and companies off-shored because of our tax rates and a low velocity of money in general. Weak purchases make for weak production which completes the cycle. I read that the real unemployment numbers are 2x to 3x what they say it is. Not a good environment to purchase big long term investments of any kind.

I think our connected world has created an opportunity to study locales and people in order to evaluate potential places to settle down. Some people can also run their business remotely as long as they have a good connection. This works in reverse too.

All I’ve ever tried to suggest is that there are a lot of factors created in the last 20 years with a globalist push and a connected world that lets people compare world centers and move. In this view Southern California ends up looking better that we think it does. Prices are not favorable compared to Houston but he prices and weather are very favorable compared to other large metropolis around the world. Also, the investor class is taking a sharp pencil to the rental market and working their business case. I think this is pushing prices up.

The factors that caused the crash in 2008 don’t exist at the moment because of low inventory and the lack of option loans stuffed into dubious Mortgage Backed Securities. I could be 100% wrong. I frequently am – just ask my wife. What am I missing?

Fensterlips, I believe it is all still being driving by over inflated markets and the quest for yield in a low interest rate environment. I don’t think real estate will be a leading indicator, but, once the markets move the other direction, and/or interest rates rise, I think it’s coming down.

There is zero slowdown in Norcal. Everyone who has been calling a change occurring has been totally off. Even deals that have not sold for a year are now all pending at the same price. In other words, the market is arching and taking properties down that were considered overpriced 6 months ago. Translation: The market is picking up steam, and not even close to cratering.

Outer Eastern Suburbs of Sacramento here – house sales have come to a grinding halt here. 2 of my neighbors put their homes on the market a few months ago and both didn’t get any offers – one at $515k and the other at $509k, same sq footage, nice homes but up nearly double from the crash. They just took them off the market. Other listings in my area growing by the day and not much going pending. Don’t know if its because not a lot of investor activity in my area, mainly families and school is in for the year?

Calgirl, I of course cannot comment on the two listings you mentioned that you said didn’t sell. However, I too am very very familiar with and heavily invested in Sacramento. By ‘eastern suburbs’ are you referring to Rancho or Fair Oaks or Folsom area? I track and invest in those areas as well, inventory has not gone up there, it is actually slightly lower than a few months back even. Also, not only are most properties selling quickly, but properties that hadn’t sold for 6 months plus and have not undergone a price reduction since, are pending as of this week. I can reference 10 properties that could not sell for 6 months plus, did not undergo a single price reduction, and then magically sold this week. Hence, buyers taking down what were considered inflated prices only months ago. This equals an upward trajectory. Look, I think this is a massive bubble forming, however there is no slowdown at all. A correction is still a ways off here.

Miyagi,

Any chance there is some dealing going on at the escrow table to affectively bring the purchase price down on these ?

It never ceases to amaze me how badly people want to see a downturn in RE that they will grab for straws to point out evidence of such a downturn. The reality is that at this point the market continues to chug along and decent well-priced properties are selling quickly. Of course over-priced units will sit like they always do. Maybe one day Jim will be right, but today is not that day.

It’s always amazing that bulls post so much on a RE bubble blog. If things are going so well, why not go out as buy as many properties as you can? Or take out more loans out of your paper equity. Just keep saying to yourself, this time, it’s really truly different.

So, buy now or be priced out forever?

Has there ever been a time to buy than now, at this very hour, this very minute, this very second, this very millisecond? Didn’t think so.

Most of this is a crazy search for yield in a low interest world.

Your bank will pay you .5% on your savings, you think you can make 6-7% buying and renting, you do it.

Jim Taylor will be proven right when interest rates on savings goes up, T bills etc. When you can park your money in a bank and earn 3% interest, how much return are you going to want to risk it in RE? 10%? When that happens pricing will resent.

In Florida what i see is that some of the all cash buyers are Canadians who can buy a condo in Century Village or similar older 55+ condo for between 40 to 60k. For the cost of a car they can have a warm weather bolt hole with access to health care not covered by the CA system.

Again, the Central and South Americans buying condos downtown are not trying to make money. these condos are survivalist bunkers in case poop goes down back home.

That doesn’t mean they don’t make money, if you bought a $500,000.00 condo 4 years ago and sold it today for $400,000.00 you still made a bundle in Brazilian Reals.

I agree with Boca.Let me add that we are currently experiencing of some of the lowest mortgage rates in history. Even if housing prices do go down its a good bet that mortgages rates will go up from here. So unless you are paying all cash, in the future you are going to get less house for more money.

I always find it odd that people rush to “lock in” low interest rates. If interests go up, it’ll just push prices down.

I’d much rather buy at a lower price with a higher interest rate. It requires a lower down payment, it allows one to pay off the principal more quickly, it leaves more potential for a price increase over time, it requires less tax payment, and it potentially allows a refinance when rates go low again.

Lower prices leads to:

Higher down payments

Less money borrowed

Lower property taxes

Lower insurance costs

What’s not to like?

“I always find it odd that people rush to “lock in†low interest rates. If interests go up, it’ll just push prices down.”

That is not necessarily true. You would think it would be, but historically speaking house prices have run independently from mortgage rates. Also it is hard to refinance when you are under-water.

I meant higher down payment percentages.

That is not necessarily true. You would think it would be, but historically speaking house prices have run independently from mortgage rates. Also it is hard to refinance when you are under-water.

Truthster, historically you’re right, but I have to think that rates dipping below 5.5-6% in 2012 was a major driver for these prices.

Buying at a low price with higher interest means you likely wouldn’t be underwater when it comes time to refinance.

@GH

Another pro to higher rates is generally when rates go higher lending standards get looser, since the lender is getting higher yield. Banks tend to not want to lend money when they are only making 2-3%.

GH….

How often have you seen interest rates going up and prices going up….

… so you actually think if you don’t lock in at 3.5%… the price is going to magically go down at 3.75%…. LoL Doesn’t work like that

Throughout history interest rates going up has gone hand in hand with increased prices… why? Because it means inflation and/or economic growth.

Almost every time home prices have gone down it has been accompanied by decreasing interest rates to fight the economic decline.

“Almost every time home prices have gone down it has been accompanied by decreasing interest rates to fight the economic decline.”

Not only are they already rock bottom, but low rates lose their effectiveness over time (8+ years) due to debt saturation, malinvestment, and the inability to address the root problems of the economic malaise. Note that GDP growth has become weaker during each subsequent economic recoveries despite record cheap and easy credit. In other words, low rates cannot repress price corrections forever.

Prince of Heck… Why in the world do you think 3.5% is rock bottom?

Do you pay attention to the Global Economy.

There are already multiple country with 1-2% mortgage rates… The US still has mortgage rates more than double that.. At what for some myopic reason you consider rock bottom.

Is 1-2% rock bottom???… Hell no… Step right up and check out any of the confries with negative interest rates…. Let’s turn to exhibit A… The Nethelands with negative mortgage rates… The government pays you to take out a loan!!!!

Are house prices cheap in the Netherlands? Is there some massive crash???LOL of course not.

So look around and ask yourself…. Would the US government do whatever it takes?

You don’t need my help to answer that.

TA TA!

Let me know when the ECB takes over the Fed and the U.S. becomes Europe. Until then, all bets are on U.S. (not European) rates going up DESPITE your desperate hope that the Fed has an endless bag of tricks. As I mentioned several times, if the Fed were to “do whatever it takes” to prop up asset prices, the real estate market will be the least of our concerns.

BTW, what do you call it when a central bank (the ECB) persists in its extreme policies (i.e. NIRP and QE) even though they threaten the solvency of one of the largest financial institutions and mortgage lenders (Deutsche Bank) despite rising real estate prices? Think that this policy of “doing whatever it takes” won’t affect their financial system?

More high-income earners are renting then before:

http://www.curbed.com/2016/11/1/13489792/rental-real-estate-apartment-high-end-rentals

We are becoming a renter’s nation in our large metropolitan areas.

@Truthster

Historically, real estate price growth barely stayed above inflation and were closely linked to local incomes. Now, prices are far more dependent on credit availability since RE has been heavily commoditized by financial institutions. Thus, cheap borrowing costs have allowed speculators to drive prices up. Why wouldn’t higher interest rates, among other things (i.e. debt saturation) not drive prices the other way?

@Prince

It should, but it just hasn’t worked that way in the past. Looking at historical charts home prices and mortgages rates moved independently of one another. There is no historical data that shows home prices always declined when mortgage rates went up.

I predict we will see mortgage rates of 5-6% within the next 2-3 years. If and when that happens, do you think home prices will decrease enough to offset the increased cost of ownership?

I agree that used to be the case, Truthster, but, like Prince of Heck said, housing also used to be tied to incomes. With home (and auto) loans these days, people are simply calculating what they can afford monthly, so I think rates and prices are linked.

@Truthster

As I pointed out before, one major difference now is that RE is treated as a speculative commodity. Hence, it is rate sensitive. Investors poured into RE when more conservative investments lost their value due to low yields. When yields return and borrowing costs go up, more investors will return to safer havens. Just like stocks, prices fall when investor interest fall — albeit more slowly.

Yes, I do believe that lower fixed costs are better than lower variable (borrowing) costs in the long run. Lower prices = better chance of retiring or refinancing debt.

Lower prices = lower cost of ownership (property taxes and other housing costs are tied to the value of the house, not to interest rates )

@Prince

RE has always been treated as a commodity for those “in the know”. But with the explosion of REITS not to mention all the TV shows and media press, RE investing has become more attractive & accessible to the mainstream and a large part of most people’s investment portfolios. Much of it is a matter of chasing yield. Like someone said earlier if you can make 6-7% net return on a rental compared to 1% in a online savings account, why wouldn’t you do it? Factor in appreciation of say 5-10% annually and you can create some real wealth unless the bottom drops out. Even then you still have the rental income while you ride the market back up.

@Prince

I understand your point. I don’t think interest rates are going to increase that fast, it will take a few years at least. But when they do I’m sure some investors will jump ship for safer ground.

@Prince

“RE has always been treated as a commodity for those ‘in the know’. But with the explosion of REITS not to mention all the TV shows and media press, RE investing has become more attractive & accessible to the mainstream and a large part of most people’s investment portfolios.”

The fact that REIT’s and other forms of RE investments have been around for several decades does not explain the exponential price appreciation where organic buyers have been priced out in several markets over the last 15 years. However, the expansion of cheap and easy credit globally by central banks does.

“Much of it is a matter of chasing yield. Like someone said earlier if you can make 6-7% net return on a rental compared to 1% in a online savings account, why wouldn’t you do it? Factor in appreciation of say 5-10% annually and you can create some real wealth unless the bottom drops out. Even then you still have the rental income while you ride the market back up.”

Yes, this “wealth” is based on investor speculation desperately searching for yield and made possible by extreme Fed and government financial engineering. That type of mania is nothing new. Neither is the ensuing trail of tears. Do consult reports where rents are coming down because of a glut of new apartments with many new ones still on the way. Also the reports where the capitalization rate for many rentals is low because they were purchased far too high.

I have a theory maybe edging on a conspiracy theory.

The Baby Boomer Bubble is rapidly entering retirement age. What better way for the Fed and US Government to keep them happy, clothed, and fed than to keep inflation low?

High inflation is very bad for fixed income recipients.

That has ramifications for younger investors. Low inflation=low bank interest rates so they are looking for better investments. Real Estate and Stocks which are driving up both.

The Baby Boomers who own a house are Ok. The ones who don’t are moving back in with children.

Keeping inflation and SS increases down is really good for the country until the Baby Boomer bubble passes. Even with the ramifications.

I wouldn’t even call it a conspiracy. The Federal Reserve Board members are all boomers, and the average age of the Senate is 61 and Congress is 57. I can’t imagine there’s a lot of voting against self interest in the Fed and our government, so they just need to kick the can down the road another decade or two.

I see the value proposition of purchases of anything of large value (housing/cars), being “what the buyer can afford per month”, and NOT how much the actual cost is. The thinking is that we are cash flow/credit purchasers and not “real price” purchasers, so low interest rates just make the cash flow purchase on credit easy(er). The actual date you will own whatever you are buying is so far out in the future (cars: 5-7 years anymore, houses 30 years), and they are so expensive anyway, one can only get these things by layering on more monthly debt. At some point, be it higher interest rates, lack of real income growth and just plain too high prices, we reach a point where the system just runs out of gas. We are here now………slowly perhaps, but we are here now.

Somewhere along the way, Americans became brainwashed into thinking that value = price. A greater share of their savings and incomes are devoted to servicing high housing costs, their wealth becomes increasingly dependent on the semblance of real estate appreciation. Hence, the inexorable belief in a new economic paradigm where the reflation of their paper equity could last indefinitely.

“…a greater share of their savings and incomes are devoted to servicing high housing costs…”

No question about it.

But where is the breaking point?

At what point does PITI and maintenance costs exceed available income?

The rule of thumb use to be 30% max.

Now 50%+ is common.

Where does it end 60%, 70%+?

Or as Dr. HBB says, every day becomes Taco Tuesday.

Could be the inevitable recession. Or a financial meltdown caused by the existing financial engineering (i.e. Deutsche Bank). We know that excessive debt through low rates are the proverbial noose for retail investors and buyers.

All I know is everything has an apex, and all real estate markets are different. Anywhere between 2002-2014 was a bad time to buy a house in Alaska, especially on the higher end. Now with crashing oil prices, and large amounts of high paying jobs leaving the state, there are price reductions of over %50 just this year in some cases-

http://www.zillow.com/homes/for_sale/Anchorage-AK-99501/2112679360_zpid/100220_rid/globalrelevanceex_sort/61.218154,-149.895551,61.200379,-149.926064_rect/14_zm/

http://www.zillow.com/homes/for_sale/54822278_zpid/globalrelevanceex_sort/61.236094,-149.887162,61.164975,-150.009213_rect/12_zm/

Thinking I will buy in another few months, and get something w/ a mother in law suite that I can either find a long term renter to subsidize, or AirBnB it in the summer, and have a place to live when I go back to visit family.

“I understand your point. I don’t think interest rates are going to increase that fast, it will take a few years at least. But when they do I’m sure some investors will jump ship for safer ground.”

If investors were could time the market, then previous busts wouldn’t have been as frequent or severe as they were. As I mentioned above, many markets are suffering from a glut of new apartments with many more on the way. Insiders are selling even as flippers and investors are getting in. So much for getting out on time.

To your point Prince, I bought a condo in 2012 in the Studio City area that I rent out. On our street in just the last few years, I’ve seen 2 different properties with 2-4 units get knocked down with large apartments built in it’s place. It’s taken some recovery time for developers to get back on it, but we’re going to see a boom in apartments coming onto the market.

“For every home buyer coming into the state, there are three Californians selling and moving elsewhere, according to data analysis firm CoreLogic.”

http://money.cnn.com/2016/11/04/pf/people-moving-out-california/index.html?iid=hp-grid-dom

If this truly was the case, wouldn’t inventory be higher then it is?

Nov 8th and beyond…When a jobs report comes out with 161k jobs and the pundits think this is a good sign, folks you know they think the public is stupid which many are.

After all who pays 21.8 million for a bay area house worth maybe 1.2m at most.

Hilary won’t matter, she will be impeached so why vote for a lame duck before she gets sworn in. Trump has great plans only problem, is a body of do nothings known as congress who will fight the guy tooth and nail for 4 years.

As a very conservative investor all my life I now see clearly what’s in play, a even more reason for all to save a few bucks if you can, the road to the bottom is coming fast very fast, you could see a Arab spring in this country, I kid you not.

My brother is selling his pristine Modern home in Venice beach that’s on a walk street. He is asking 3.4 million and he’s already received an offer in less than a week on the market from a young girl who’s father will pay cash for the house. She also owns a home in San Francisco. Man! I was born into the wrong family. I know money isn’t everything, but it must be nice.

Interesting report states CA is losing more people to other states then gaining as housing costs push low- and middle-wage workers out of California.

http://next10.org/sites/next10.org/files/beacon-press-release.pdf

But but but Larry Yun says:

Millenials will drive 2017 existing-home sales

http://www.marketwatch.com/story/young-first-time-home-buyers-will-drive-2017-existing-home-sales-2016-11-04

Yun must be worried that investors aren’t as hot for RE if, after all these years of “recovery”, he expects organic buyers to pick up the slack.

“The good news is that an expansion of entry-level home buying won’t bring about a repeat of a late 2000s-style real-estate crash, according to Atlanta Federal Reserve Bank President Dennis Lockhart”

He must be using his best Bernanke impersonation.

I paid $250k (cash buyer) for my house in the Atlanta suburbs 2 months ago. Zillow had is estimated around that price tag when we bought.

Just two months later, it’s estimated at around $275k. At the rate things are going up around here, I wouldn’t be surprised if Feb/March – spring rush, I could sell it for over $300k in just a couple more months.

I left California last year due to the cost of housing, and am flat out shocked to see things go beserk down here in the South.

I wonder how many of these cash purchases were made by retirees who sold their big house up north and downsized. into something less than $100K.

Leave a Reply